The latest ktcs corporation earnings report for the third quarter of 2025 presents a compelling paradox for investors. While headline revenue figures show a decline, a closer look reveals significant year-over-year improvements in both operating and net profit. This signals a strategic shift towards qualitative growth and enhanced operational efficiency. This comprehensive analysis will dissect the Q3 performance, explore the drivers behind its rising profitability, and evaluate the long-term potential of its transformation into an AI Contact Company.

Deconstructing the Q3 2025 Performance

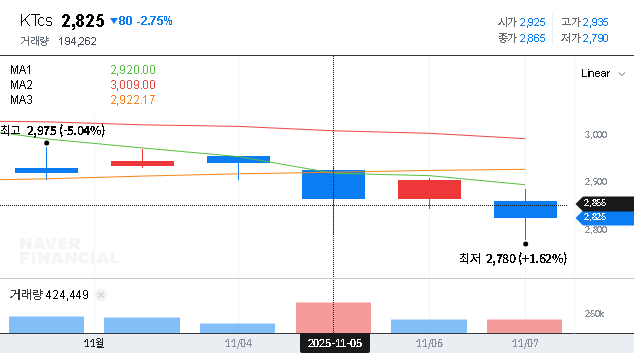

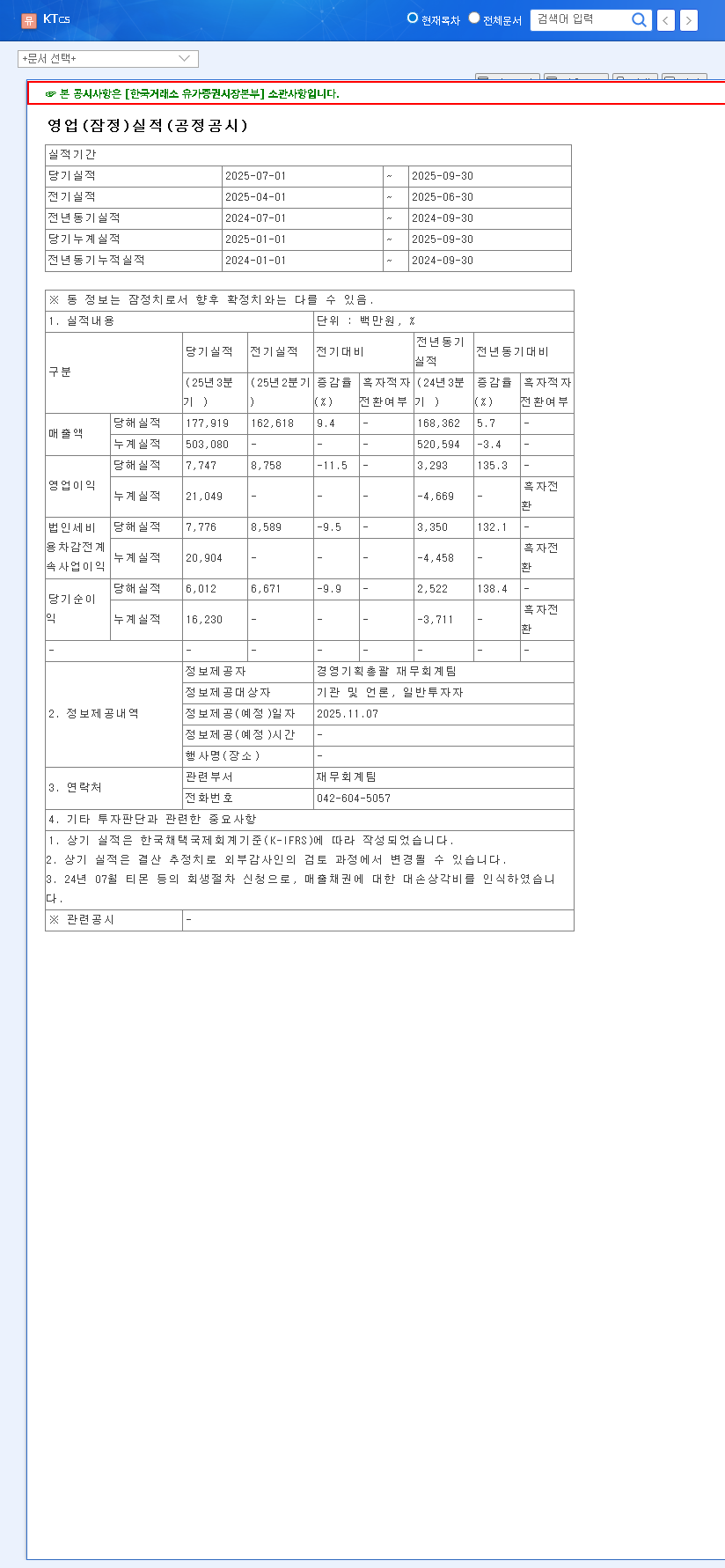

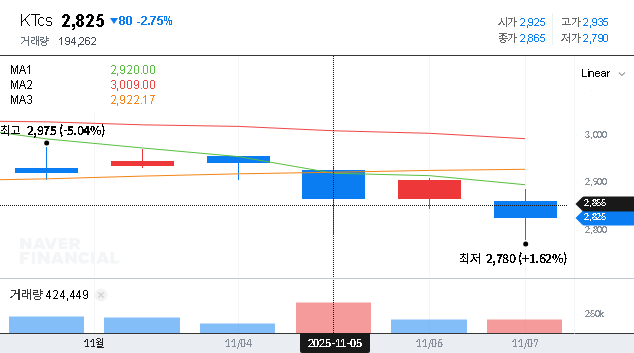

On November 7, 2025, ktcs corporation released its provisional Q3 earnings, providing a mixed but ultimately positive picture of its financial health. The numbers highlight a company in transition, prioritizing sustainable profits over sheer revenue volume.

Key Q3 2025 Financial Metrics:

• Revenue: 177.9 billion KRW

• Operating Profit: 7.7 billion KRW (+2.6B YoY)

• Net Profit: 6.0 billion KRW (+1.9B YoY)

When compared to the previous quarter (Q2 2025), revenue saw a notable decrease of approximately 70 billion KRW. This decline can be largely attributed to persistent weakness in the distribution business (-64.13%) and B2B sales (-34.40%), a trend also observed in our analysis of H1 2025 performance. However, the year-over-year comparison tells a more optimistic story. Despite maintained revenue levels, the sharp increase in operating and net profit demonstrates a successful focus on enhancing profitability and operational leverage.

The Secret to Profitability: A Pivot to Qualitative Growth

The key takeaway from the latest ktcs corporation earnings is the company’s ability to decouple profit from revenue growth. This was achieved through rigorous management efficiency initiatives and stringent cost controls. By strategically reducing exposure to lower-margin business segments and optimizing core operations, ktcs has successfully transitioned from a consolidated loss to a sustained profit, laying a robust foundation for what can be termed ‘qualitative growth’.

AI Contact Company: The Core of the Future Strategy

At the heart of ktcs’s long-term vision is its transformation into an AI Contact Company. This isn’t merely a buzzword; it’s a fundamental shift in their business model. The company is channeling resources into strengthening its AI-powered contact service offerings and establishing a competitive edge in the market. Key initiatives include:

- •Commercialization of ‘HiQri’: This proprietary AICC (AI Contact Center) solution is being rolled out to enhance customer interaction efficiency and provide data-driven insights for clients.

