The recent news concerning the Hydrolithium treasury stock disposal has sent ripples through the investment community. With Hydrolithium (101670) planning to sell shares worth 1.6 billion KRW, investors are at a crossroads: does this move signal a strategic step towards resolving liquidity issues, or is it a desperate measure that highlights deeper financial instability? This comprehensive Hydrolithium stock analysis will dissect the event, evaluate the company’s precarious financial health, and provide actionable investor guidance.

The Official Announcement: What Happened?

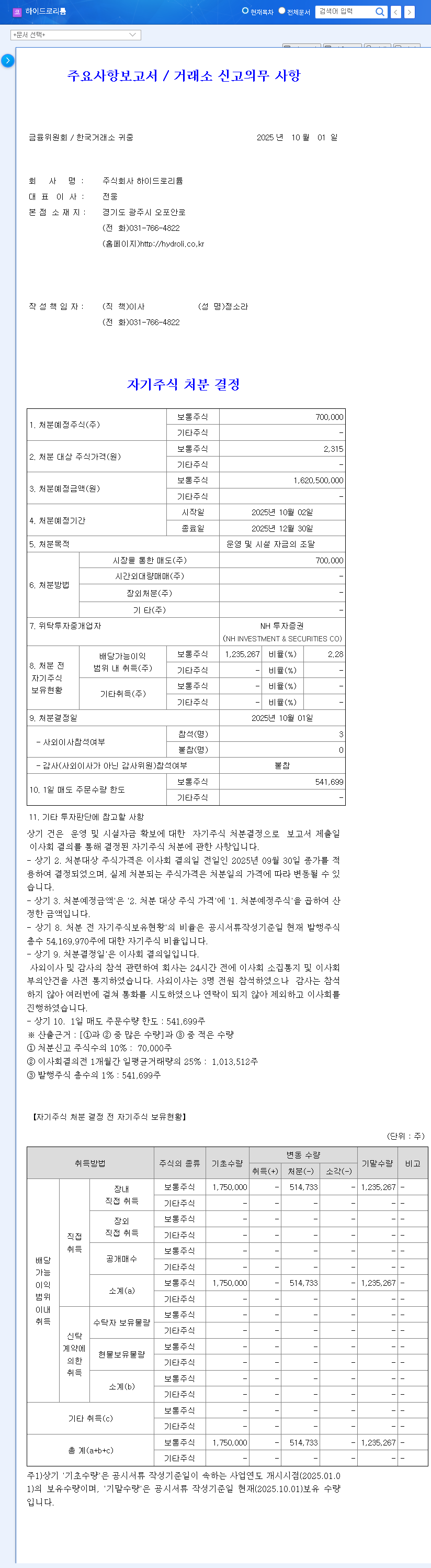

On October 1, 2025, Hydrolithium formally announced its decision to dispose of a significant portion of its treasury shares. According to the company’s filing, the plan involves selling 700,000 common shares, which accounts for approximately 1.29% of the total outstanding shares. The transaction, facilitated by NH Investment & Securities, is expected to raise around 1.6 billion KRW, earmarked for securing essential operating and facility funds. You can view the complete details in the Official Disclosure (DART Source).

While seemingly a standard corporate finance maneuver, this treasury share sale cannot be viewed in isolation. To grasp its true implications, one must examine the turbulent financial waters Hydrolithium is currently navigating.

Unpacking the Financial Crisis: Why Now?

Hydrolithium is in the midst of a strategic pivot, scaling down its legacy civil engineering materials business to focus on the high-growth secondary battery materials sector. The potential to produce high-quality lithium hydroxide is a compelling narrative. However, the company’s financial statements paint a grim picture that demands scrutiny.

Key Financial Red Flags

- •Persistent Losses: The first half of 2025 saw a continuation of declining sales and significant operating losses, signaling a severe profitability crisis.

- •Weakening Balance Sheet: A rapidly increasing debt-to-equity ratio combined with dwindling cash reserves has critically weakened the company’s financial structure and liquidity.

