The latest SM C&C earnings report for Q3 2025 has sent a clear and concerning signal to the market. For investors tracking SM Culture & Contents Co., Ltd. (048550), the preliminary numbers revealed a significant downturn that goes beyond a simple market miss. The report highlights severe fundamental weaknesses and raises critical questions about the company’s future trajectory. This comprehensive 048550 stock analysis will dissect the results, explore the underlying causes, and provide a clear outlook for investors navigating this turbulent period.

Is this a temporary storm that SM C&C can weather, or are these red flags indicative of a deeper, more systemic crisis? Let’s delve into the data to understand what this earnings shock truly means for your investment portfolio.

Unpacking the SM C&C Q3 2025 Earnings Shock

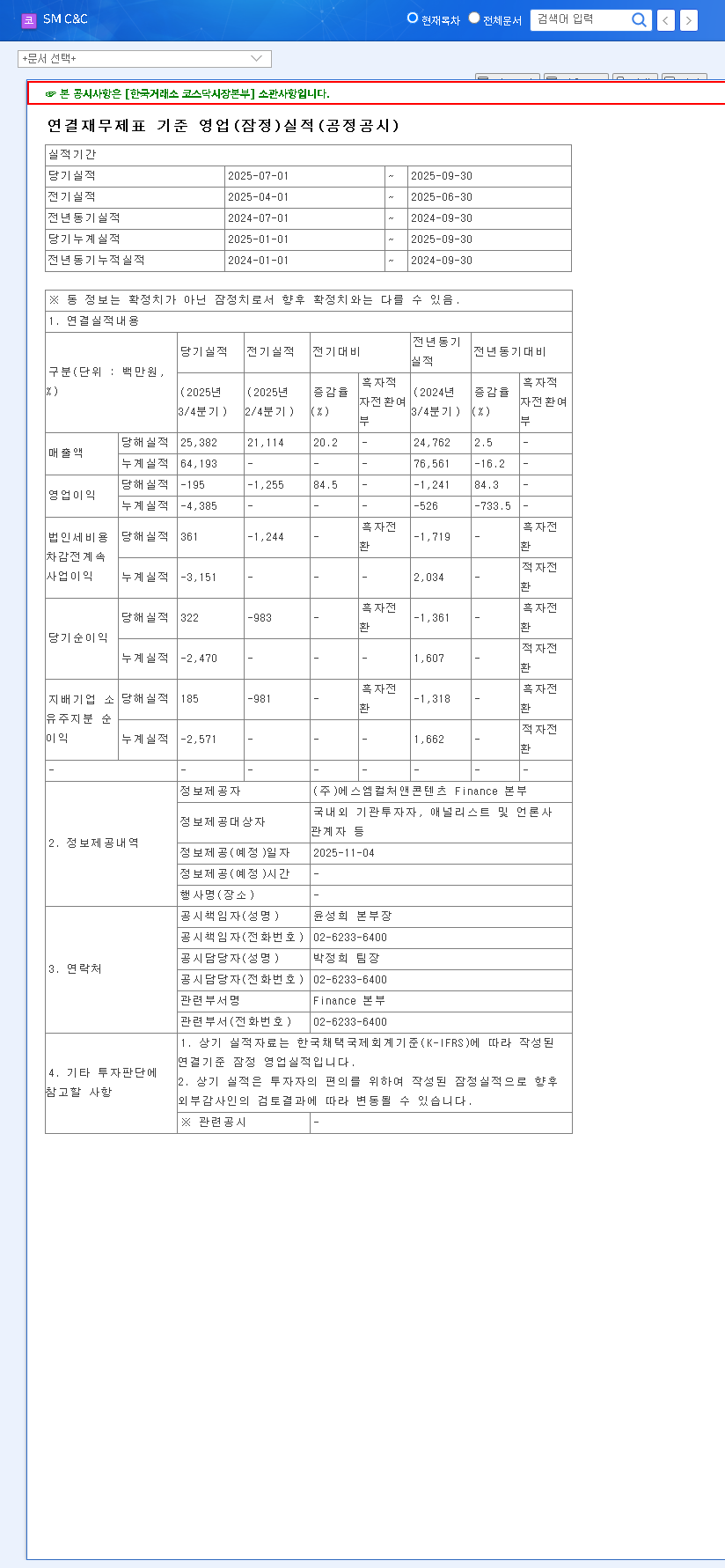

SM Culture & Contents Co., Ltd. announced its preliminary Q3 2025 earnings, posting a revenue of KRW 25.4 billion. However, the headline figures were the operating loss of KRW 0.2 billion and a net income of just KRW 0.2 billion. This performance marks a dramatic deterioration compared to the same period last year, with the crucial operating income metric flipping from profit to loss. The sharp decline in net income also signals a high probability of a full-fledged net loss in the near future. The official figures can be reviewed in the company’s Official Disclosure on DART.

The shift to an operating loss is a significant red flag. It indicates that the company’s core business operations are no longer profitable, even before accounting for taxes and interest expenses.

Historical Performance: A Pattern of Decline

