A significant financial maneuver has placed OSUNG ADVANCED MATERIALS CO., LTD. under the investor spotlight. Korea Bond Investment Management Co., Ltd. recently executed a strategic acquisition of convertible bonds (CBs), securing a new 5.82% stake in the company. While officially designated as a ‘simple investment,’ this move has sent ripples through the market, prompting a deeper look into the company’s future. This analysis will dissect the implications of this convertible bond acquisition, evaluate the core fundamentals of OSUNG ADVANCED MATERIALS, and assess the broader macroeconomic factors at play to provide a comprehensive investment outlook.

The Core Event: A 5.82% Stake via Convertible Bonds

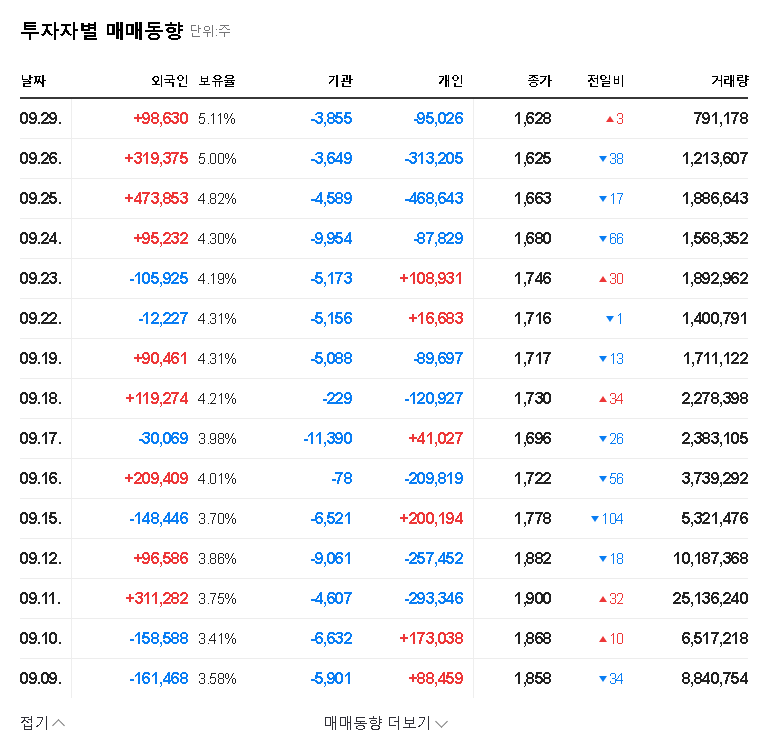

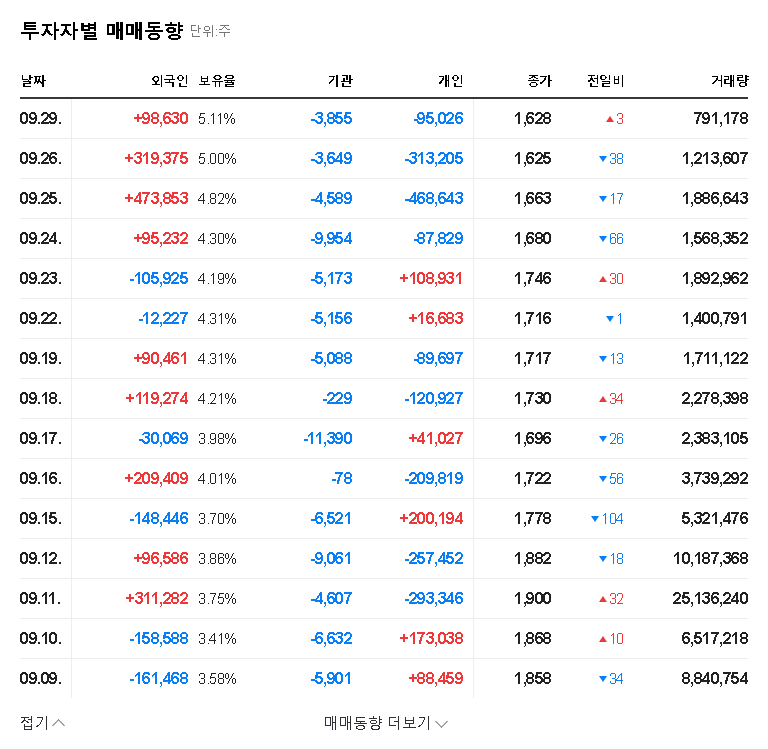

On October 23, 2025, Korea Bond Investment Management acquired convertible bonds of OSUNG ADVANCED MATERIALS, marking a pivotal moment. According to the Official Disclosure filed on October 28, 2025, this transaction shifted their holding from 0% to a notable 5.82%. Understanding this requires knowing what convertible bonds are. Essentially, they are a form of debt that can be converted into a predetermined number of the company’s common stock, offering a hybrid of both debt and equity features. For a more detailed explanation, you can refer to authoritative sources like Investopedia’s guide on convertible bonds.

Key Details of the Transaction:

- •Reporting Entity: Korea Bond Investment Management Co., Ltd.

- •Purpose of Holding: Stated as ‘Simple Investment’.

- •Change in Holding: From 0% to 5.82% post-issuance.

- •Mechanism: Acquisition of company-issued Convertible Bonds.

Deep Dive into OSUNG ADVANCED MATERIALS’ Fundamentals

Beyond this single event, a prudent investor must analyze the company’s underlying health. OSUNG ADVANCED MATERIALS presents a mixed but intriguing picture, characterized by strategic diversification efforts counterbalanced by risks in its legacy operations.

Growth Drivers and Strengths

The company is actively pursuing new growth engines to offset weaknesses in its traditional markets. The acquisitions of Chunji Shipping Co., Ltd. (logistics) and Hwail Pharmaceutical Co., Ltd. (pharmaceuticals) are pivotal steps in this business diversification strategy. These moves are viewed as positive long-term value creators. Furthermore, a stable financial position, underpinned by substantial cash and cash equivalents, provides a solid foundation for these new ventures.

Risk Factors and Weaknesses

Several challenges warrant caution. The core display materials business continues to face declining sales amidst a competitive global landscape. A concerning trend is the reduction in R&D investment, which could jeopardize long-term technological competitiveness—a critical factor in the advanced materials sector. Until the new business segments generate stable, tangible results, the company remains vulnerable to market shifts and the performance of its existing operations.

