The semiconductor landscape is buzzing, and at the center of the conversation is Chips&Media, Inc., a leading semiconductor IP company that just posted impressive preliminary third-quarter 2025 earnings. After navigating a challenging start to the year, the company has demonstrated a remarkable recovery, driven by the powerful momentum of its Chips&Media AI NPU IP (Neural Processing Unit Intellectual Property). This surge not only surpasses market expectations but also solidifies the company’s position as a key player in the future of on-device AI.

This in-depth analysis unpacks the latest Chips&Media earnings report, explores the revolutionary technology behind its success, and provides a comprehensive Chips&Media stock analysis for investors considering its future value.

A Closer Look at the Q3 2025 Earnings Triumph

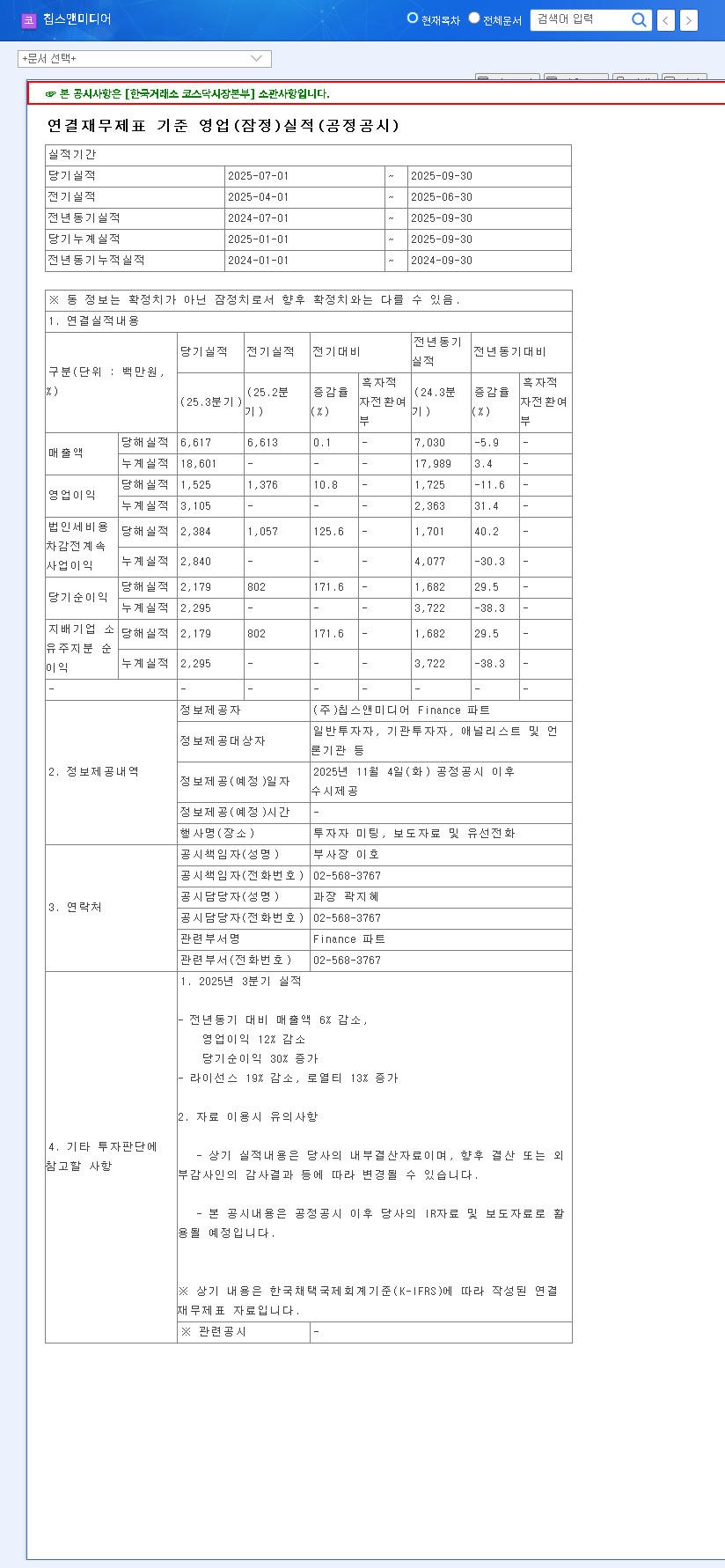

On November 4, 2025, Chips&Media disclosed its preliminary consolidated Q3 earnings, painting a picture of robust financial health and a strong upward trajectory. The numbers speak for themselves, as detailed in their Official Disclosure (DART).

