The recent preliminary LX Semicon Q3 2025 earnings announcement has sent a significant shockwave through the investment community. With key financial metrics falling dramatically short of market consensus, investors are understandably concerned about the company’s trajectory. The core questions are clear: What triggered this sharp downturn, and what does it mean for the future of LX Semicon stock?

This comprehensive analysis unpacks the Q3 results, explores the underlying causes of the performance slump, and evaluates the company’s financial health and strategic initiatives. We will provide a clear, actionable perspective on both short-term risks and long-term opportunities to help you navigate this period of uncertainty and make well-informed investment decisions.

The Q3 2025 Earnings Report: A Closer Look at the Numbers

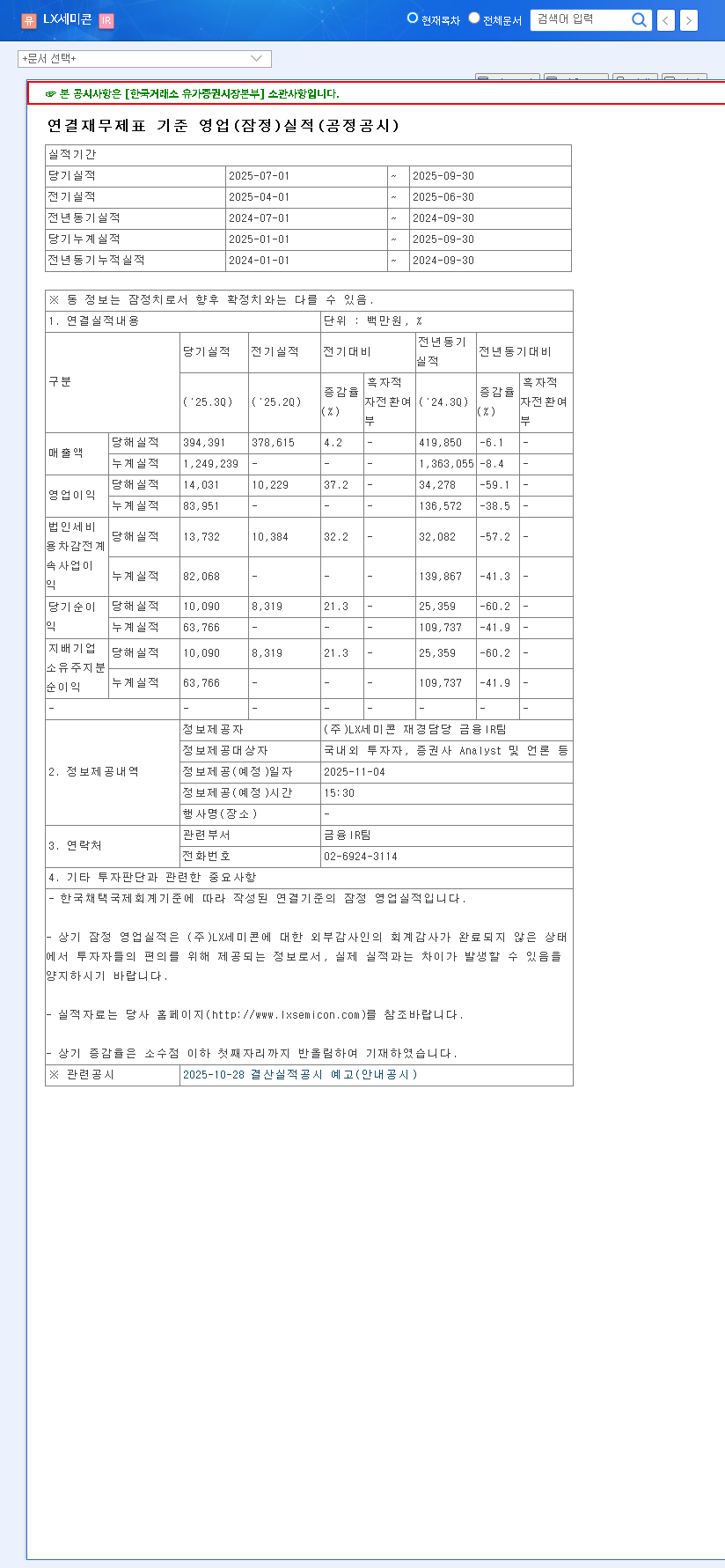

LX Semicon Co., Ltd. officially reported its preliminary third-quarter results for 2025, revealing a significant miss on all major financial fronts. The figures paint a challenging picture when compared against both market expectations and prior periods.

