A significant development has emerged for HANSUNG CLEANTECH CO., LTD. (066980), a company navigating a period of financial turbulence. The announcement of a massive new ultrapure water contract has injected a wave of optimism, but it comes against a backdrop of declining revenue and investor skepticism. The critical question for investors is whether this contract is a sustainable turning point or merely a temporary reprieve.

This comprehensive analysis will dissect the contract’s impact on HANSUNG CLEANTECH stock, evaluate the company’s precarious financial health, and provide an actionable framework for making an informed investment decision. We’ll explore the company’s core business, the market dynamics, and the essential factors to monitor moving forward.

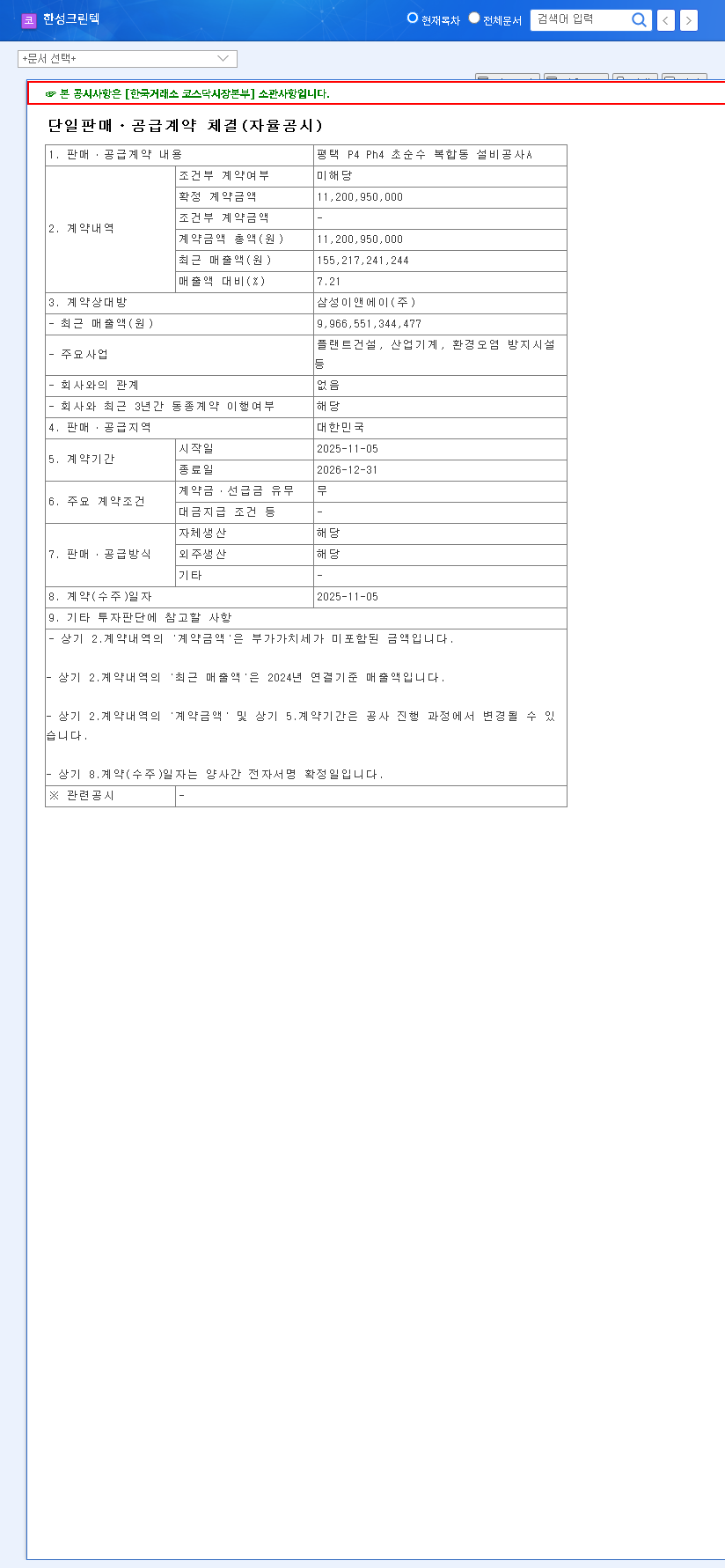

The Landmark ₩11.2 Billion Samsung E&A Contract

On November 5, 2025, HANSUNG CLEANTECH officially disclosed a pivotal agreement with Samsung E&A Co., Ltd. for the ‘Pyeongtaek P4 Ph4 Ultrapure Water Complex Facility Construction A’. (Source: Official Disclosure). The contract is valued at ₩11.2 billion, a figure that represents approximately 180% of the company’s entire 2024 revenue. The project is scheduled to run for over a year, from November 2025 to the end of December 2026, promising a sustained revenue stream.

