Global apparel manufacturing powerhouse, HANSAE CO.,LTD., is making waves in the financial markets with a remarkably positive 2025 annual earnings forecast. After a period of sluggish performance, this projection suggests a significant turnaround, with investors keenly watching if the HANSAE CO.,LTD. stock is poised for a major rally. The company anticipates substantial growth in both operating and net profits compared to 2024, raising a critical question for investors: Is now the time to buy?

This comprehensive HANSAE investment analysis provides a deep dive into the 2025 earnings outlook, dissecting the company’s core fundamentals, strategic growth initiatives, and the multifaceted factors—both positive and negative—that could influence its stock price. Whether you’re a current shareholder or considering a new position, this report will equip you with clear, actionable insights.

The Landmark 2025 Earnings Forecast: A Turning Point?

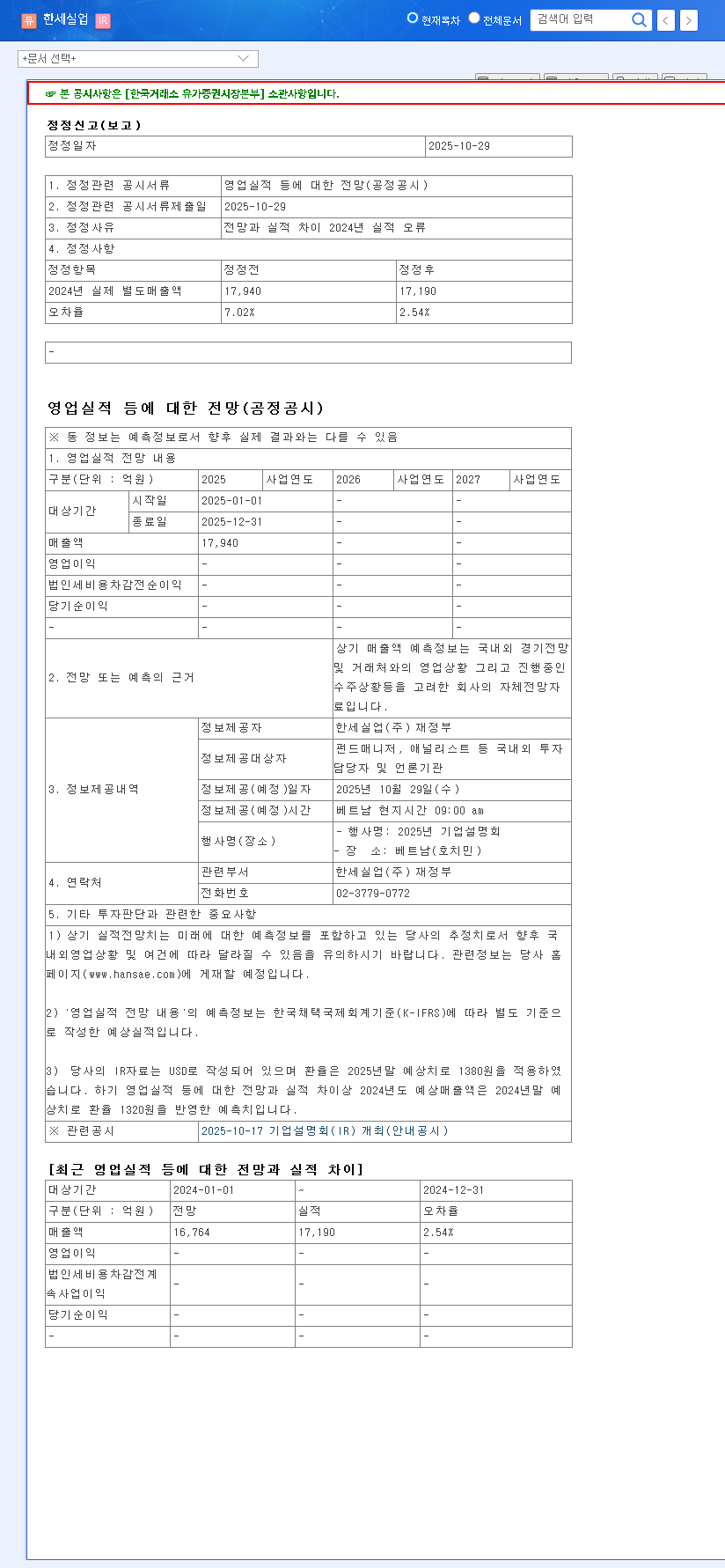

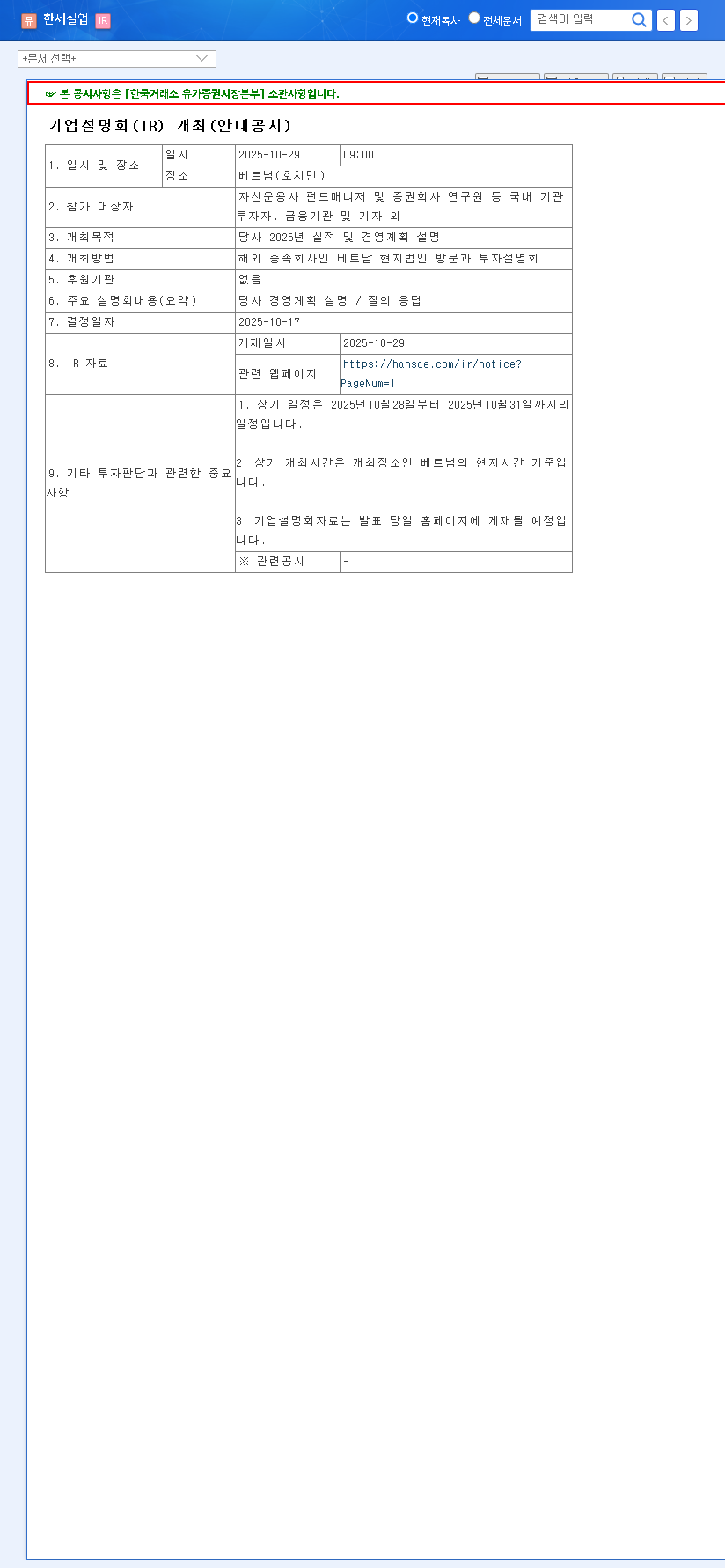

On October 29, 2025, HANSAE CO.,LTD. released its official annual revenue forecast, signaling a new era of growth. According to the Official Disclosure (Source: DART), the company projects revenue for 2025 to reach KRW 2.7987 trillion, a solid 5% increase from the 2024 estimate. The more striking figures lie in profitability:

- •Operating Profit Surge: Expected to skyrocket by an impressive 55%, from KRW 215.6 billion in 2024 to KRW 333.9 billion in 2025.