- •Modernizing the 114 Service: The legacy 114 directory assistance service is being revitalized with the integration of AI voice bots, significantly reducing operational costs and improving service stability.

This strategic pivot aligns with broader industry trends, where AI is revolutionizing customer experience management. According to a recent report by Forrester, the market for AI-driven contact center solutions is expected to grow exponentially, placing ktcs in a prime position to capture this demand.

Investor’s Playbook: Analyzing Risks and Opportunities

For current and prospective investors, the Q3 2025 ktcs stock analysis requires a nuanced perspective. While short-term volatility is possible following the earnings announcement, the mid-to-long-term outlook depends on the successful execution of its AI strategy and a turnaround in its traditional business lines. For complete transparency, investors should review the Official Disclosure on DART for raw financial data.

Key Strengths (Bull Case)

- •Proven Profitability: Demonstrated ability to improve profits even with lower revenue points to strong management and a resilient core business.

- •AI Growth Engine: The AICC market provides a significant runway for future growth as its solutions mature and gain market share.

- •Financial Fortress: Debt-free management is a powerful advantage, insulating the company from the financial pressures of a high-interest-rate environment.

- •Strong ESG Credentials: Earning an ‘A’ grade in ESG for four consecutive years appeals to institutional investors and enhances long-term corporate value.

Key Risks (Bear Case)

- •Persistent Revenue Decline: The slump in the distribution and B2B segments requires a clear and effective turnaround strategy to restore top-line growth.

- •Execution Risk: The success of the AI strategy hinges on the company’s ability to successfully commercialize and scale its new technology solutions.

- •Macroeconomic Headwinds: Broader economic uncertainty, including high interest rates and currency fluctuations, could impact client spending and business environment.

Final Outlook & Key Takeaways

The Q3 2025 ktcs corporation earnings paint a picture of a company undergoing a successful and disciplined transformation. While the revenue decline is a concern that needs to be addressed, the impressive improvement in profitability and the clear strategic focus on the high-growth AI sector are highly encouraging. Investors should monitor the tangible revenue contribution from AICC solutions and any signs of stabilization in the distribution business. If ktcs can demonstrate material progress in these areas, it will solidify its case as a compelling long-term investment opportunity at the intersection of stability and innovation.