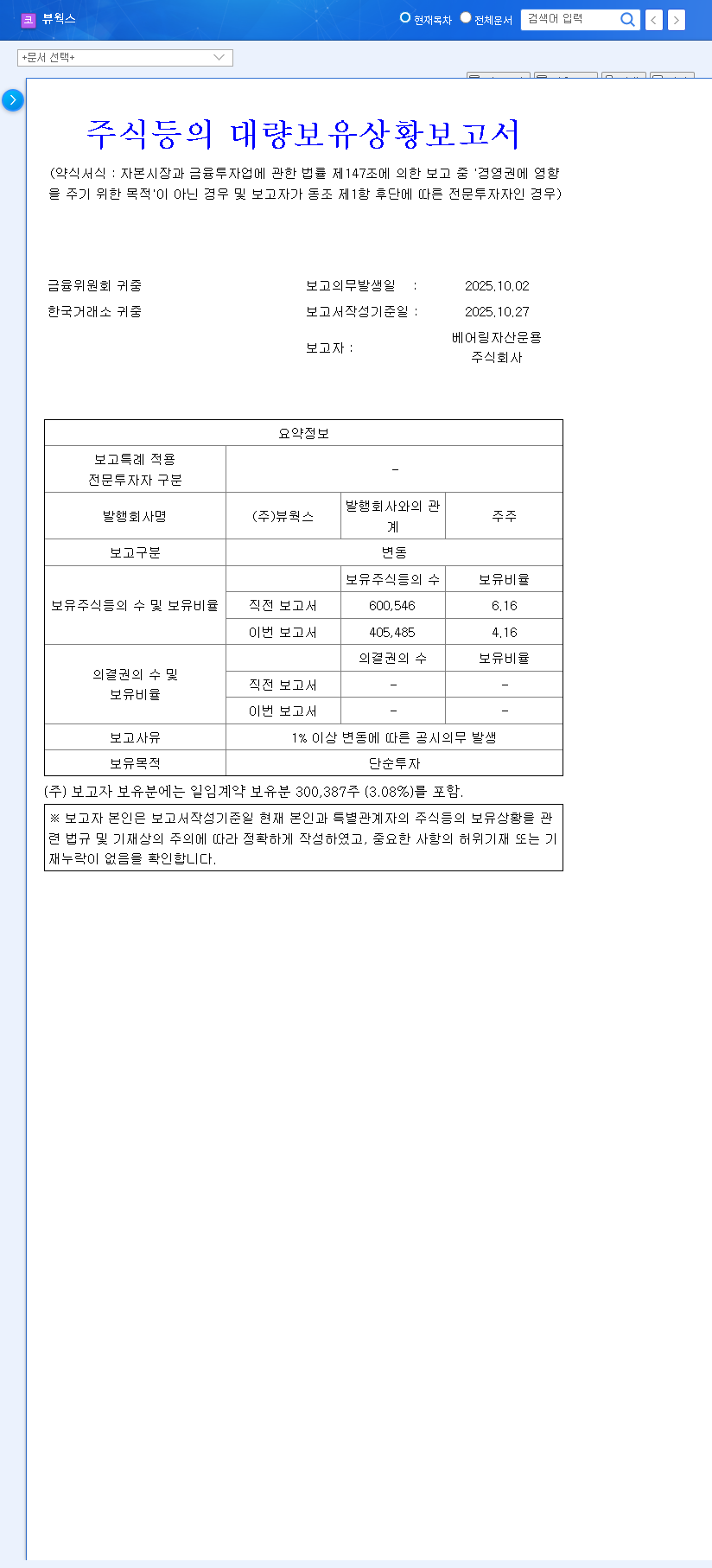

This comprehensive Vieworks stock analysis for 2025 addresses a critical question shaking investor confidence: is a major stakeholder’s recent share reduction a warning sign? On November 7, 2025, a significant disclosure revealed that Bearings Asset Management, a prominent institutional investor, cut its stake in Vieworks Co., Ltd. from 6.16% to 4.16%. This 2-percentage-point drop, officially documented in a ‘Report on the Status of Large Shareholdings’ (Official Disclosure), has naturally created apprehension about the company’s future performance.

Is this a strategic portfolio rebalance, or does it point to underlying weakness? To answer this, we will perform an in-depth analysis of Vieworks’ fundamentals, using its H1 2025 report as our guide. By examining its business performance, financial health, and the broader macroeconomic landscape, we aim to provide a clear, data-driven perspective for current and potential investors in Vieworks Co., Ltd.