- •Net Profit Turnaround: Projected to improve dramatically from a modest KRW 3.2 billion in 2024 to a robust KRW 333.1 billion in 2025.

This optimistic HANSAE 2025 earnings forecast marks a significant departure from the operating losses recorded in 2022 and 2023. This turnaround is widely seen as the culmination of strategic internal improvements meeting a more favorable global market environment.

Core Strengths & Future Growth Strategy

HANSAE’s foundation is its role as a leading global Original Equipment Manufacturer (OEM) and Original Design Manufacturer (ODM) in the apparel industry. This means it manufactures clothing for major U.S. retail giants like TARGET, OLD NAVY, and GAP. Understanding its strategic pillars is key to evaluating the potential of HANSAE CO.,LTD. stock.

Robust Global Production Network

The company operates an expansive production network across 8 countries, including key hubs in Vietnam, Indonesia, and Central America. This geographic diversification provides crucial operational efficiency, cost competitiveness, and resilience against supply chain disruptions—a significant advantage in the post-pandemic era, as noted by industry experts at Bloomberg.

Strategic Vertical Integration & Diversification

HANSAE is aggressively moving to control more of its supply chain and diversify its revenue streams:

- •Acquisition of TEXOLLINI, INC.: This move signals a strategic push into higher-value product categories, enhancing profit margins.

- •Guatemala Spinning/Dyeing Factory: By producing its own key raw materials, HANSAE strengthens its defense against cost volatility and gains greater control over production timelines and quality. This is a critical step for any apparel OEM stock.

- •Fabric Business Growth: The expansion of its subsidiary, Color & Touch Co., Ltd., adds a stable and growing revenue stream to its overall business structure.

Analyzing the Impact on HANSAE CO.,LTD. Stock Price

The forecast is promising, but investors must weigh the positive catalysts against potential headwinds. Here’s a breakdown of the factors at play.

