This comprehensive HCT CO., LTD. earnings analysis explores the company’s provisional Q3 2025 results, revealing a fascinating story of rising profitability despite a slight revenue dip. For investors tracking the 072990 stock analysis, understanding the dynamics behind these figures is crucial. HCT, a key player in the testing, certification, and calibration industry, has presented a complex picture that warrants a deeper look into its fundamentals, market position, and future prospects. We will dissect these results to provide clear, actionable insights for your investment strategy.

HCT’s Q3 2025 Earnings at a Glance

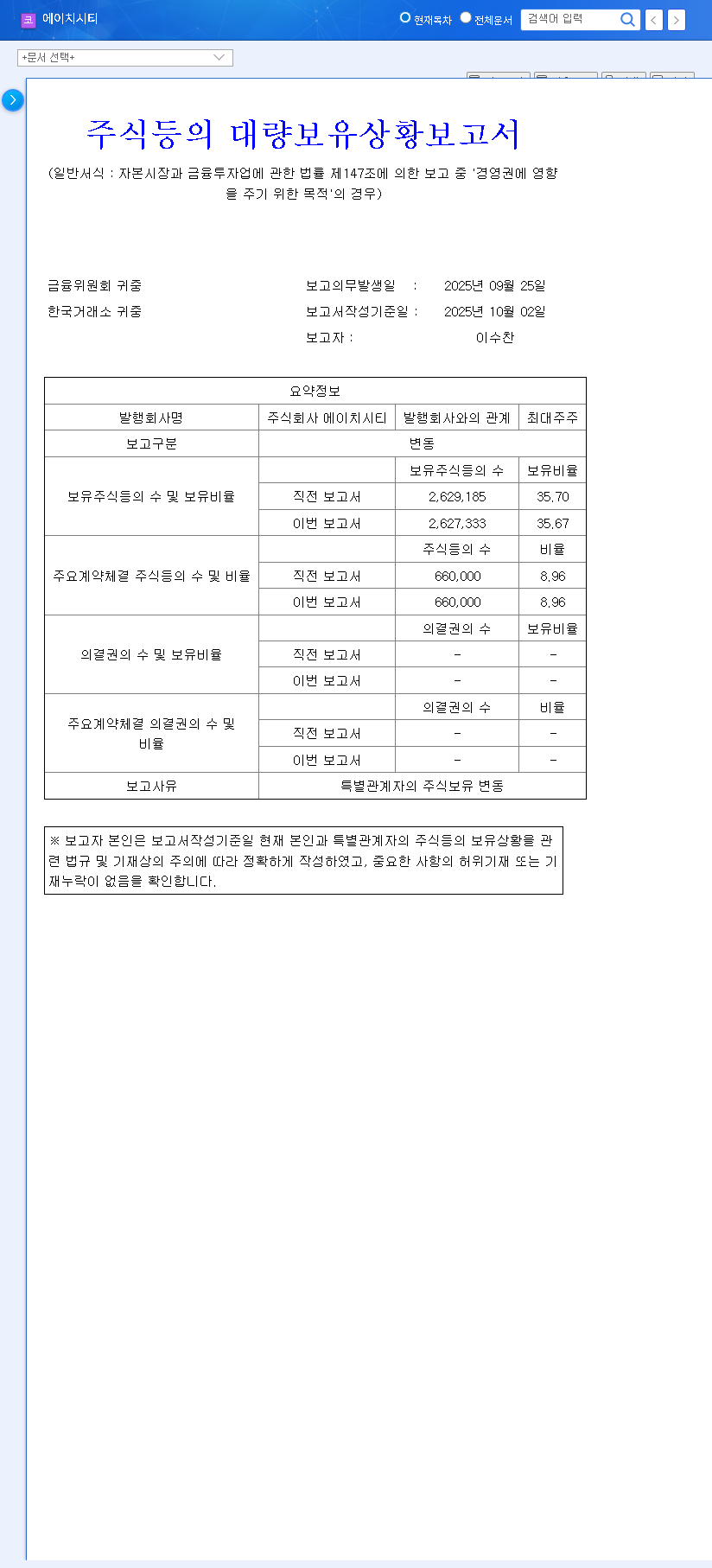

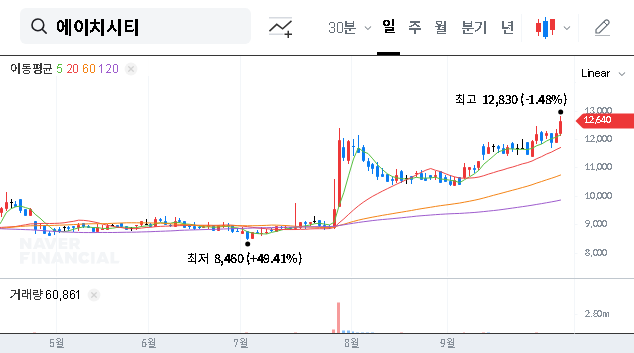

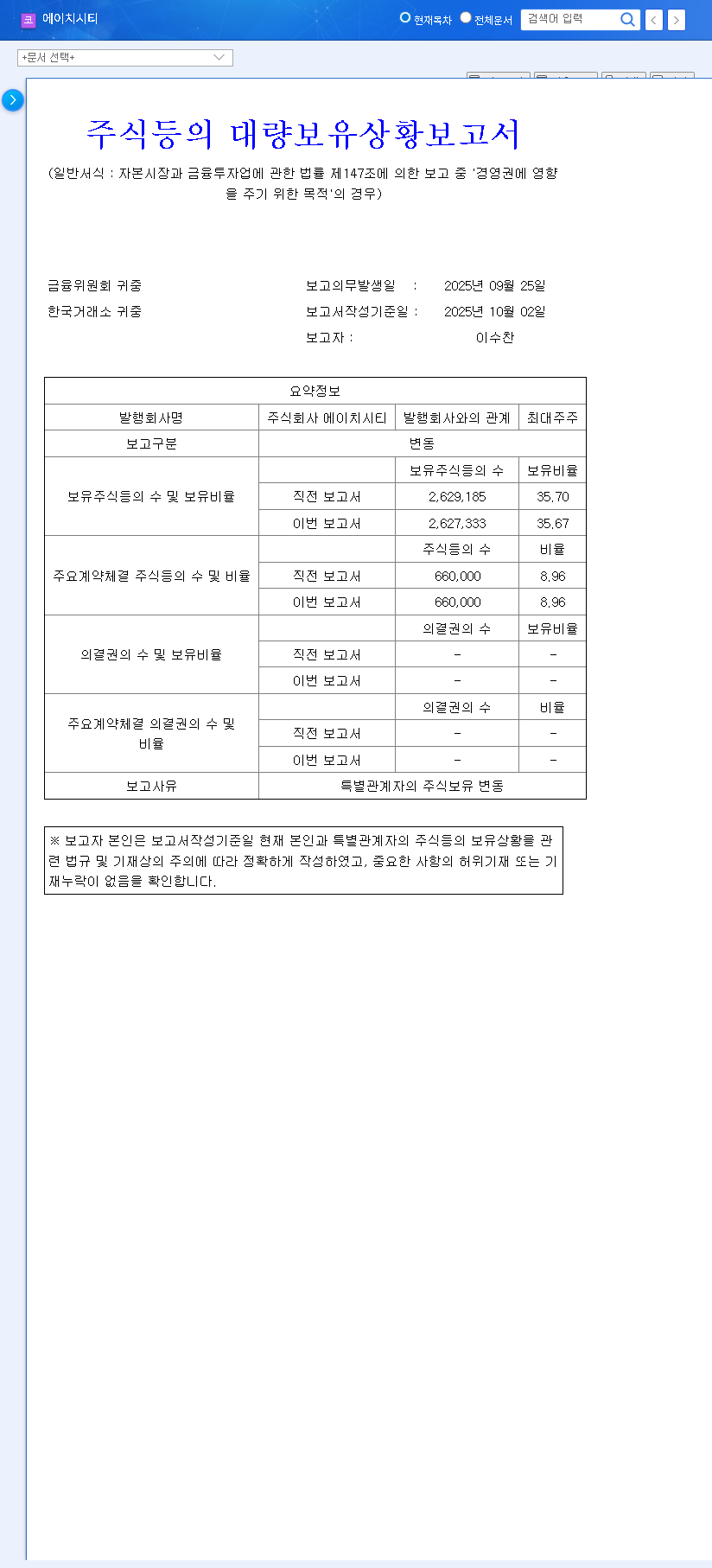

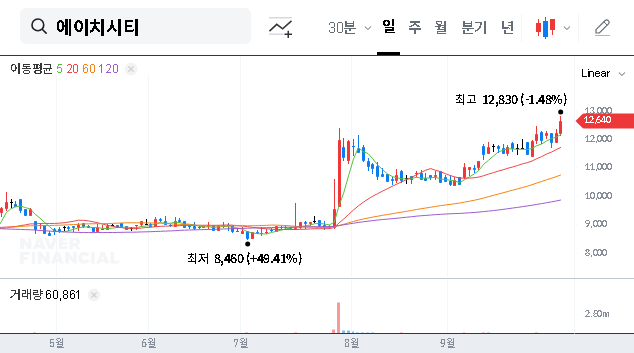

HCT CO., LTD. announced its provisional consolidated financial statements for the third quarter of 2025, showing resilience in its bottom line. The key metrics from the report signal a strategic focus on profitability and operational efficiency. You can view the full report directly from the Official Disclosure (DART).

- •Revenue: KRW 28.1 billion (a slight decrease from KRW 29.2 billion in Q2 2025)

- •Operating Profit: KRW 4.5 billion (down from KRW 5.0 billion in Q2 2025)

- •Net Income: KRW 3.5 billion (an increase from KRW 3.3 billion in Q2 2025)

The most notable takeaway is the growth in net income, which indicates improved margin performance or effective cost management. This continues the positive trend of profitability since the company recovered from a net loss in Q4 2024, a significant milestone for investor confidence.