The Critical Role of Ultrapure Water

To grasp the significance of this deal, it’s essential to understand ultrapure water (UPW). UPW is water purified to an exceptionally high standard, removing virtually all contaminants. It is a non-negotiable, mission-critical component in the semiconductor manufacturing process, where even the smallest impurity can ruin entire batches of microchips. Securing a major UPW facility contract with a global leader like Samsung reaffirms HANSUNG CLEANTECH’s technical expertise in a highly demanding field.

A Deep Dive into HANSUNG CLEANTECH’s Financial Health

This new contract doesn’t exist in a vacuum. It arrives at a time when HANSUNG CLEANTECH’s financial foundations have been severely weakened, a crucial part of any 066980 analysis.

Persistent Performance Decline

- •Shrinking Revenue: A consistent downward trend from ₩11.4 billion (2022) to just ₩6.27 billion (2024).

- •Plummeting Profits: Operating profit collapsed from ₩1.75 billion (2022) to a mere ₩0.19 billion (2024).

- •Net Losses: The company fell into a net loss of ₩1.28 billion by the end of 2024, with losses projected to continue.

Eroding Investor Trust and Financial Soundness

The company’s stability metrics are equally concerning. The Debt-to-Equity ratio climbed from 92% to over 114%, while the Current Ratio, a key measure of liquidity, fell drastically from 340% to a precarious 58% in the same period.

