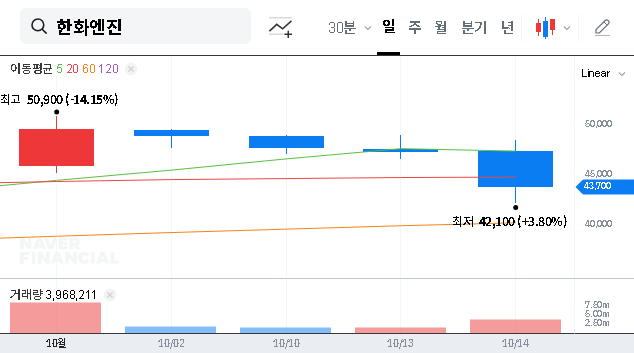

The latest Hanwha Engine Q3 2025 earnings report has presented investors with a complex puzzle. While the company’s revenue and operating profit fell short of market consensus, a surprising and significant outperformance in net profit has added a layer of intrigue. This mixed result raises critical questions for current and prospective shareholders: Is this a sign of underlying weakness or a signal of shrewd financial management? This in-depth financial analysis will dissect the preliminary results, explore the macroeconomic context, and provide a clear investment strategy for navigating the path ahead for Hanwha Engine stock.

Q3 2025 Performance: The Core Numbers

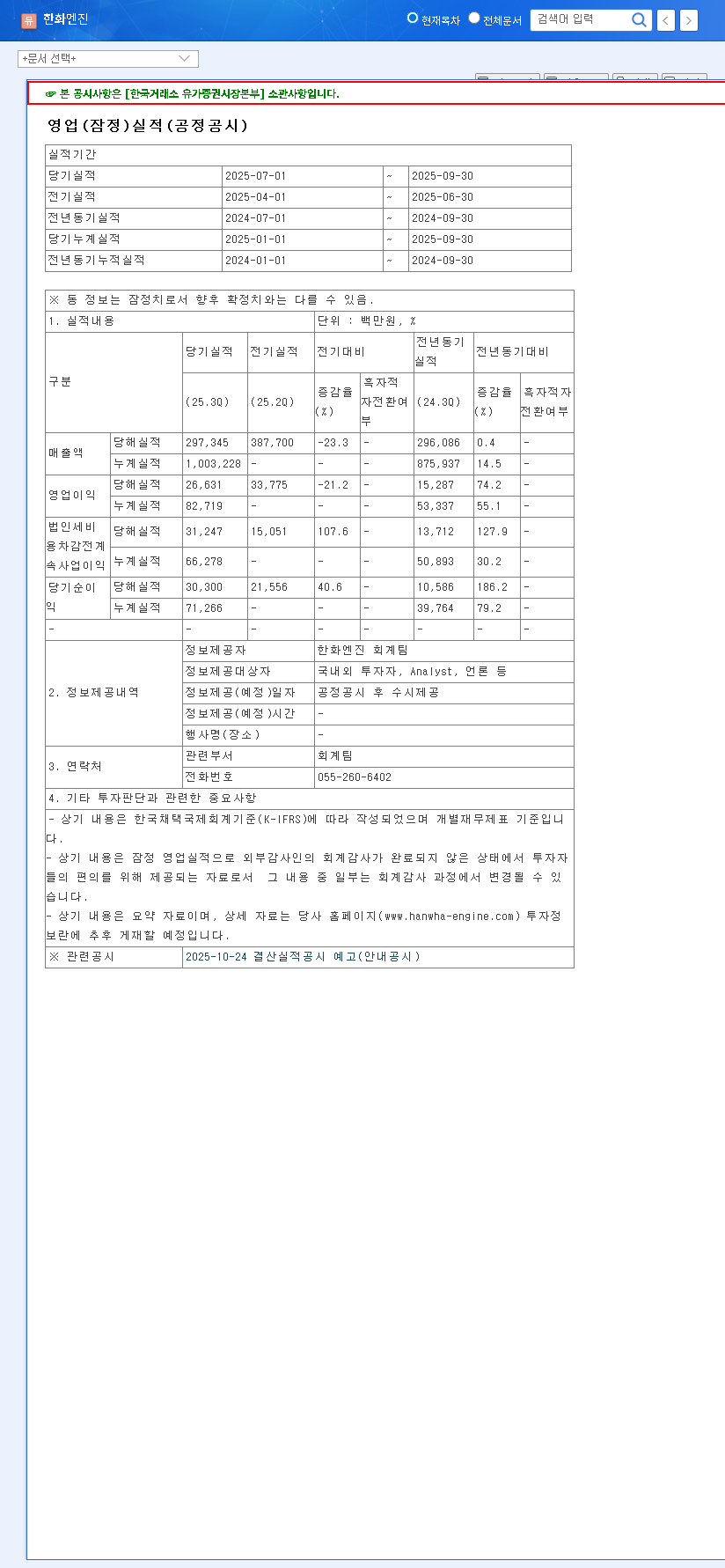

On November 7, 2025, Hanwha Engine Co., Ltd. released its preliminary third-quarter earnings, revealing a divergence between its operational performance and its bottom line. Here are the key figures compared to market expectations:

- •Revenue: KRW 297.3 billion, missing the expected KRW 343.3 billion by 13.0%.

- •Operating Profit: KRW 26.6 billion, falling 9.2% short of the KRW 29.3 billion forecast.

- •Net Profit: KRW 30.3 billion, impressively beating the KRW 25.1 billion expectation by 21.0%.

The central conflict for investors is clear: the operational miss suggests potential headwinds, while the robust net profit hints at financial resilience. Understanding the source of this disparity is key to evaluating the company’s true health.

A Deeper Financial Analysis of the Results

Investigating the Revenue and Operating Profit Shortfall

The miss on the top line (revenue) and operating profit could stoke concerns about the second-half performance outlook. This underperformance is likely tied to several external pressures. A global economic slowdown can dampen demand in the shipping industry, leading to delayed or smaller orders. Furthermore, increased uncertainty in global trade routes and volatile raw material costs can squeeze operating margins. While the company’s order book remains a source of strength, these Q3 results indicate that it is not entirely immune to broader market volatility. This performance dip, following a strong Q2, suggests a reaction to short-term environmental shifts rather than a fundamental flaw in the business model.

The Story Behind the 21% Net Profit Surprise

