The recent announcement of the Orbitech convertible bond (CB) issuance, a KRW 5 billion capital injection, has sparked intense debate among investors. While the move secures much-needed liquidity for the company, it simultaneously raises valid concerns about potential stock dilution and its impact on shareholder value. For those invested in or monitoring Orbitech, this decision represents a critical juncture that demands careful analysis.

This comprehensive guide provides a deep dive into Orbitech’s CB issuance. We will dissect the terms, evaluate the company’s underlying financial health, weigh the potential benefits against the risks, and offer a strategic framework to help you make an informed investment decision.

Understanding the Orbitech Convertible Bond Terms

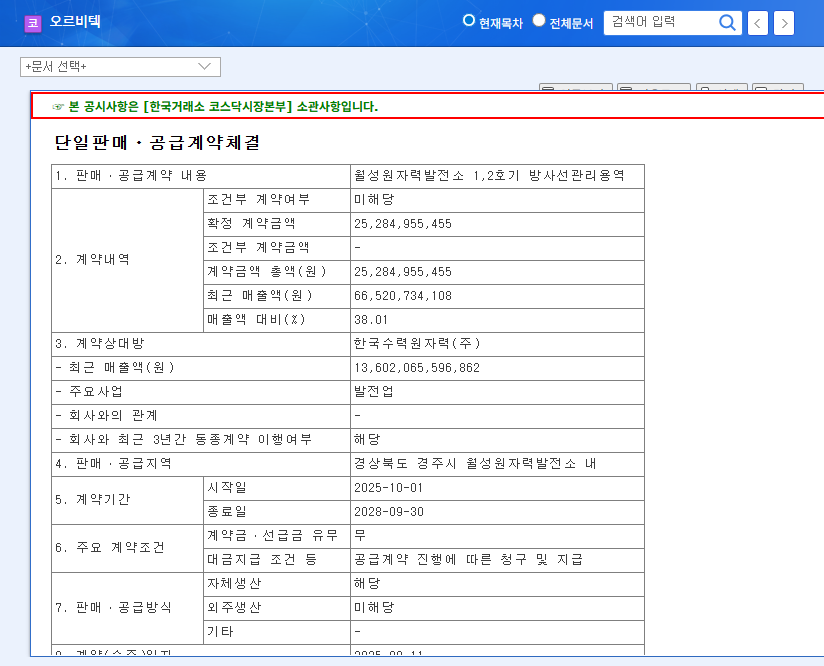

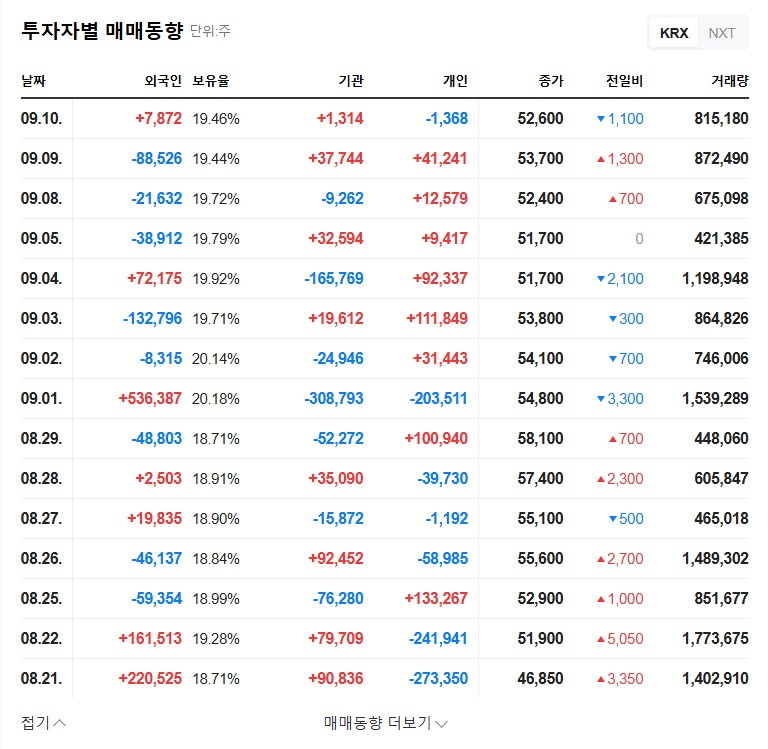

On November 10, 2025, Orbitech Co., Ltd. finalized a private placement for KRW 5 billion in convertible bonds. The primary investors in this offering are Finednc and Codes. Understanding the specifics of this deal is the first step in any thorough Orbitech stock analysis. The full details can be reviewed in the Official Disclosure (DART).