Unpacking Bearings Asset Management’s Stake Reduction

The disclosure filed on November 7, 2025, confirmed that Bearings Asset Management‘s holding in Vieworks fell below the 5% threshold, a key reporting level. The shares were held within two specific funds: the ‘Bearings High Dividend Balanced 60’ and ‘Bearings High Dividend’ funds. The stated purpose of the holding was ‘simple investment.’ While this term suggests the investment was not for management control, a significant reduction by a respected institution often triggers market uncertainty and can lead to short-term selling pressure as retail investors follow the institutional lead.

Fundamental Health: A Vieworks Stock Analysis of the H1 2025 Report

To determine if Bearings AM’s move is justified by company performance, we must look directly at the numbers and strategic initiatives outlined in the Vieworks H1 2025 report. The company’s health appears multifaceted, with strong growth in some areas and notable risks in others.

Core Business Performance and Growth Drivers

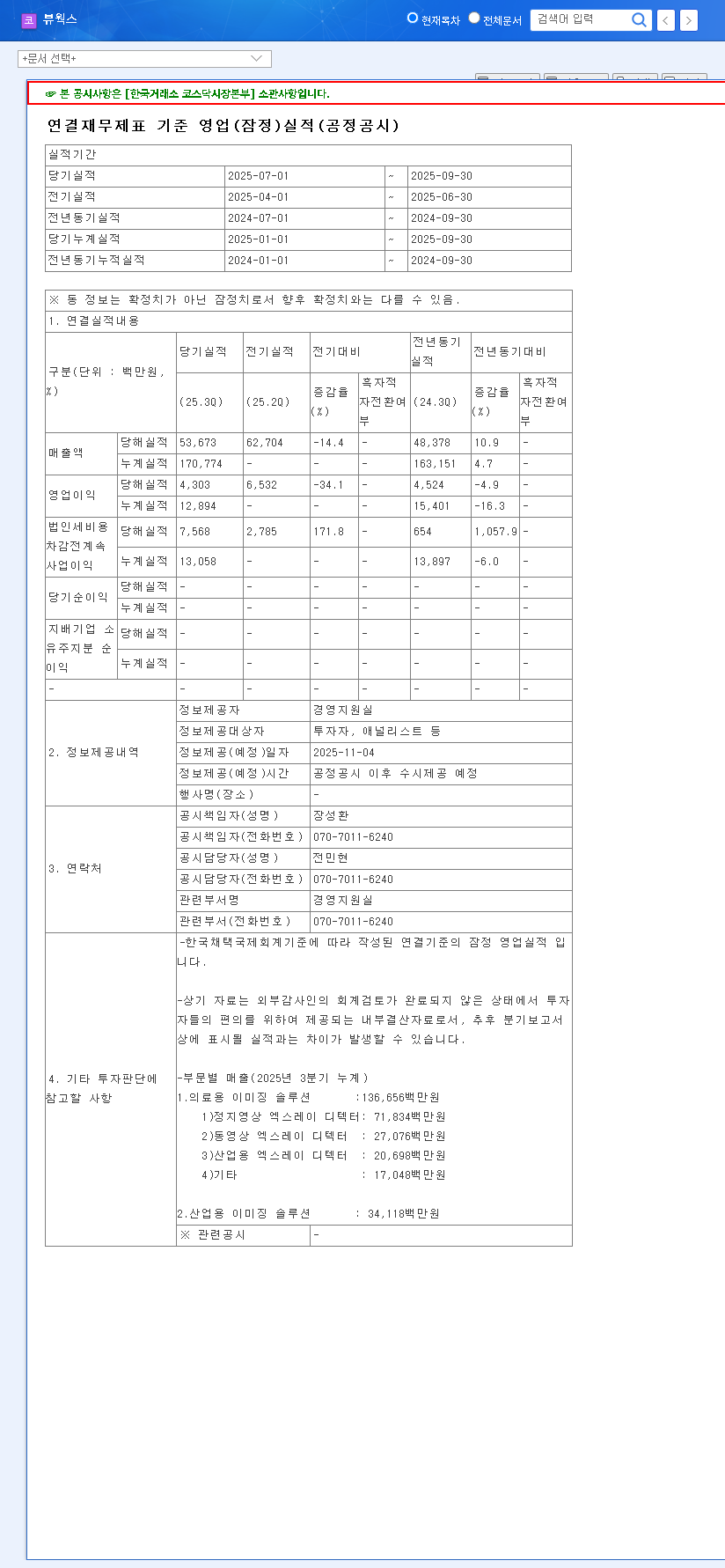

Vieworks operates in the high-tech space of digital imaging solutions, primarily serving the medical (79% of business) and industrial (21%) sectors. In the first half of 2025, the company generated revenue of KRW 117.1 billion and an operating profit of KRW 8.6 billion.