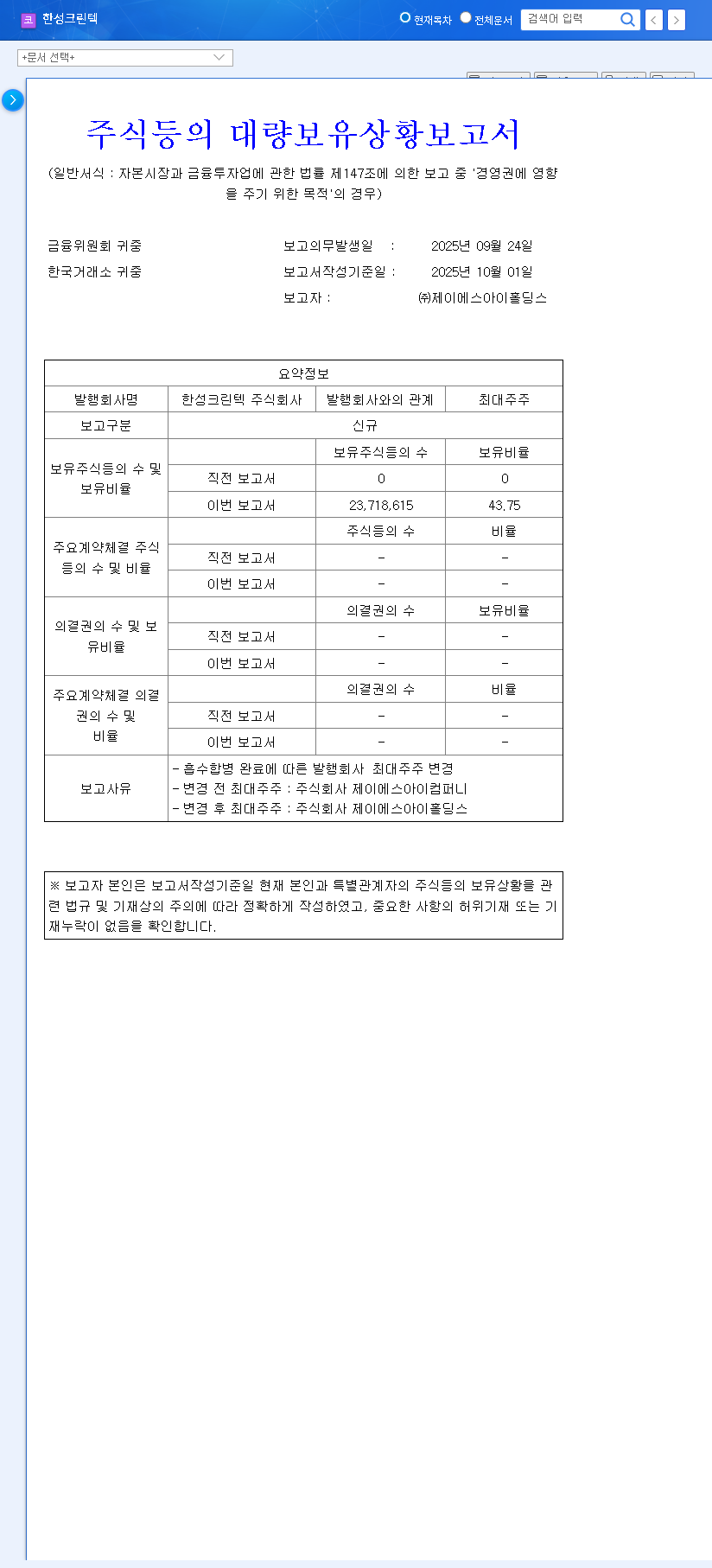

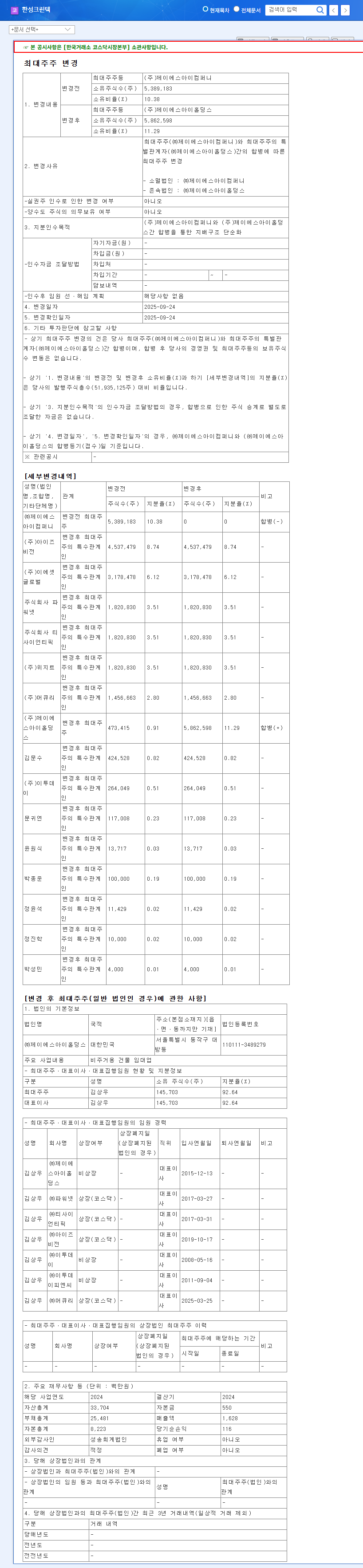

Compounding these issues was a major financial statement restatement, which revealed a ₩28.2 billion overstatement in 2024 revenue. This correction led to a staggering restated operating loss of ₩50.73 billion, severely damaging investor confidence in the company’s accounting and governance.

Investment Outlook: Hope vs. Hurdles

The new ultrapure water contract is undeniably a powerful positive catalyst. It provides a much-needed revenue infusion, reinforces the company’s market position, and offers a clear path toward improved financial performance in 2025-2026. However, long-term success for HANSUNG CLEANTECH depends on overcoming significant challenges.

While this is a domestic contract with limited direct exposure to currency fluctuations, broader macroeconomic factors like high interest rates and volatile material costs remain a risk. The primary hurdle, however, is internal: rebuilding trust and demonstrating consistent, transparent financial management.

Actionable Plan for Investors

Given the balance of strong positive momentum and significant underlying risks, a cautious but watchful approach is warranted. For those considering an investment in HANSUNG CLEANTECH stock, here is a checklist of key areas to monitor.

- •Track Contract Execution: Scrutinize quarterly reports in 2025 and 2026 to verify that revenue from the Samsung E&A contract is being recognized as planned and contributing positively to the bottom line.

- •Monitor Governance Improvements: Look for clean auditor opinions and company announcements regarding the strengthening of internal accounting controls to ensure past mistakes are not repeated.

- •Assess New Business Development: Sustainable long-term growth will require more than one large contract. Watch for efforts in business diversification and new market penetration.

For more general guidance, you can also read our guide on how to analyze industrial technology stocks.

Investment Opinion: We maintain a “Neutral” rating. The potential for a turnaround is real, but the risks associated with its past financial instability are too significant to ignore. The rating will be re-evaluated as the company demonstrates tangible progress in its financial performance and governance.

Frequently Asked Questions (FAQ)

What is the new contract secured by HANSUNG CLEANTECH?

HANSUNG CLEANTECH secured a ₩11.2 billion contract with Samsung E&A for the construction of an ultrapure water facility at the Pyeongtaek P4 site, a project almost double its 2024 revenue.

How will this contract impact HANSUNG CLEANTECH’s finances?

It is expected to significantly boost revenue and profitability in 2025 and 2026, potentially serving as a crucial catalyst for improving the company’s deteriorating financial health.

What are the main risks for HANSUNG CLEANTECH stock?

The key risks are the company’s history of financial underperformance, poor liquidity, and the severe erosion of investor trust stemming from a major financial statement restatement issue.