Positive Catalysts: Strong Tailwinds for Growth

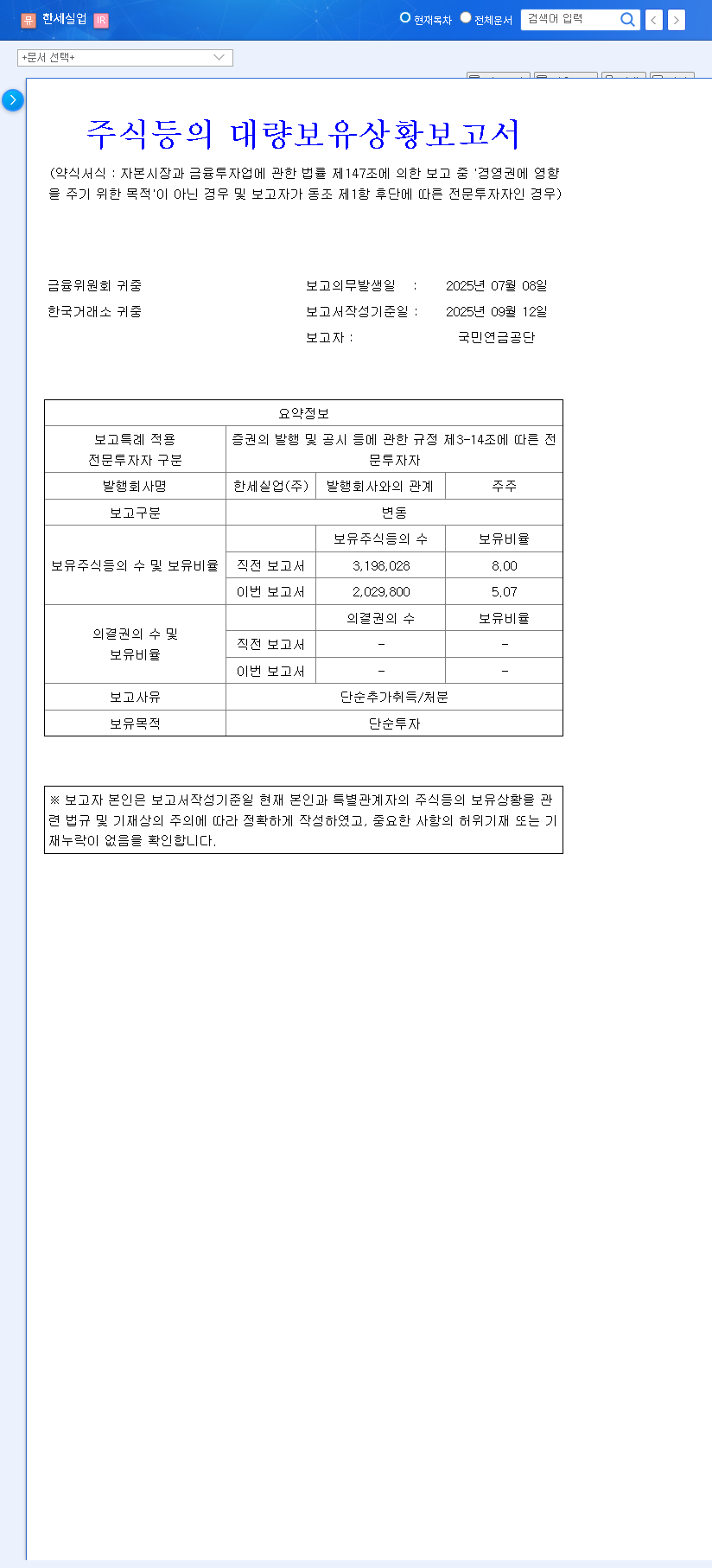

The projected improvements in key profitability metrics are the strongest drivers for stock price appreciation. Indicators like operating profit margin (expected to rise from 8.09% to 11.93%) and Return on Equity (ROE) (from 0.49% to 5.84%) signal a fundamental strengthening of the company’s financial health and operational efficiency.

Neutral Variables: The Double-Edged Swords

Certain macroeconomic factors could have a mixed impact. Fluctuations in the USD/KRW exchange rate can boost revenue in KRW terms but may also increase overseas production costs. Similarly, while stable oil prices and interest rates are currently favorable, any future volatility remains a significant variable that could affect everything from raw material costs to consumer spending.

Potential Risks: Factors Requiring Vigilance

Despite the positive outlook, several risks warrant continuous monitoring:

- •U.S. Market Dependence: With a high concentration of clients in the United States, an economic slowdown there could directly impact orders and revenue.

- •Geopolitical Instability: Operational risks, such as the business environment in Haiti, require careful management.

- •Macroeconomic Headwinds: Global inflation and unpredictable geopolitical events can dampen investor sentiment and affect the real economy. For more on this, see our guide to investing in textile stocks during uncertain times.

Overall Assessment & Investment Thesis

Investment Opinion: Buy. The 2025 earnings outlook for HANSAE CO.,LTD. presents a compelling case for investment. The substantial profit growth, coupled with strategic initiatives in vertical integration and portfolio diversification, indicates a company overcoming past challenges and building a stronger foundation for long-term growth.

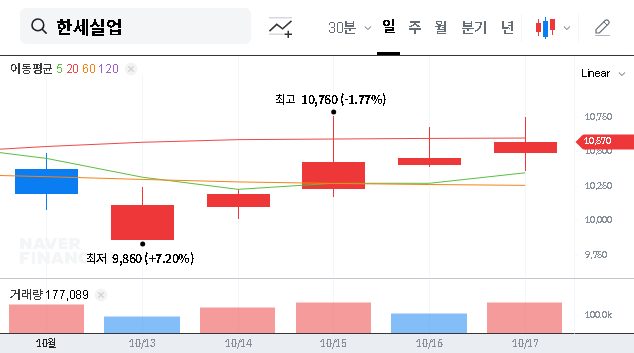

Based on the 2025 estimated Earnings Per Share (EPS) of KRW 3,776, the closing price of KRW 20,800 on Oct 29, 2025 (PER 14.86x) appears to be an attractive valuation that does not yet fully reflect the company’s growth potential and improved fundamentals. The combination of an exceptional growth forecast and efforts to secure long-term drivers makes the HANSAE stock price look appealing at current levels.

Disclaimer

This analysis is for informational purposes only and is based on publicly available data. It does not constitute an investment recommendation. All investment decisions carry risk, and the ultimate responsibility rests with the individual investor. Please conduct your own due diligence before making any investment.