While revenue has seen a marginal increase over the past several quarters, the profitability metrics tell a much darker story. Operating and net income have consistently registered significant losses, painting a clear picture of a deepening profitability crisis. The Q3 2025 operating margin of approximately -0.79% underscores the severity of these challenges, suggesting that the company is spending more to operate than it earns from its sales. For more context, you can review our previous analysis on entertainment sector trends.

Root Cause Analysis: Why is Performance Deteriorating?

This poor SM C&C earnings result is not a one-off event. It’s the culmination of weakening internal fundamentals and challenging external market forces. A closer look at the H1 2025 report reveals the core issues.

1. Severe Erosion of Corporate Fundamentals

- •Widespread Underperformance: H1 2025 revenue fell by a staggering 34.4% year-over-year. This decline wasn’t isolated; it was systemic, affecting all primary business segments, including advertising, entertainment, and travel.

- •Profitability Collapse: The company swung from a KRW 715 million operating profit in H1 2024 to a KRW 4.19 billion operating loss in H1 2025, a clear indicator of a collapsing profit structure.

- •High Fixed Costs: Despite the sharp drop in revenue, Selling, General, and Administrative (SG&A) expenses barely budged. This rigidity in costs is squeezing margins and amplifying losses.

- •Financial Health Risks: A debt-to-equity ratio of 230.13% and a current ratio of just 33.20% (as of year-end 2024) signal significant liquidity risks. This means the company has far more debt than equity and may struggle to meet its short-term obligations.