- •Revenue: KRW 6.6 billion (Consistent with Q2, demonstrating stability)

- •Operating Profit: KRW 1.5 billion (A healthy increase from KRW 1.4 billion in Q2)

- •Net Profit: KRW 2.2 billion (A massive surge from KRW 0.8 billion in Q2)

This performance marks a significant turnaround from a subdued Q1. The sustained revenue combined with a dramatic leap in net profitability points to improved operational efficiency and the successful commercialization of high-margin products, namely the highly anticipated Chips&Media AI NPU IP.

The Game Changer: Decoding the Chips&Media AI NPU IP Advantage

The stellar Q3 results are not just a financial event; they are a validation of Chips&Media’s strategic pivot towards artificial intelligence. The new growth engine is undoubtedly its proprietary NPU IP, designed for the exploding market of on-device AI. Unlike cloud-based AI which sends data to remote servers, on-device AI performs computations directly on the hardware (like a smartphone or car), offering faster responses, enhanced privacy, and lower operational costs.

Chips&Media’s unique competitive advantage lies in its NPU IP’s ability to process complex AI data without requiring DRAM access. This innovation significantly reduces power consumption and chip size, making it a highly attractive solution for device manufacturers.

The generation of its first license revenue from this technology in 2025 marks a pivotal moment, shifting the Chips&Media AI NPU IP from a promising R&D project to a tangible, revenue-generating asset that fuels future growth.

Investment Outlook: Chips&Media Stock Analysis

For investors, these earnings have both immediate and long-term implications. Understanding the context of the broader semiconductor IP market is crucial.

Short-Term Momentum

The significant beat on net profit is likely to generate positive investor sentiment and create upward pressure on the stock price. The clear evidence of the AI NPU IP business contributing to the bottom line could attract a new wave of investors focused on the AI sector.

Mid-to-Long-Term Value Proposition

The long-term appeal is even more compelling. Chips&Media is positioning itself perfectly to capitalize on the growth of on-device AI, a market projected to grow exponentially. Key factors for long-term growth include:

- •Stable Core Business: The company’s leadership in video codec IP (HEVC, AV1) provides a stable revenue stream, particularly from the Chinese market, which funds innovation.

- •Expanding AI Portfolio: As the company secures more design wins for its NPU IP, royalty revenues will begin to layer on top of license fees, creating a highly profitable, recurring revenue model.

- •Attractive Fundamentals: Continuous performance improvements strengthen the company’s balance sheet and overall investment appeal.

Navigating Potential Risks

No investment is without risk. Investors should monitor macroeconomic variables like KRW/USD exchange rate fluctuations, which can impact an export-heavy company. Furthermore, the global semiconductor market is notoriously competitive and cyclical. Competition from larger players like Arm and Synopsys in the NPU space, as discussed by industry analysts at Gartner, remains a key factor to watch.

Frequently Asked Questions (FAQ)

Q1: What is the main takeaway from Chips&Media’s Q3 2025 earnings?

The key takeaway is the significant jump in net profit to KRW 2.2 billion, which signals a major improvement in profitability and validates the company’s strategic investment in its new Chips&Media AI NPU IP business.

Q2: Why is the AI NPU IP business so important for Chips&Media’s future?

It targets the high-growth on-device AI market. Its unique technology, which processes data without DRAM access, offers a powerful competitive advantage in efficiency and cost, positioning the company as a key enabler of next-generation smart devices.

Q3: What should investors monitor going forward?

Investors should track the rate of new customer acquisitions and design wins for the AI NPU IP. Monitoring the competitive landscape and macroeconomic trends like exchange rates and global semiconductor IP demand is also crucial for a complete Chips&Media stock analysis.

Conclusion: A Positive Outlook with Key Variables to Watch

Chips&Media’s Q3 2025 preliminary earnings are unequivocally positive, showcasing a company in a strong recovery phase with a powerful new growth driver. The successful monetization of the Chips&Media AI NPU IP is a critical milestone that improves fundamentals and enhances its long-term corporate value. While investors should remain mindful of market risks, the current trajectory suggests that Chips&Media is well-positioned to carve out a significant niche in the future of artificial intelligence.