Key Financial Details

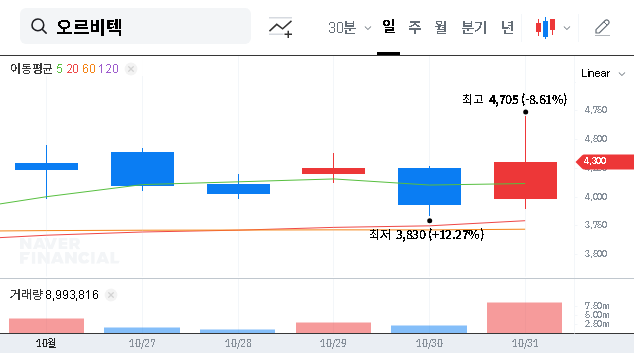

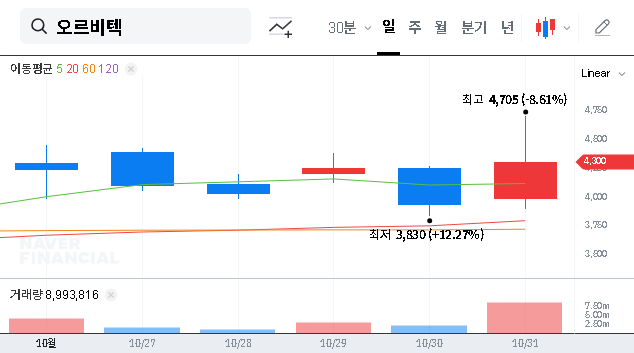

- •Conversion Price: Set at KRW 3,967 per share, which is slightly below the market price of KRW 4,130 at the time of the announcement. This incentivizes conversion into stock.

- •Interest Rates: Both the coupon rate and the maturity yield are 0%. This indicates that bondholders are not seeking interest payments but are banking on capital gains from converting the bonds into equity.

- •Timeline: The payment date for the bonds is December 26, 2025. The conversion period, during which bondholders can request to swap their bonds for stock, runs from December 26, 2026, to November 26, 2028.

Why Now? Orbitech’s Pressing Need for Capital

The decision to issue an Orbitech CB is directly tied to the company’s recent financial performance. While Orbitech has maintained a steady stream of revenue from its core nuclear, ISI, and aerospace divisions, profitability has become a major concern. As of the first half of 2025, operating losses have widened, signaling an urgent need for both capital and operational improvements.

The primary challenge stems from a high cost of goods sold (COGS) ratio, particularly within the aerospace and ISI segments. This has eroded margins and put significant pressure on the company’s financial health, making this capital raise a defensive necessity.

While the company’s net income saw some improvement due to non-operational gains from financial asset valuations, this masks the underlying weakness in its core business activities. This disconnect highlights that without fundamental changes to its cost structure, the company’s long-term stability remains at risk.

The Bull Case vs. The Bear Case for Investors

For any Orbitech investment, it’s crucial to weigh the positive implications of this fundraising against the significant risks it introduces.

Potential Positives (The Bull Case)

- •Improved Financial Stability: The KRW 5 billion infusion provides immediate short-term liquidity, strengthening the balance sheet and allowing the company to fund operations and strategic initiatives.

- •Vote of Confidence: A private placement to specific investors like Finednc and Codes can be interpreted as a sign of external confidence in Orbitech’s long-term business model and recovery potential.

- •Future Growth Catalyst: If used effectively to improve the cost structure and invest in profitable areas, this capital could fuel a turnaround, ultimately driving the stock price higher and making the eventual conversion a net positive for all shareholders.

Potential Negatives (The Bear Case)

The most significant risk is stock dilution. When the convertible bonds are exchanged for common stock, the total number of outstanding shares increases. This means each existing share represents a smaller percentage of ownership in the company, which can decrease earnings per share and depress the stock price. To learn more, you can read a detailed explanation of how stock dilution affects shareholders on high-authority sites like Investopedia.

- •High Conversion Likelihood: With a 0% interest rate and a conversion price below the current market price, conversion is the only path to profit for bondholders, making future dilution almost certain.

- •Masking Deeper Issues: The capital raise might be seen as a temporary fix that fails to address the core problem: a lack of operational profitability. Without a clear plan to reduce the COGS ratio, the company could find itself in a similar position in the future.

Investor Strategy: Navigating the Path Forward

The Orbitech convertible bond issuance is a pivotal event. In the short term, the market will likely react to the infusion of cash, but the overhang of potential dilution will remain a headwind. The long-term trajectory of Orbitech’s stock will depend entirely on how effectively management deploys this new capital.

Actionable Checklist for Investors

- •Monitor Profitability Metrics: Pay close attention to Orbitech’s upcoming H2 2025 earnings reports. Look for specific evidence of margin improvement and a reduction in the COGS ratio.

- •Track the Conversion Price vs. Market Price: As the stock price moves, the incentive to convert will change. A significant rise in stock price would make conversion and subsequent selling by bondholders more likely.

- •Analyze Industry Tailwinds: Keep an eye on the broader outlook for the nuclear and aerospace industries. Positive sector trends could provide a lift to Orbitech and help offset the dilution pressure.

In conclusion, Orbitech’s decision is a calculated risk. For investors, this is not a simple buy or sell signal but a call for heightened diligence. A prudent investment strategy requires a comprehensive assessment of the company’s ability to translate this financial lifeline into tangible, sustainable improvements in its core business profitability.