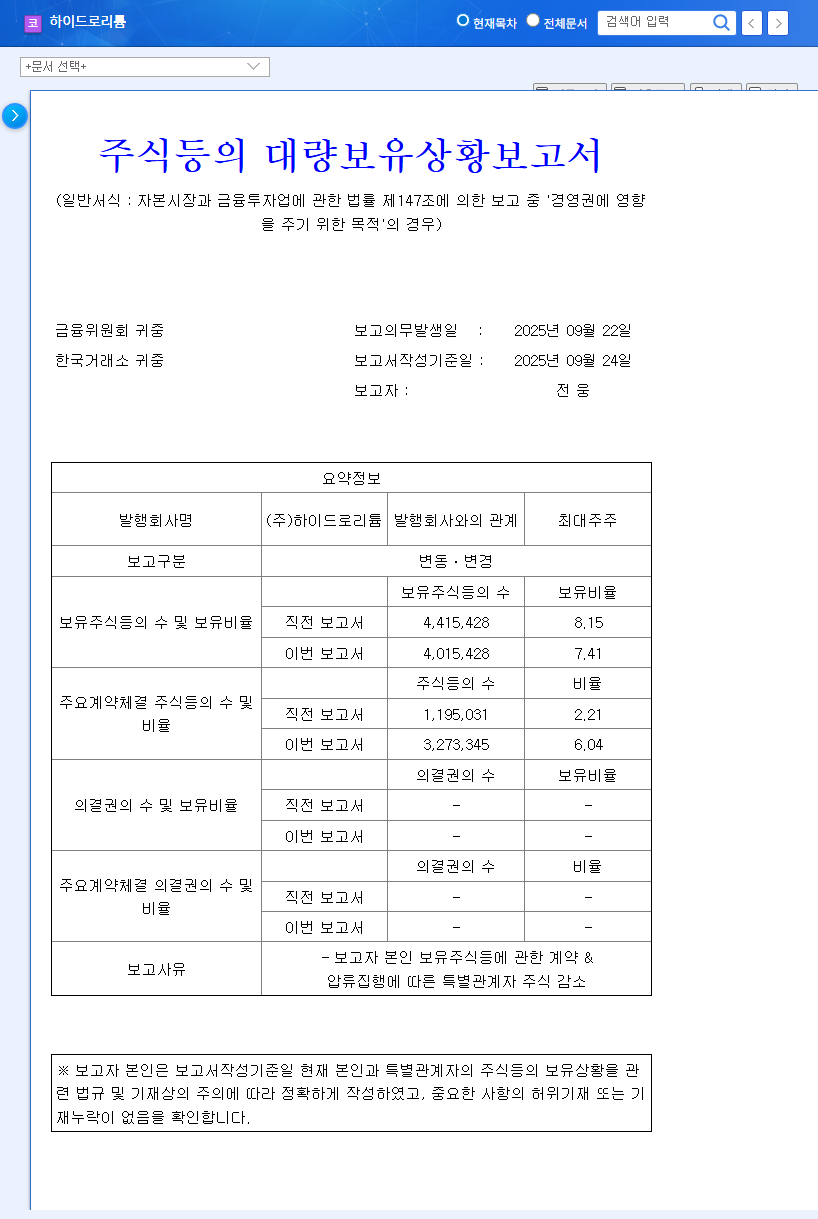

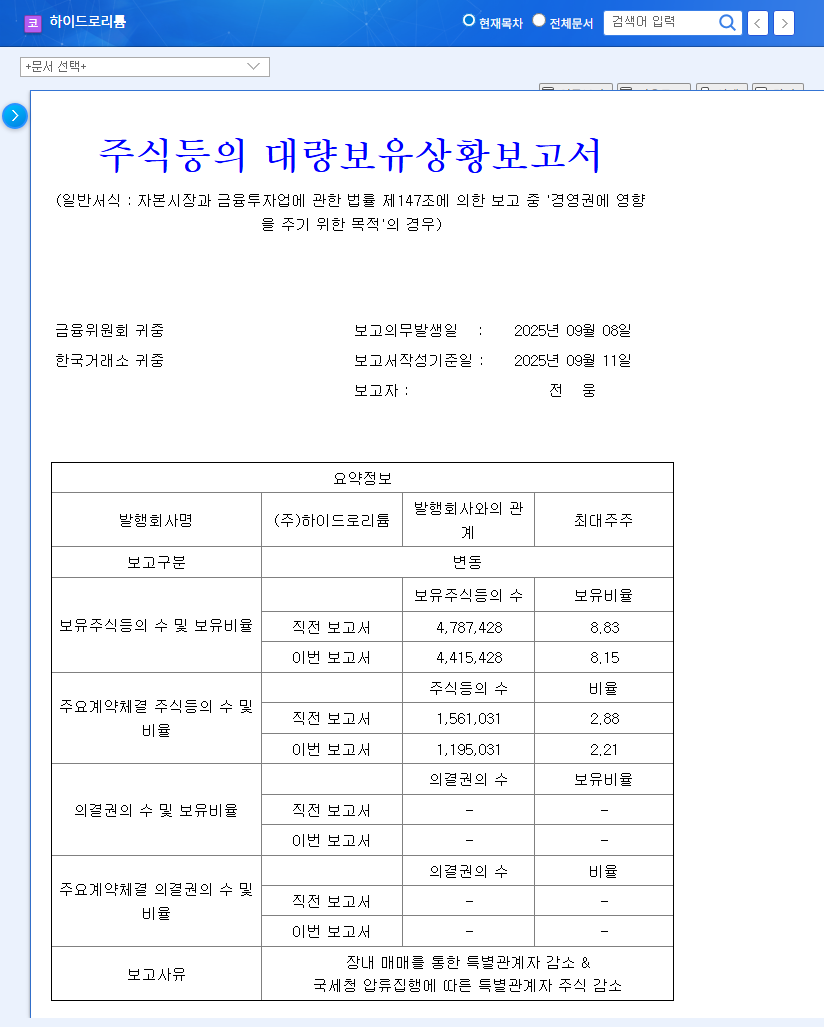

- •Default and Seizures: The failure to make convertible bond interest payments, subsequent loss of benefit of time, and provisional seizures have raised serious doubts about the company’s ability to continue as a going concern.

Given this immense financial pressure, the Hydrolithium treasury stock disposal appears to be an unavoidable, last-ditch effort to secure immediate cash. This move is a short-term fix for a company grappling with long-term systemic issues.

For investors, a treasury stock sale from a financially distressed company is often a double-edged sword. It provides immediate cash but simultaneously signals to the market that internal cash flow is insufficient to cover operations, potentially eroding confidence.

Impact Analysis: Short-Term Relief vs. Long-Term Pain

The consequences of this treasury share sale must be weighed carefully. While there is a clear, immediate benefit, the potential long-term negative impacts are substantial.

The Upside: A Temporary Lifeline

The primary positive outcome is the injection of 1.6 billion KRW. This capital can temporarily alleviate the pressing liquidity crunch, fund daily operations, and perhaps even be used to partially service debt. It buys the company precious time to address its deeper operational and financial challenges.

The Downside: Share Dilution and Negative Signaling

The most significant risk for existing shareholders is share value dilution. By increasing the number of shares in circulation, the ownership stake and potential earnings per share for each existing shareholder are reduced. While a 1.29% increase may seem minor, it sets a precedent for future capital raises that could further dilute value. Moreover, this action serves as a public admission of financial distress, which can spook investors, damage market confidence, and attract short-sellers, putting further downward pressure on the 101670 stock price.