The significant outperformance in net profit, despite the operational miss, is the most compelling part of the Hanwha Engine Q3 2025 earnings story. This suggests that positive non-operating factors played a crucial role. Potential contributors include effective cost-cutting measures in selling, general, and administrative (SG&A) expenses, favorable foreign exchange gains due to currency fluctuations, or other one-off financial gains. While a positive result, it is critical for investors to determine the quality and sustainability of this profit. A one-time gain is less valuable than a structural improvement in cost management. For a comprehensive breakdown, investors should consult the Official Disclosure (Source: DART).

Long-Term Outlook and Investment Strategy

Fundamental Strengths in the Marine Engine Market

Despite short-term volatility, the long-term fundamentals for Hanwha Engine remain robust. The company holds a powerful position as the world’s second-largest producer of low-speed marine engines. This is particularly significant given the industry-wide shift towards sustainability. As regulations from bodies like the International Maritime Organization (IMO) become stricter, the demand for eco-friendly, fuel-efficient vessels (and their advanced engines) is set to accelerate. Hanwha Engine’s technological capabilities in this area, particularly with its marine engine and SCR (Selective Catalytic Reduction) businesses, position it as a key beneficiary of this multi-decade transition. The ongoing recovery of the global shipbuilding market further solidifies this long-term growth potential.

An Actionable Plan for Hanwha Engine Stock Investors

Given the mixed signals from the Hanwha Engine Q3 2025 earnings, a prudent investment strategy requires careful monitoring and analysis. Investors should focus on the following key areas:

- •Analyze Profit Quality: Dig into the official earnings report to understand the specific drivers of the net profit beat. Distinguish between sustainable cost improvements and one-off gains.

- •Monitor Order Books: Keep a close watch on global shipbuilding order trends, particularly for LNG carriers and other eco-friendly vessels. A strong order backlog is the best indicator of future revenue. For more information, you can learn how to track shipbuilding industry data.

- •Track Macro Indicators: Continue to monitor macroeconomic variables such as exchange rates (KRW/USD), interest rates, and key shipping indices (e.g., Baltic Dry Index). These factors will continue to influence the company’s costs and the overall health of the marine engine market.

In conclusion, while the Q3 2025 report may cause some short-term downward pressure on Hanwha Engine stock, the company’s long-term growth trajectory appears intact. The unexpected net profit beat provides a cushion, but the focus must remain on the core operational performance and the robust, long-term industry trends that favor the company. Diligent investors who look beyond the headline numbers will be best positioned to make informed decisions.