The recent announcement regarding the new Huvitz Shareholder Return Policy has certainly captured the market’s attention. Huvitz Co., Ltd. (KRX: 065510), a key player in the ophthalmic medical device industry, has committed to a more generous dividend payout, signaling a focus on shareholder value. However, for astute investors, the headline is just the beginning. The real question is whether this policy is a sustainable promise built on solid financial ground or a risky maneuver in the face of underlying challenges. This comprehensive Huvitz stock analysis drills down into the company’s latest financial reports to uncover the full picture.

We will dissect the feasibility of this enhanced dividend policy, examine the warning signs in the company’s fundamentals, and outline the critical risk factors every investor must consider before making a decision on Huvitz stock.

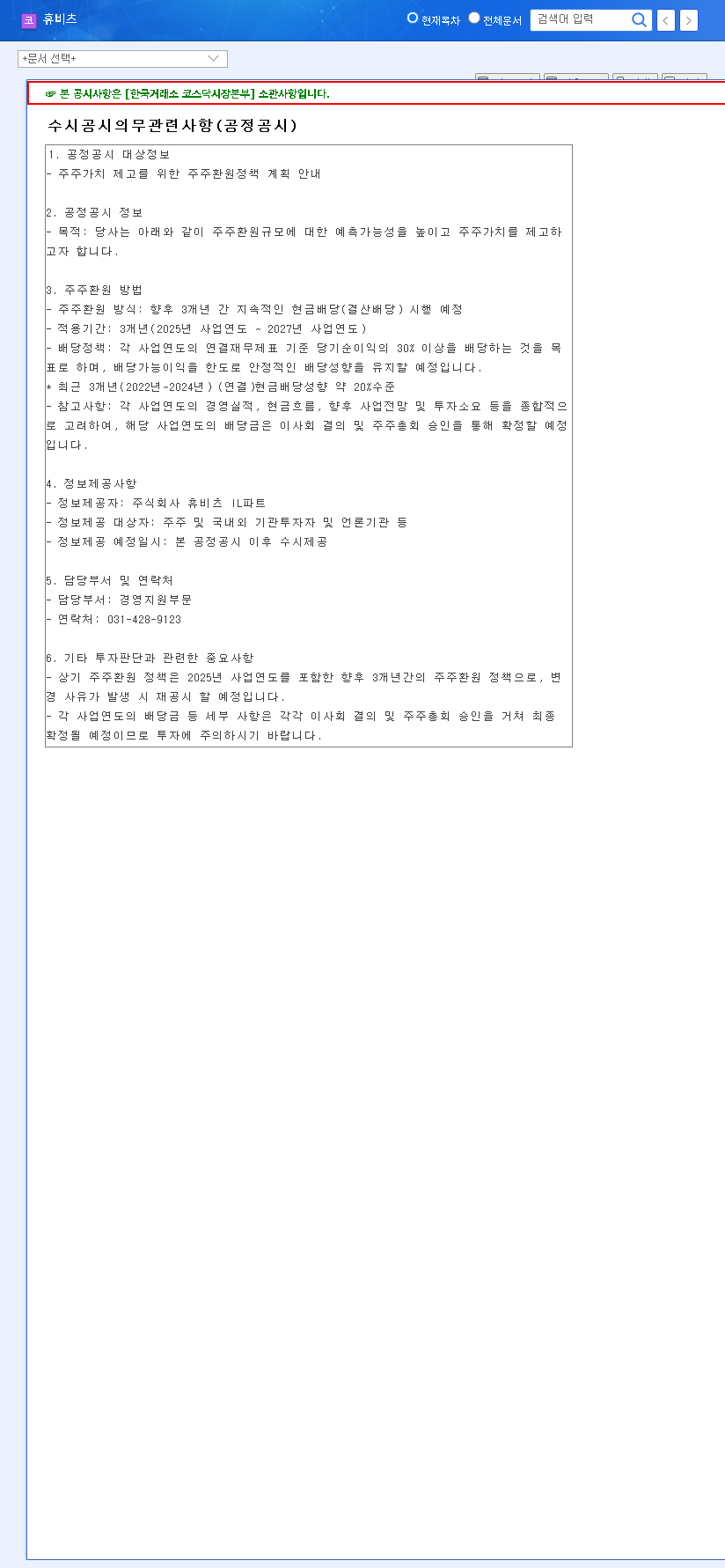

The New Huvitz Dividend Policy: What’s on the Table?