Investor Guidance: A Prudent Action Plan

In light of this analysis, a highly cautious and defensive investment strategy is warranted. The Hydrolithium treasury stock disposal is a symptom of a larger illness, not a cure.

- •Adopt a ‘Hold/Suspend’ Stance: Given the extreme financial instability, initiating a new position is highly risky. Existing investors should consider a ‘Neutral’ or ‘Hold’ position, avoiding further capital allocation until there is clear evidence of a fundamental turnaround.

- •Monitor Key Turnaround Metrics: Closely watch for tangible progress. This includes how the newly raised funds are utilized, resolutions regarding the convertible bond defaults, and any concrete revenue generation from the secondary battery business.

- •Prioritize Rigorous Risk Management: Acknowledge the high probability of further stock price volatility. This event underscores the company’s severe financial risks, and any investment should be managed with extreme caution. For more on this topic, see our guide on Analyzing High-Risk Tech Stocks.

Frequently Asked Questions

What is Hydrolithium’s recent treasury stock disposal decision?

On October 1, 2025, Hydrolithium announced a plan to sell 700,000 treasury shares (about 1.29% of total shares) to raise approximately 1.6 billion KRW for operating and facility funds.

How might this disposal affect Hydrolithium’s stock price?

While providing a short-term cash infusion, the sale is a strong indicator of financial distress. This can negatively impact investor sentiment, dilute existing shareholder value, and ultimately place downward pressure on the stock price.

Is Hydrolithium a good investment right now?

No, Hydrolithium is currently a high-risk investment. The company is in a very unstable financial position, and the treasury stock disposal does not solve its fundamental problems. A conservative ‘Hold’ or ‘Neutral’ stance with rigorous risk management is advisable until a clear and sustainable turnaround is evident.