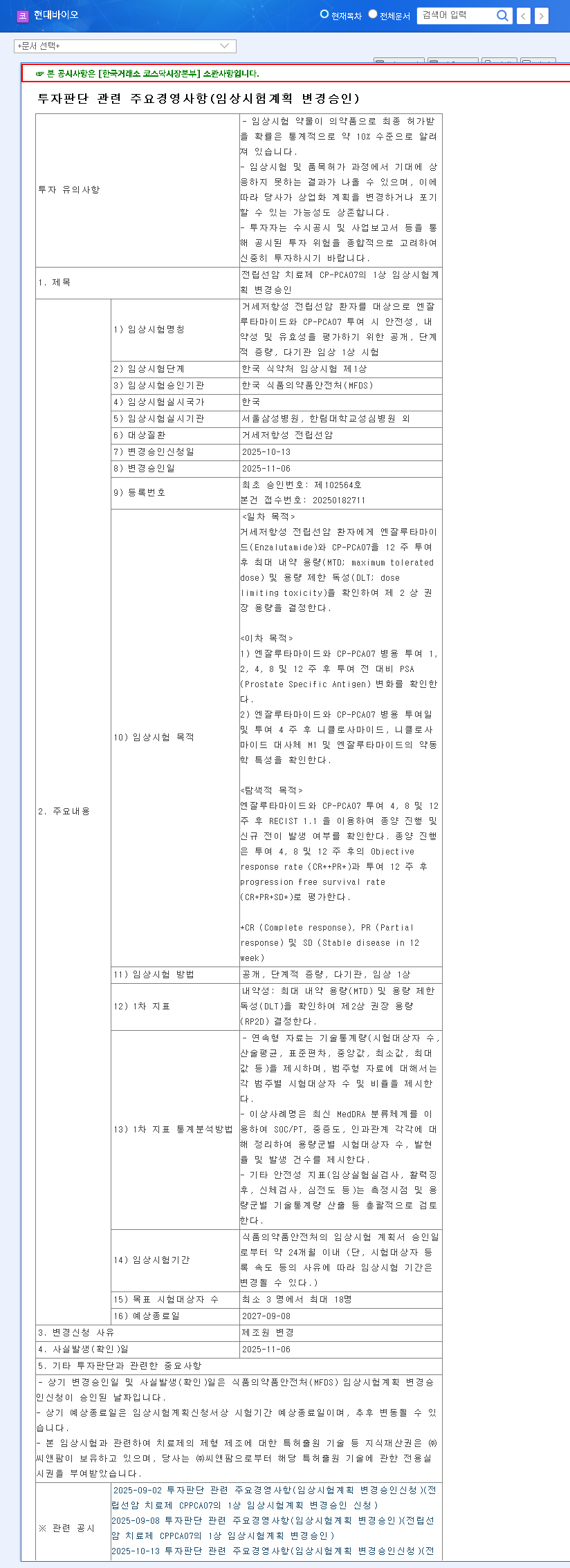

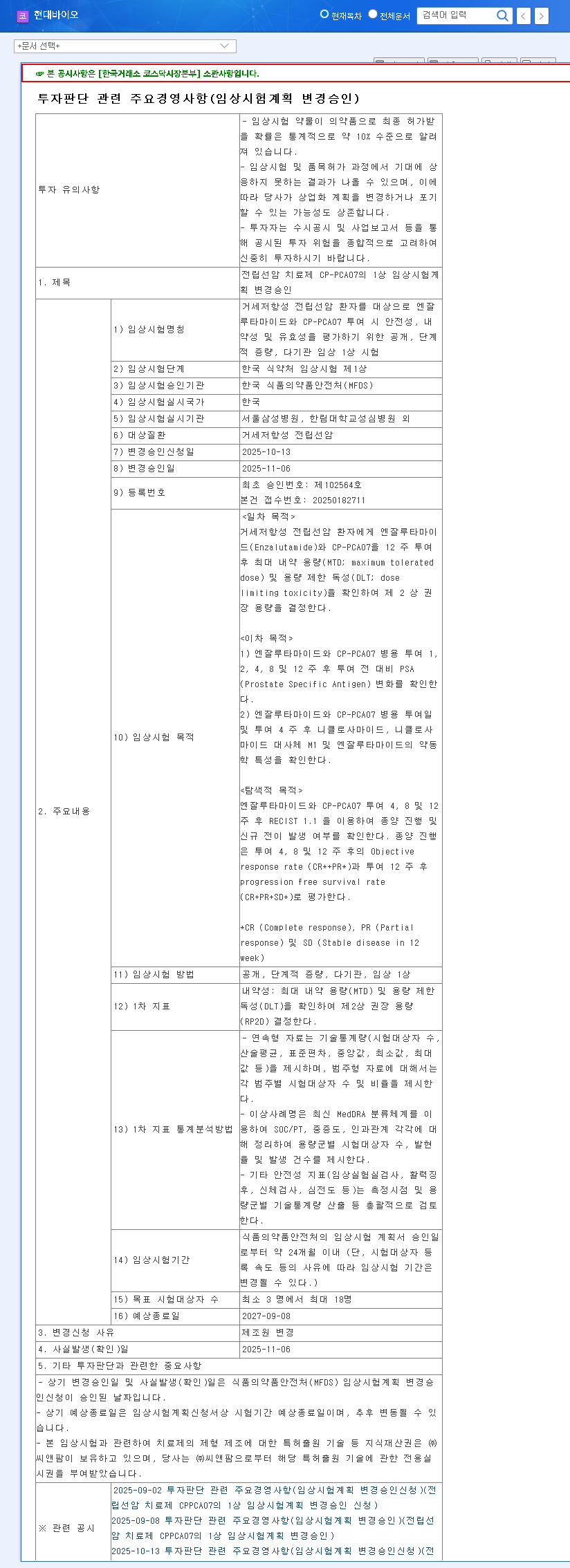

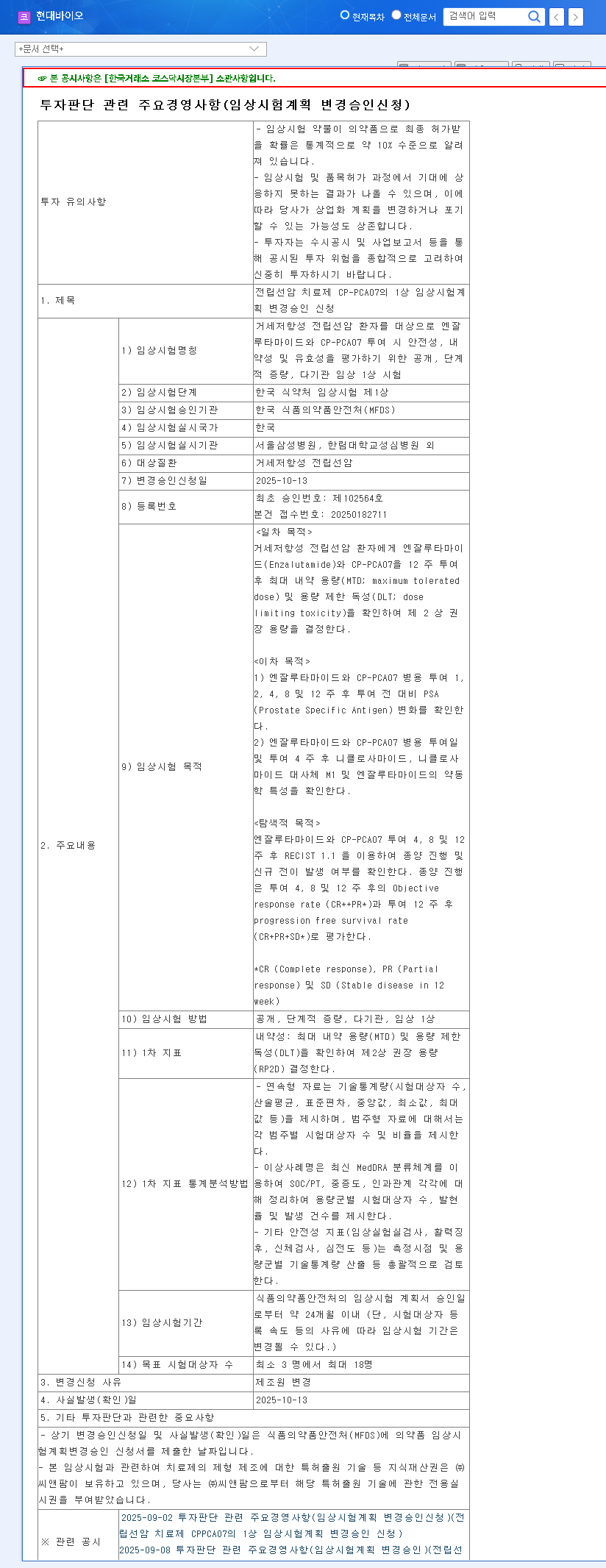

The world of biotech investing is often defined by pivotal moments, and for HYUNDAI BIOSCIENCE, a significant development has emerged. The company recently announced a key amendment approval for the clinical trial of its broad-spectrum antiviral candidate, HYUNDAI BIOSCIENCE CP-COV03, specifically targeting Dengue fever. This news has sparked considerable interest among investors, who are keen to understand the implications for the company’s future and stock value. In this comprehensive analysis, we will dissect this development, exploring the potential upside and the inherent risks to provide a clear roadmap for informed investment decisions.