- •Revenue: KRW 394.4 billion, a 9% miss versus the market estimate of KRW 435.7 billion.

- •Operating Profit: KRW 14.0 billion, a staggering 41% miss compared to the estimate of KRW 23.6 billion.

- •Net Profit: KRW 10.1 billion, a 46% miss against the estimated KRW 18.6 billion.

These results represent a clear deterioration in profitability, falling not only below analyst forecasts but also declining quarter-over-quarter and year-over-year. For detailed information, you can view the Official Disclosure (DART).

Core Factors Behind the Earnings Slump

The disappointing performance can be attributed to a confluence of internal business challenges and external macroeconomic pressures. Understanding these factors is crucial for any investor analysis.

Weakness in the Core DDI Business

The primary driver of the slump was the underperformance of LX Semicon’s main business: the System IC segment, specifically Display Driver ICs (DDIs). DDIs are essential components that control the pixels in displays for TVs, smartphones, and monitors. The weakness here stems from a broader slowdown in the global DDI market, as major customers adjusted their inventories in response to cooling consumer demand for electronics. This industry-wide trend directly impacted LX Semicon’s sales volume and pricing power.

Escalating Logistical and Operational Costs

Compounding the revenue shortfall, the company faced significant cost pressures. A sharp increase in global ocean and container freight rates eroded profit margins. These heightened logistics costs, a persistent challenge in the post-pandemic supply chain, proved to be a major drag on the bottom line, turning a revenue problem into a severe profitability crisis.

“The Q3 report highlights a perfect storm: a cyclical downturn in their core market combined with secular cost inflation. The key question for investors now is whether the company’s diversification strategy can provide a meaningful buffer against these headwinds in the coming quarters.”

Silver Linings: Financial Stability and Future Growth Engines

Despite the grim quarterly results, it’s important to look beyond the headlines. LX Semicon possesses underlying strengths that provide a foundation for recovery.

A Fortress Balance Sheet

The company maintains an exceptionally robust financial structure. With a low debt-to-equity ratio and stable, positive cash flow, LX Semicon is well-positioned to weather short-term storms without facing significant financial risk. This debt-free management approach is a key positive, offering flexibility and resilience.

Strategic Diversification and R&D Investment

Management is actively working to reduce its reliance on the DDI market. The new automotive thermal substrate business, which began mass production in April 2025, is a key part of this strategy. Additionally, ongoing R&D investments in areas like Microcontroller Units (MCUs) signal a clear intent to capture future growth. While the revenue contribution from these new ventures is still minimal, they represent crucial long-term growth drivers. For more on market trends, industry analysis from sources like Gartner’s Semiconductor Forecast can provide valuable context.

Investor Outlook and Strategic Action Plan

Given the LX Semicon Q3 2025 earnings report, a bifurcated investment view is necessary.

Short-Term Outlook: A Cautious Stance is Warranted

In the immediate future, the LX Semicon stock price is likely to face significant downward pressure. The market will react to the earnings miss and the uncertainty surrounding the core business’s recovery. Expect analyst downgrades and weakened investor sentiment. A cautious, wait-and-see approach is advisable for short-term traders.

Mid-to-Long-Term Strategy: Focus on Key Milestones

For long-term investors, the focus should shift to the company’s ability to execute its recovery and growth strategy. Re-evaluation of the stock’s value will depend on tangible progress in several key areas. Our internal guide on How to Analyze Semiconductor Stocks provides a framework for this evaluation.

Key monitoring points include:

- •New Business Traction: Watch for specific revenue figures from the automotive thermal substrate and other new segments in subsequent earnings calls. Is their contribution growing meaningfully?

- •Cost Management: Scrutinize management’s plans to mitigate high logistics costs. Are they implementing more efficient supply chain strategies?

- •DDI Market Recovery: Monitor broader industry trends. Are customers beginning to increase orders again? Is inventory destocking nearing its end?

- •Financial Discipline: Confirm that the company maintains its strong balance sheet and does not allow short-term issues to evolve into long-term financial risks.

In conclusion, while the Q3 2025 results are undeniably disappointing, LX Semicon is not without its strengths. Investors should balance the current operational headwinds against the company’s solid financial footing and long-term growth potential. A careful, data-driven approach will be essential in the months ahead.