The paradox of declining revenue against rising net income signals a potential shift towards higher-margin services and improved operational efficiency, a key positive indicator for long-term investors.

In-Depth Analysis: The Factors Driving Performance

Core Business Strengths & Corporate Fundamentals

HCT’s foundation remains solid, built upon the evergreen demand for testing and certification. This is amplified by several key strengths:

- •Diverse Industry Demand: HCT serves critical sectors like ICT, automotive, battery technology, and defense, creating a stable and diversified revenue stream.

- •New Technology Catalyst: The proliferation of 5G, autonomous driving, and electric vehicles creates a continuous need for new, complex testing, positioning HCT as a direct beneficiary of technological advancement.

- •Strategic Diversification: The expansion into the non-clinical CRO (Contract Research Organization) business through H&H Bio opens up a new, high-growth avenue in the biotech sector.

- •Financial Health: With a manageable debt-to-equity ratio of 66.04% and healthy operating cash flow, the company’s financial structure is robust enough to weather economic shifts.

Market Conditions & External Headwinds

The broader market presents both opportunities and challenges. The global testing, inspection, and certification (TIC) market is projected to grow, driven by stricter safety and environmental regulations. However, investors must consider macroeconomic risks:

- •Intense Competition: The TIC industry is competitive, which could put pressure on pricing and margins over time.

- •Economic Volatility: Fluctuations in currency exchange rates (KRW/USD, KRW/EUR) and rising interest rates can impact foreign asset values and increase the cost of borrowing.