The Core Development: CP-COV03 Clinical Trial Amendment

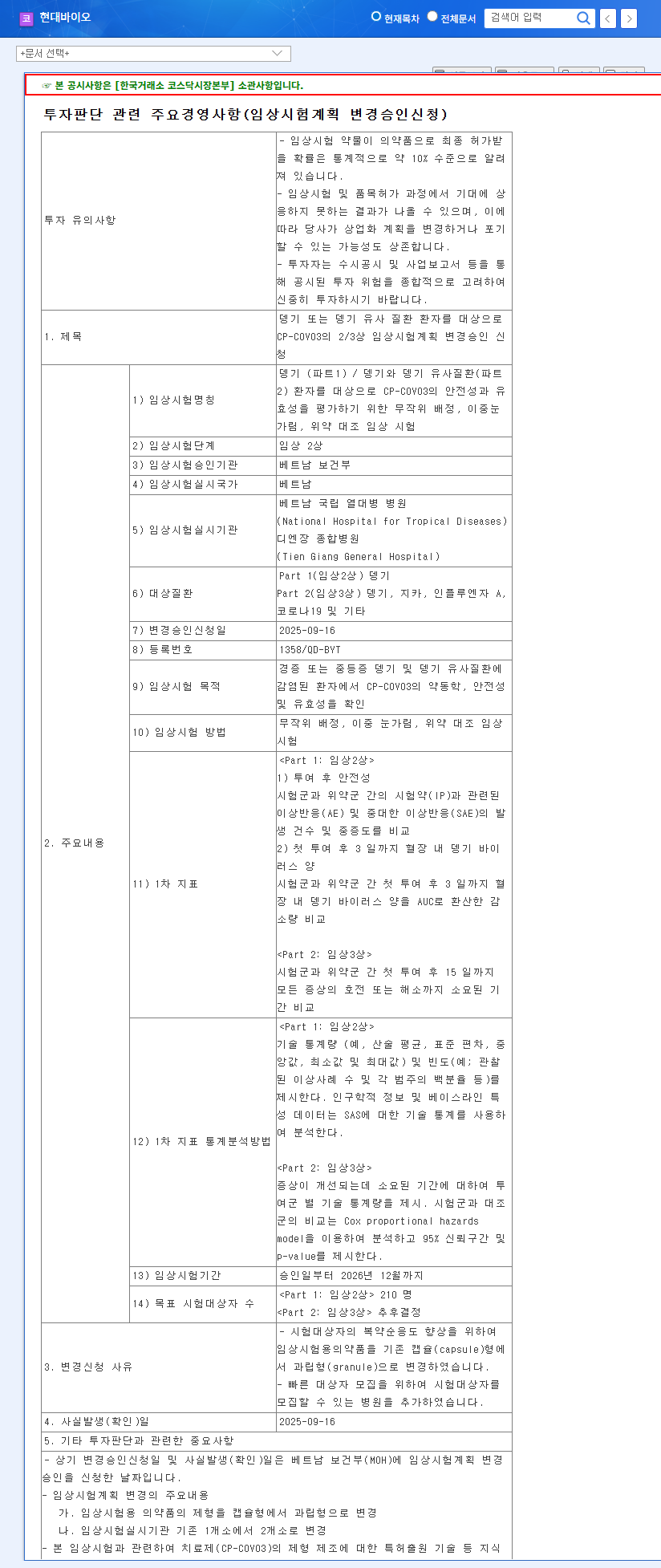

Hyundai Bioscience has secured approval from the Vietnamese Ministry of Health to amend its Phase 2/3 clinical trial plan for CP-COV03. According to the Official Disclosure, this strategic move is designed to streamline and enhance the trial focused on patients with Dengue fever and similar viral illnesses. This isn’t just a procedural step; it signals tangible progress in the drug’s development pathway.