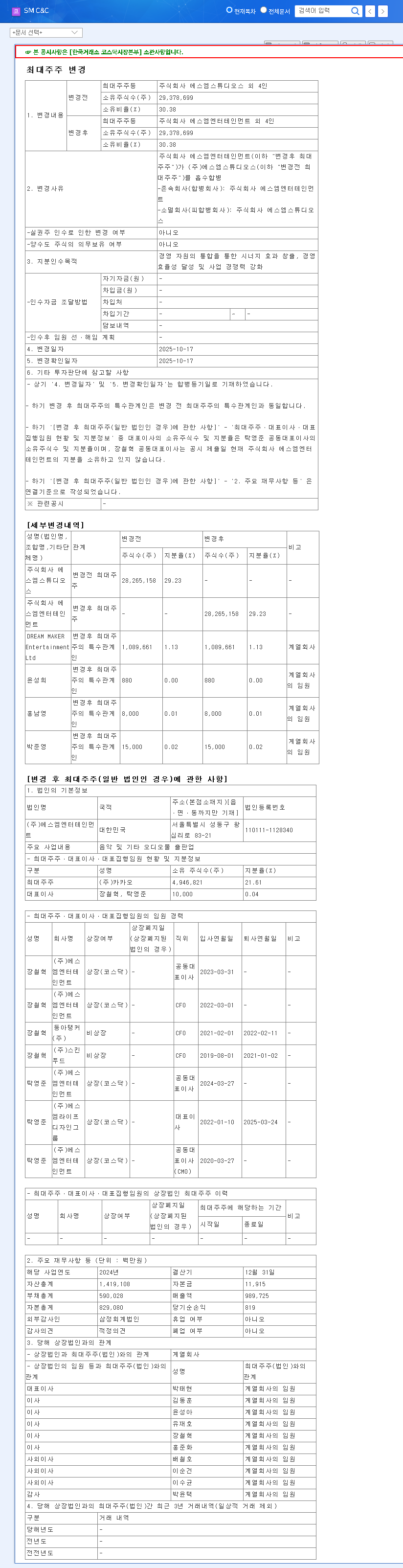

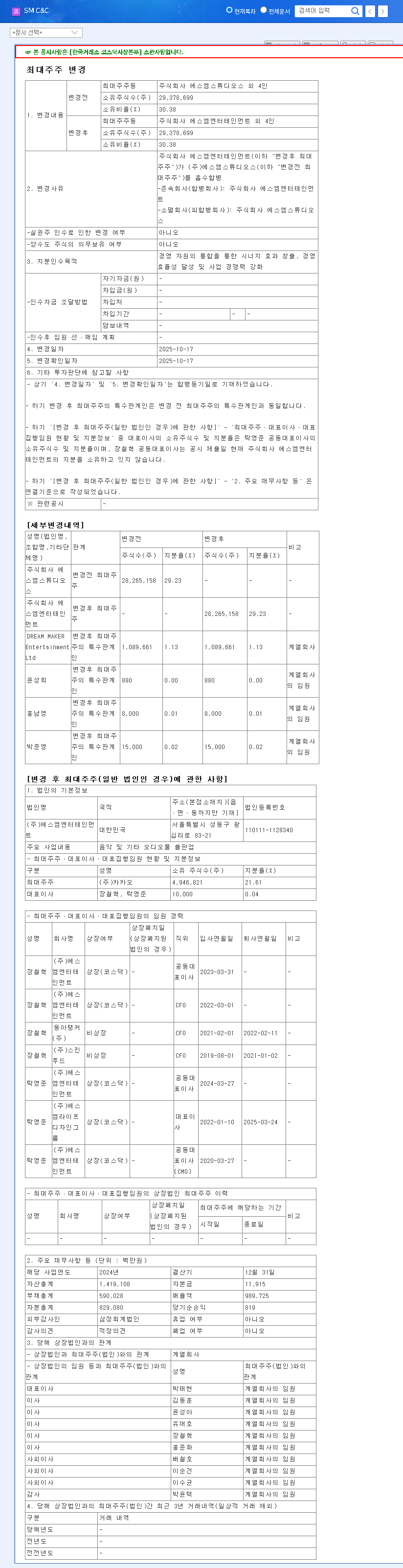

- •Shareholder Uncertainty: The pending merger where SM Entertainment will become the largest shareholder introduces major uncertainty regarding management, strategy, and overall business direction.

2. Unfavorable External Headwinds

The company’s internal struggles are compounded by a difficult external environment. According to industry analysis from sources like Reuters, macroeconomic factors are creating significant pressure.

- •Macroeconomic Pressure: High global interest rates and currency volatility increase borrowing costs and dampen corporate and consumer spending, directly impacting advertising and travel budgets.

- •Intense Competition: The advertising, entertainment, and travel sectors are fiercely competitive. SM C&C’s struggles suggest its competitive advantages have eroded or are insufficient to thrive in the current market.

Investment Outlook: A ‘Sell’ Recommendation

Given the continued underperformance and deeply rooted fundamental weaknesses, the outlook for SM C&C’s stock (048550) is decidedly negative. The latest earnings report will likely intensify downward pressure on the stock price as investor confidence wanes.

Our investment opinion is a firm ‘Sell.’ There is little evidence to suggest a short-term turnaround. Until the company demonstrates a clear and effective strategy for restructuring, cutting costs, and finding new avenues for growth, investors are advised to exercise extreme caution.

Key Factors for Investors to Monitor

For those still considering the stock, here are the critical signposts to watch for potential change:

- •Future Earnings Reports: The upcoming 2025 annual earnings and the 2026 business plan will be vital for gauging any long-term strategic shifts.

- •Synergy from SM Entertainment Merger: Monitor whether the change in ownership leads to tangible synergies, cost efficiencies, and improved corporate value, rather than just more uncertainty.

- •Strategic Initiatives: Look for concrete actions related to business diversification and cost reduction, and track the results of their implementation closely.

This SM C&C earnings analysis is based on currently available data. Any new information or strategic pivots from the company could alter this outlook.