Huvitz has officially unveiled a forward-looking shareholder return plan for the fiscal years 2025 through 2027. The core of this policy is a commitment to a cash dividend payout ratio of 30% or more of its consolidated net profit. This is a notable increase from the average 20% payout ratio seen in the preceding years (2022-2024). On the surface, this move is a clear and positive signal of management’s intent to reward long-term investors. You can view the complete details in the Official Disclosure (DART).

Fundamental Diagnosis: A Look Under the Hood at H1 2025

While the policy is forward-looking, its viability depends entirely on current and future financial performance. The H1 2025 report reveals several areas of concern that challenge the optimistic outlook.

The Shadow of Slowed Growth & Worsening Profitability

- •Stagnant Revenue: H1 2025 revenue came in at KRW 59.02 billion, a marginal year-on-year increase. This figure, representing only about half of the full-year 2024 revenue, points to a significant growth slowdown. A major red flag is the sharp revenue decline from its Chinese subsidiary (Shanghai Huvitz), indicating severe market weakness in a key growth region.

- •Plummeting Profits: Operating profit fell by a staggering 40% year-on-year. Consequently, the operating profit margin collapsed from 8.7% to just 5.1%. This deterioration is attributed to sluggish sales combined with rising costs of goods sold and administrative expenses.

- •R&D Investment: A silver lining is the company’s continued high investment in research and development, which stands at 19.52% of revenue. While this pressures short-term profits, it is essential for long-term competitiveness and innovation.

Financial Health Warning Signs

An analysis of the balance sheet reveals a weakening financial structure. While total assets saw a slight increase, total liabilities grew more significantly due to a rise in short-term borrowings. This has pushed the net debt ratio higher, raising concerns about the company’s financial soundness. Since 2023, key indicators like net profit margin and ROE (which was negative in 2023) show a clear downward trend, signaling that urgent improvements are needed.

While the promise of higher dividends is appealing, investors must weigh this against the clear deterioration in Huvitz’s underlying financials. Prudence is paramount in this scenario.

A Double-Edged Sword: Potential Impacts of the Policy

The enhanced Huvitz shareholder return policy presents both opportunities and significant risks that investors must carefully balance.

Potential Positives

- •Improved Investor Sentiment: The policy clearly signals a shareholder-friendly management approach, which can boost confidence and attract income-focused investors.

- •Stock Price Support: A reliable and generous dividend can provide a floor for the stock price, offering downside protection in volatile markets.

Significant Risks and Negatives

- •Execution Risk: If profitability continues to decline, Huvitz may be unable to generate sufficient net profit to meet the 30% payout target. A failure to deliver on this promise would severely damage management’s credibility.

- •Increased Financial Strain: With debt levels rising, channeling significant cash toward dividends could further strain the company’s finances, limiting its ability to invest in growth or weather economic downturns.

- •Macroeconomic Pressures: Unfavorable exchange rates (KRW/USD, KRW/EUR), a high-interest rate environment as reported by institutions like Reuters, and elevated logistics costs all pose external threats to Huvitz’s profitability and cash flow.

Comprehensive Analysis & Investment Outlook

Given the conflicting signals, a Neutral investment opinion is warranted. While the shareholder-friendly policy is a positive development, it is overshadowed by the tangible deterioration in Huvitz’s financial performance and rising balance sheet risks.

Investors should proceed with caution and closely monitor the following points:

- •H2 2025 Performance: Look for concrete signs of a turnaround in revenue and profitability, especially in overseas markets.

- •Dividend Execution: Monitor whether the company can actually achieve the stated payout ratio in its next dividend declaration.

- •Financial Ratio Trends: Keep an eye on the debt-to-equity ratio and other key health indicators. For more information, see our guide on analyzing financial statements for medical device companies.

- •Macroeconomic Shifts: Pay attention to changes in exchange rates and interest rates that could impact Huvitz’s bottom line.