The global transition to renewable energy is creating unprecedented demand for critical infrastructure, with Energy Storage Systems (ESS) at the very heart of this revolution. In a decisive move to capture this growth, HanJungNCS.Co.,Ltd has announced a landmark 24.3 billion KRW investment to establish a HanJungNCS US ESS production facility. This strategic expansion into North America is poised to reshape the company’s future, but it also introduces new challenges. This analysis explores the profound implications of this venture, from market opportunities to investor considerations.

The Landmark Investment: What We Know

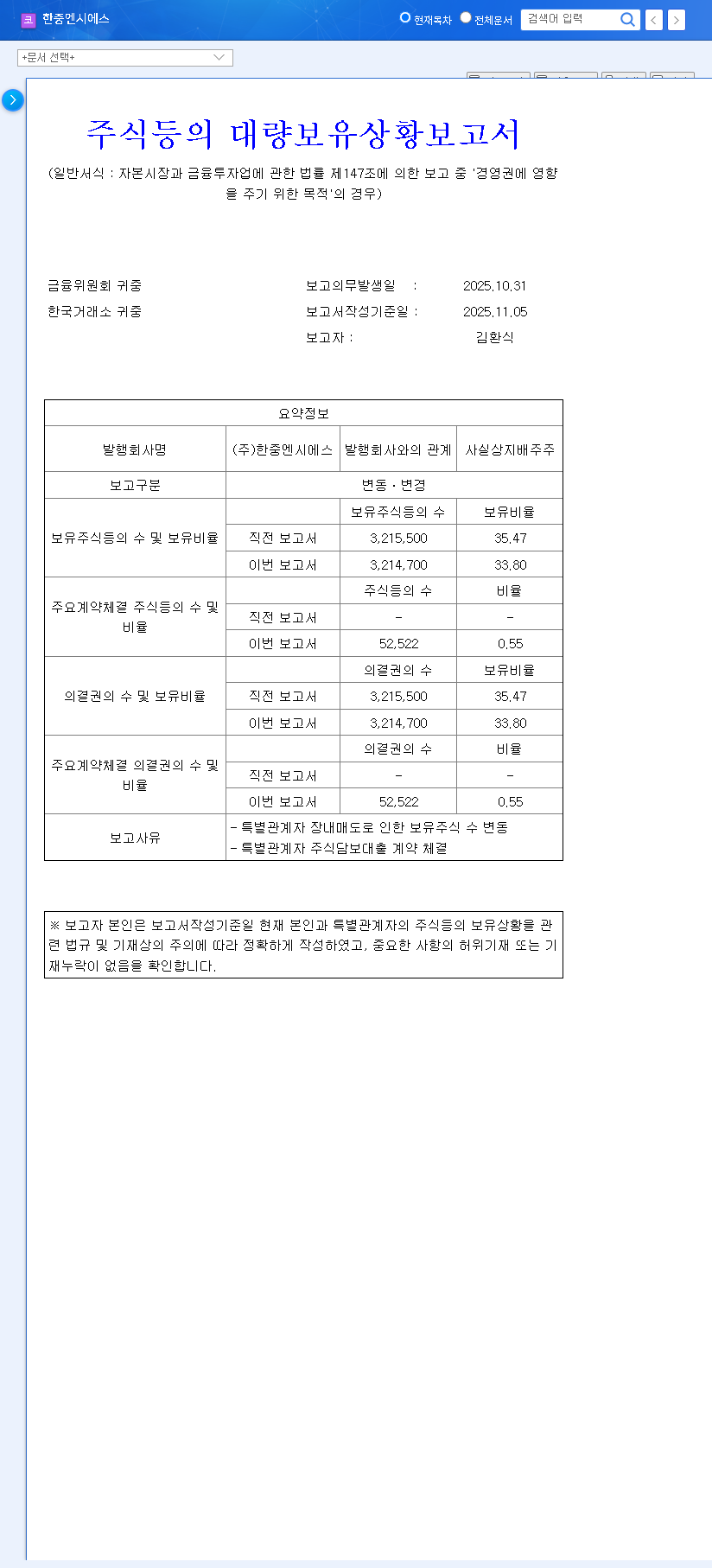

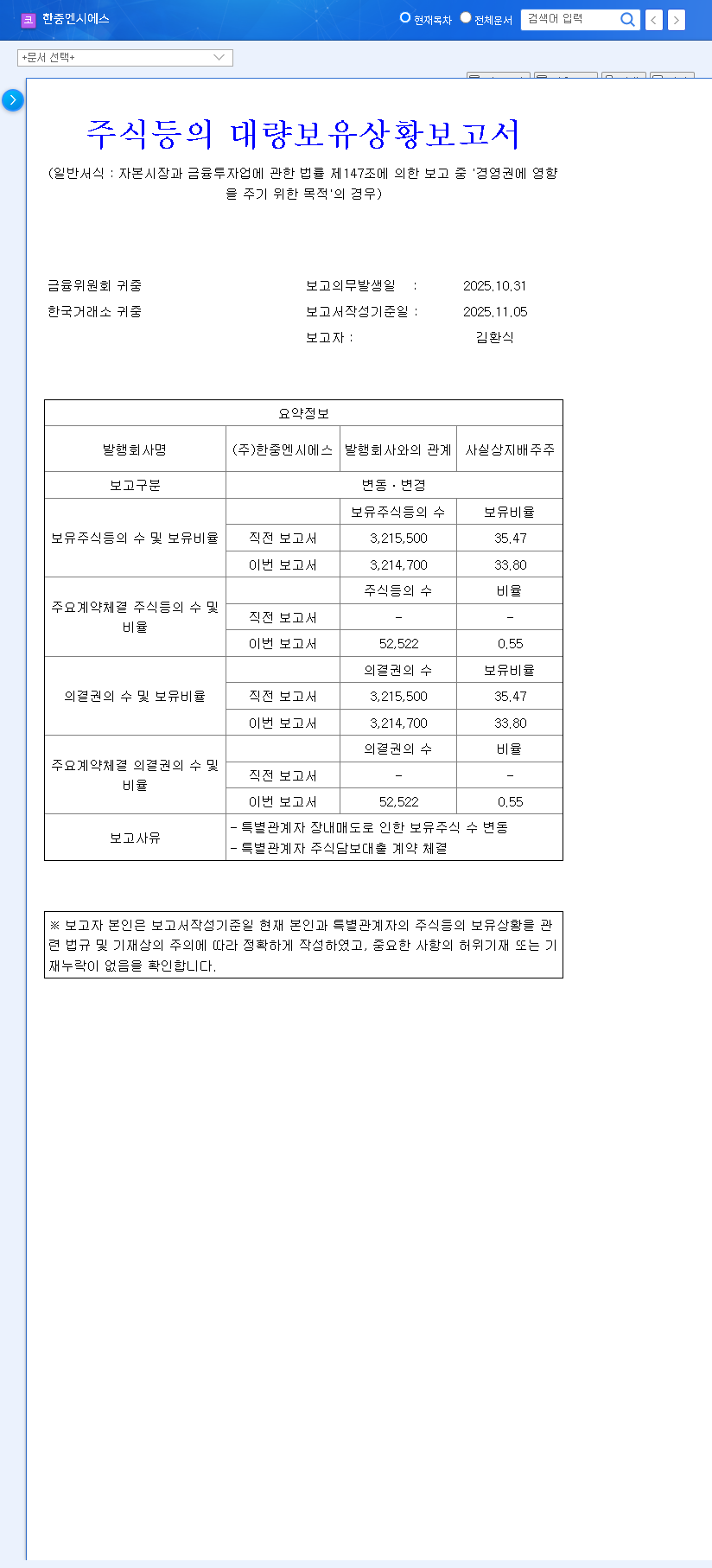

HanJungNCS.Co.,Ltd has confirmed that its subsidiary, HANJUNG AMERICA CO. (Indiana), will acquire new facilities and infrastructure to build a dedicated production hub. This investment is not just about acquiring assets; it’s a strategic declaration of intent to become a dominant player in the lucrative North American market. According to the Official Disclosure, the acquisition is scheduled for completion by November 18, 2025.