- •Customer Concentration: A dependency on a single major customer (over 30% of revenue) is a notable risk that requires ongoing diversification efforts.

Investment Thesis: A Cautiously Optimistic Outlook

Our HCT investment guide concludes with a ‘Buy’ rating, balanced by careful consideration of the associated risks. The company’s ability to grow its net income in a challenging quarter underscores its operational strength and strategic acumen.

Key Investment Points

- •Durable Core Business: The non-discretionary nature of testing and certification provides a stable foundation for growth.

- •Future Growth Engines: The CRO business and investments in automation technology represent significant long-term growth catalysts.

- •Global Expansion: HCT’s established global network is a key asset for capturing growth in international markets.

Conclusion: Positioned for Sustained Growth

The HCT CO., LTD. Q3 2025 earnings report reaffirms the company’s solid fundamentals and promising future. While the slight revenue dip and external risks require monitoring, the improvement in net income and strategic growth initiatives paint a positive picture. HCT appears well-positioned to navigate market challenges and continue its growth trajectory, making it a compelling stock for investors with a long-term horizon. For more on this sector, read our guide on Understanding the Testing and Certification Industry.

Disclaimer: This analysis is based on publicly available information. Investment decisions should be made at the sole discretion of the investor. We assume no legal responsibility for any investment outcomes.