- •Industrial X-ray Detectors: This segment was a standout performer, posting a significant revenue increase fueled by new client acquisition and robust market demand, particularly in sectors like non-destructive testing for EV batteries.

- •Medical Imaging Solutions: While facing slight negative growth, the medical division maintained its stable market position, demonstrating resilience in its core revenue stream.

- •Industrial Cameras: This unit showed stable growth, a commendable feat considering the contraction in the broader machine vision market.

Strategic R&D and Future Markets

Vieworks is actively investing in future growth. A key development is the approval of its high-resolution digital slide scanners, marking a strategic entry into the burgeoning digital pathology market. This move aligns with growing healthcare trends favoring digitization for faster, more accurate diagnostics. For more information, you can read our deep dive into the digital pathology market.

Financial Health and Potential Risks

While the top line is growing, the balance sheet reveals areas requiring caution:

- •Higher Leverage: The debt-to-equity ratio increased from 36.36% to 47.33%, indicating greater reliance on borrowing to fund operations and expansion.

- •Currency & Interest Rate Exposure: As a major exporter, a 10% change in exchange rates could swing pre-tax profit by KRW 7.4 billion. Similarly, a 1% change in interest rates could alter interest expenses by KRW 0.75 billion.

- •Liquidity Management: With KRW 93.4 billion in financial liabilities due within one year, effective short-term liquidity management is critical.

Interpreting the Market’s Reaction

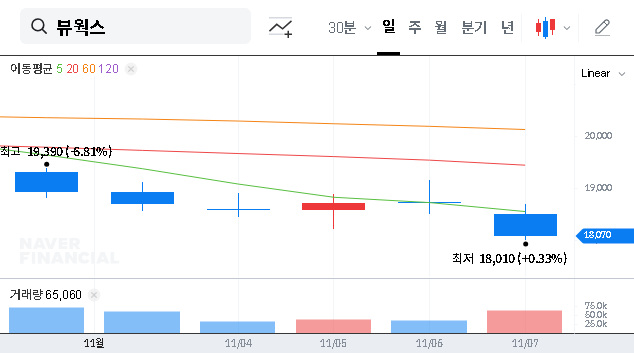

The sale by Bearings Asset Management could be interpreted in two primary ways. Firstly, it could be seen as a negative signal, increasing short-term selling pressure and making other investors cautious. However, it’s equally plausible that the sale is unrelated to Vieworks’ fundamentals. It could be a simple act of profit-taking or a portfolio rebalancing act within the specific Bearings funds. Understanding these dynamics is key; you can learn more about institutional investor strategies from authoritative sources like Reuters.

Despite short-term market noise from the stake sale, the core of this Vieworks stock analysis suggests the company’s long-term value hinges more on its fundamental performance and strategic execution than on one institution’s portfolio adjustment.

Comprehensive Outlook and Investor Takeaways

Investors should weigh the short-term supply/demand pressure against the company’s medium-to-long-term growth trajectory. The key is to focus on fundamental milestones rather than reacting to headlines.

Key Factors to Monitor:

- •Future Earnings Reports: Pay close attention to profitability in the new digital pathology segment and continued growth in industrial detectors.

- •Institutional Investor Flow: Track whether other institutions are buying or selling, which will provide a broader sentiment indicator.

- •Macroeconomic Indicators: Keep an eye on exchange rates and interest rate policies, as they directly impact Vieworks’ bottom line.

- •Debt Management: Look for signs of deleveraging or effective management of the company’s increased financial liabilities in upcoming quarters.

In conclusion, while the Bearings AM stake sale is a notable event causing temporary headwinds, Vieworks’ robust fundamentals, particularly its growth in key industrial sectors and strategic entry into new markets, suggest a resilient long-term outlook. Prudent investors will monitor the key factors listed above to make informed decisions.