This 24.3 billion KRW investment is aimed squarely at securing a state-of-the-art ESS production base, enabling localized manufacturing, reducing logistical complexities, and enhancing our cost competitiveness in the North American region.

Why North America? The Booming US ESS Market

The decision to establish a HanJungNCS US ESS production base is fueled by the explosive growth of the American renewable energy sector. Favorable government policies, such as the Inflation Reduction Act (IRA), provide significant incentives for domestic manufacturing. Furthermore, the increasing reliance on intermittent power sources like solar and wind has created a critical need for grid stabilization, a role perfectly filled by advanced Energy Storage Systems. Data from authoritative sources like the U.S. Energy Information Administration (EIA) project continued, robust growth in this sector for the next decade. By producing locally, HanJungNCS can better serve this demand and build a resilient supply chain, a crucial lesson learned from recent global disruptions.

Key Strategic Benefits of the Investment

- •Accelerated Market Penetration: A local presence allows for faster response times, customized product development, and stronger relationships with North American clients, driving market share growth.

- •Enhanced Cost Competitiveness: Onshoring production eliminates substantial international shipping costs and potential tariffs, directly improving profit margins.

- •Synergy with EV Business: The facility can create powerful synergies with HanJungNCS’s EV components division, as both rely on similar core technologies. Explore this further in our guide to the EV components market.

- •Securing Future Growth: This move solidifies HanJungNCS’s position as a forward-looking company committed to the future of energy, boosting investor confidence.

Navigating the Challenges: A Clear-Eyed View of Risks

While the upside is significant, this ambitious Energy Storage System investment is not without risks. Investors should remain aware of potential hurdles that could impact the project’s timeline and profitability.

- •Financial & Cash Flow Strain: An outlay of 24.3 billion KRW is substantial and may place short-term pressure on the company’s cash reserves, requiring meticulous financial management.

- •Operational & Execution Risks: Establishing a new facility in a foreign market involves navigating different regulatory landscapes, labor laws, and supply chain logistics.

- •Intensifying Competition: The US ESS market is attracting global players. HanJungNCS must differentiate through superior technology, quality, and service to succeed.

- •Macroeconomic Volatility: Fluctuations in exchange rates, interest rates, and raw material prices could impact production costs and overall project ROI.

Investor Outlook & Future Milestones

From a long-term perspective, the expansion of HanJungNCS US ESS production capabilities is a powerful catalyst for growth. It signals a proactive strategy to capitalize on one of the most significant economic shifts of our time. While short-term stock price volatility is possible due to the capital expenditure, the move solidifies the company’s growth narrative. Prudent investors may consider a phased approach, aligning their positions with key project milestones.

Key Points to Monitor:

- •Progress on the facility’s construction and operational launch date.

- •Announcement of new customer contracts and partnerships in North America.

- •Quarterly reports detailing initial production output and sales performance from the US subsidiary.

- •Impact of macroeconomic factors (e.g., KRW/USD exchange rate) on the company’s financials.

Frequently Asked Questions (FAQ)

Q1: What is the main driver for HanJungNCS’s US investment?

The primary driver is to capitalize on the rapidly growing US ESS market, driven by renewable energy adoption. Local production enhances cost-competitiveness and strengthens their market position.

Q2: How will the ₩24.3B investment affect HanJungNCS financially?

It may cause short-term pressure on cash flow. However, the company’s sound financial base suggests it is manageable, and the long-term potential for increased revenue and profitability is expected to outweigh the initial cost.

Q3: What are the growth prospects for the North American ESS market?

The market is projected for sustained, high growth due to government clean energy policies and the essential need for grid stabilization, making it a critical region for any major ESS player.