The primary challenge for OSUNG ADVANCED MATERIALS is managing the transition: leveraging its financial stability to successfully scale new ventures while mitigating the decline in its legacy display materials business.

Navigating Macroeconomic Headwinds

No company operates in a vacuum. The performance of OSUNG ADVANCED MATERIALS is intrinsically linked to several key macroeconomic indicators:

- •Exchange Rate Sensitivity: With significant USD-denominated assets, currency fluctuations are a major factor. A 10% change in the KRW/USD rate is estimated to impact net profit by approximately 2.6 billion KRW. A rising dollar helps exports but inflates the cost of imported raw materials.

- •Interest Rate Environment: A climate of rising interest rates globally increases the cost of capital. This can make future funding more expensive and potentially dampen the company’s appetite for new investments and large-scale expansion.

- •Commodity and Freight Costs: Volatility in raw material prices can squeeze margins in the materials business. Simultaneously, the profitability of its logistics subsidiary, Chunji Shipping, is directly tied to global freight indices like the Baltic Tanker Index, which have shown recent declines.

Investment Outlook and Action Plan

Considering the CB acquisition, the company’s mixed fundamentals, and macroeconomic uncertainties, a cautious yet watchful stance is recommended. The acquisition by Korea Bond Investment Management is not an immediate catalyst for a stock re-rating, but rather a long-term factor to monitor. The potential for future share dilution upon conversion is real, but the immediate impact is limited.

Therefore, the current investment outlook for OSUNG ADVANCED MATERIALS is a ‘Hold’ or ‘Watch’. The company’s strategic diversification is a significant positive, but the risks associated with its core business and the broader economy cannot be ignored.

Key Monitoring Points for Investors:

Investors should keep a close eye on the following developments. For more insights, you might also want to review our complete guide to the advanced materials sector.

- •Any announcement regarding the timing and price of the convertible bond conversion.

- •Quarterly performance reports, focusing on the revenue growth and profitability of the new pharmaceutical and logistics businesses.

- •Changes in the company’s R&D budget and any new technology announcements.

- •Management commentary on the impact of exchange rates and interest rates on earnings.

※ This analysis is for informational purposes only and is based on publicly available data. It does not constitute investment advice. All investment decisions should be made based on your own judgment and research.