Key Details of the Amendment

- •Trial Focus: The randomized, double-blind, placebo-controlled trial will evaluate the safety and efficacy of CP-COV03 in patients with Dengue (Part 1) and expand to Dengue-like diseases such as Zika, Influenza A, and COVID-19 in Part 2.

- •Formulation Change: The investigational drug has been changed from a capsule to a granule formulation. This could improve patient compliance, especially in pediatric or geriatric populations, and potentially alter drug absorption rates.

- •Site Expansion: The number of clinical trial sites has been increased from one to two, which is expected to accelerate patient recruitment and data collection, thereby shortening the overall trial timeline.

The Bull Case: Why This Is a Positive Catalyst

This approval is more than just a regulatory checkmark; it represents a multi-faceted positive signal for Hyundai Bioscience and its investors. The potential impact extends from drug pipeline validation to market access.

Validating the Broad-Spectrum Antiviral Strategy

The greatest potential of HYUNDAI BIOSCIENCE CP-COV03 lies in its ambition to be a broad-spectrum antiviral. By targeting Dengue fever—a mosquito-borne illness that, according to the World Health Organization (WHO), infects up to 400 million people annually—the company is tackling a massive unmet medical need. Success in this area could serve as a proof-of-concept for its efficacy against other viral threats listed in Part 2 of the trial, significantly amplifying its total addressable market and long-term value.

Operational Efficiency and Market Access

Expanding to two trial sites in Vietnam is a savvy operational move. It not only accelerates the research timeline but also builds a strong foundation for regulatory approval and commercialization within the Southeast Asian market, a region where Dengue is highly endemic. This provides a clear, strategic path to an initial target market upon successful trial completion.

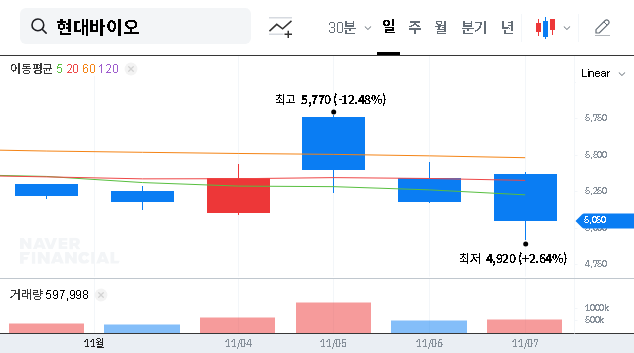

The amendment approval for the CP-COV03 clinical trial is a critical step forward, demonstrating regulatory confidence and operational progress. For investors, it reinforces the narrative that Hyundai Bioscience is actively advancing its most promising pipeline asset.

The Bear Case: Navigating Potential Risks

Despite the optimism, investing in a clinical-stage biotech company carries substantial risks. Acknowledging these hurdles is essential for a balanced investment thesis. For those new to this sector, understanding the common challenges is crucial. You can learn more by reading our Guide to Investing in Biotech Stocks.

- •Clinical Uncertainty: The primary risk is always the clinical outcome. Positive results in Phase 2 are not guaranteed. Any negative or inconclusive data regarding the safety or efficacy of CP-COV03 would be a significant setback, likely impacting the company’s valuation and development strategy.

- •Financial Health and Cash Burn: Clinical trials are expensive. Expanding sites and advancing research increases the rate of cash burn. Investors must monitor Hyundai Bioscience’s financial statements, particularly its cash reserves and capital-raising activities, to ensure it has the runway to see this trial through to completion.

- •Formulation Risk: While the switch to granules has potential benefits, it also introduces a new variable. The company must demonstrate that this new formulation is safe, stable, and delivers the drug effectively. Any issues could cause delays or require further costly studies.

Frequently Asked Questions (FAQ)

What is the core significance of this clinical trial approval?

It signifies tangible progress in the development of HYUNDAI BIOSCIENCE’s key drug, CP-COV03. Approval from the Vietnamese Ministry of Health advances its Dengue treatment program and signals potential expansion to other viral diseases, de-risking the development pathway to a small degree.

Why was the CP-COV03 formulation changed to granules?

The change from a capsule to a granule formulation is likely intended to improve patient convenience and compliance, particularly for those who have difficulty swallowing pills. However, its impact on the drug’s performance must be validated in the clinical trial.

What should investors watch for next?

The most critical upcoming catalyst will be the interim and final results from the Phase 2 portion of this trial. Positive safety and efficacy data will be essential for moving to Phase 3 and will be a major driver of the company’s valuation. Investors should also monitor financial reports for updates on R&D spending and cash position.