The biotech market is buzzing with a significant development that has investors closely watching OSCOTECInc. stock. Meritz Securities, a top-tier Korean financial institution, has publicly disclosed its acquisition of a 5.04% stake in the innovative bio-venture. While officially labeled a ‘simple investment,’ a move of this magnitude in a company valued at over $1.3 billion demands a closer look. This signals strong institutional confidence and raises a critical question: What does Meritz Securities see in OSCOTECInc.’s future?

This comprehensive analysis will delve into the core drivers behind this investment. We will dissect OSCOTECInc.’s promising new drug pipeline, evaluate its stable foundational businesses, and consider the financial landscape to provide a clear outlook for current and prospective investors.

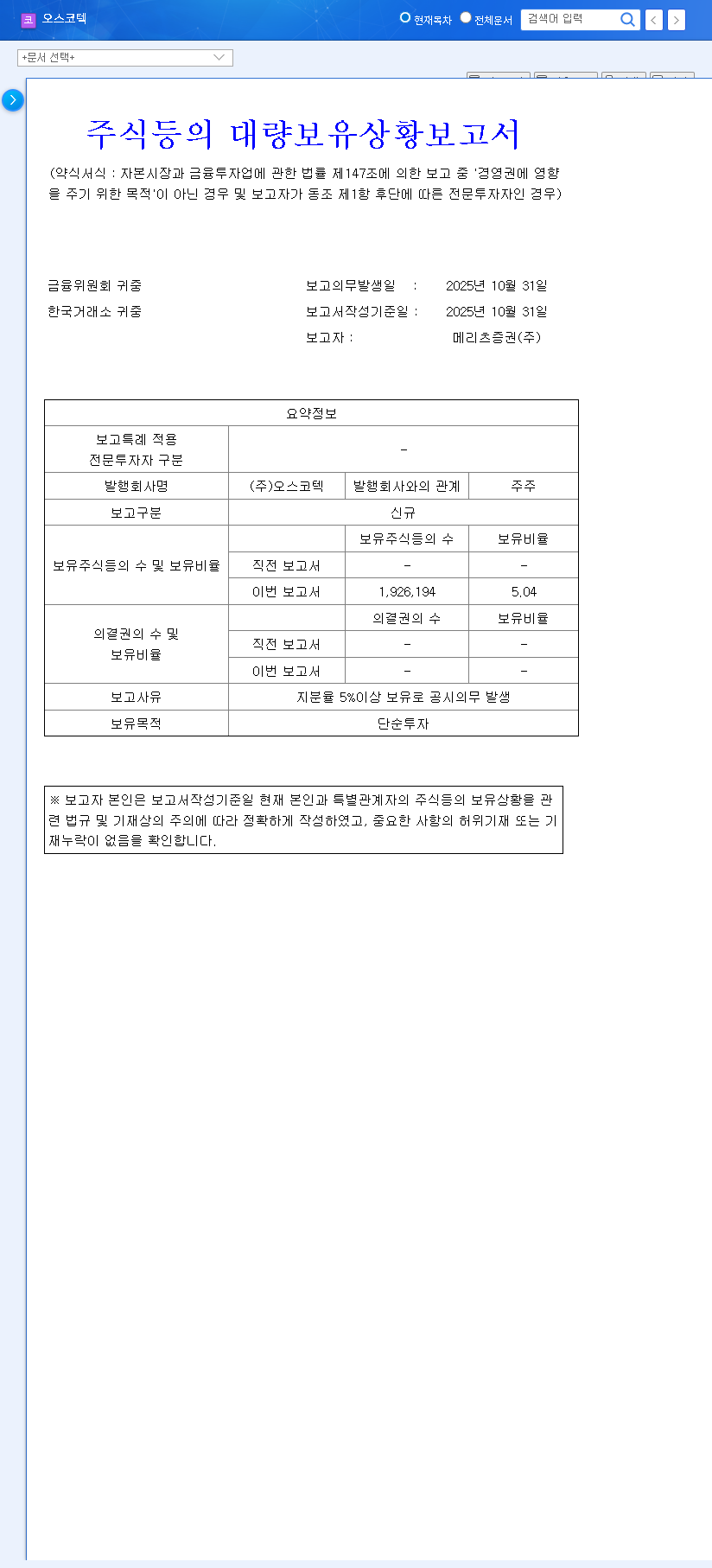

The Catalyst: Meritz Securities Discloses Major Stake

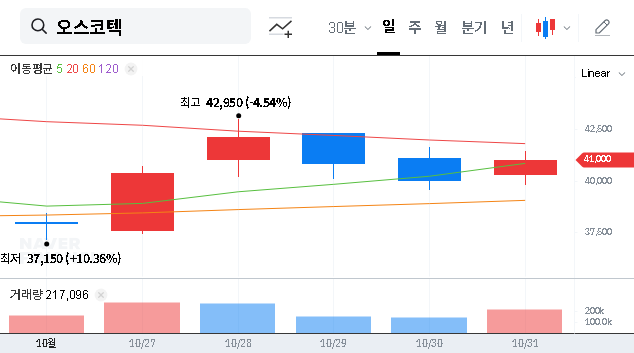

On October 31, 2025, the market took notice when Meritz Securities filed a mandatory disclosure report. According to the Official Disclosure, the firm acquired 20,319 common shares via open market purchases, elevating its total ownership to 5.04%. In capital markets, crossing the 5% threshold is a significant event, as it triggers a public reporting obligation and signals the arrival of a major shareholder. For a biotech company like OSCOTECInc., such a vote of confidence from a respected financial powerhouse is a powerful validator.

Meritz Securities’ investment is not just a financial transaction; it’s a strong endorsement of OSCOTECInc.’s underlying value proposition, blending cutting-edge drug development with stable, revenue-generating operations.

Analyzing the OSCOTECInc. Stock Investment Thesis

To understand the long-term potential of OSCOTECInc. stock, we must analyze the company’s fundamentals through the same lens an institutional investor would. The appeal lies in a potent combination of high-growth potential and foundational stability.

1. The Crown Jewel: A Promising New Drug Pipeline

The primary driver of any biotech valuation is its pipeline. OSCOTECInc. boasts several compelling candidates that are progressing steadily through clinical trials, a process meticulously tracked by agencies like the U.S. Food and Drug Administration (FDA).

- •OCT-598 (Solid Cancer Therapy): With FDA Phase 1 IND approval, this AXL-targeted therapy represents a significant growth engine. AXL inhibitors are a promising class of drugs for treating various solid tumors, a massive market with unmet needs.

- •ADEL-Y01 (Alzheimer’s Treatment): The commencement of dosing for FDA Phase 1a of this Tau antibody is a major milestone. The Alzheimer’s space is challenging but offers astronomical potential for any therapy that proves effective.

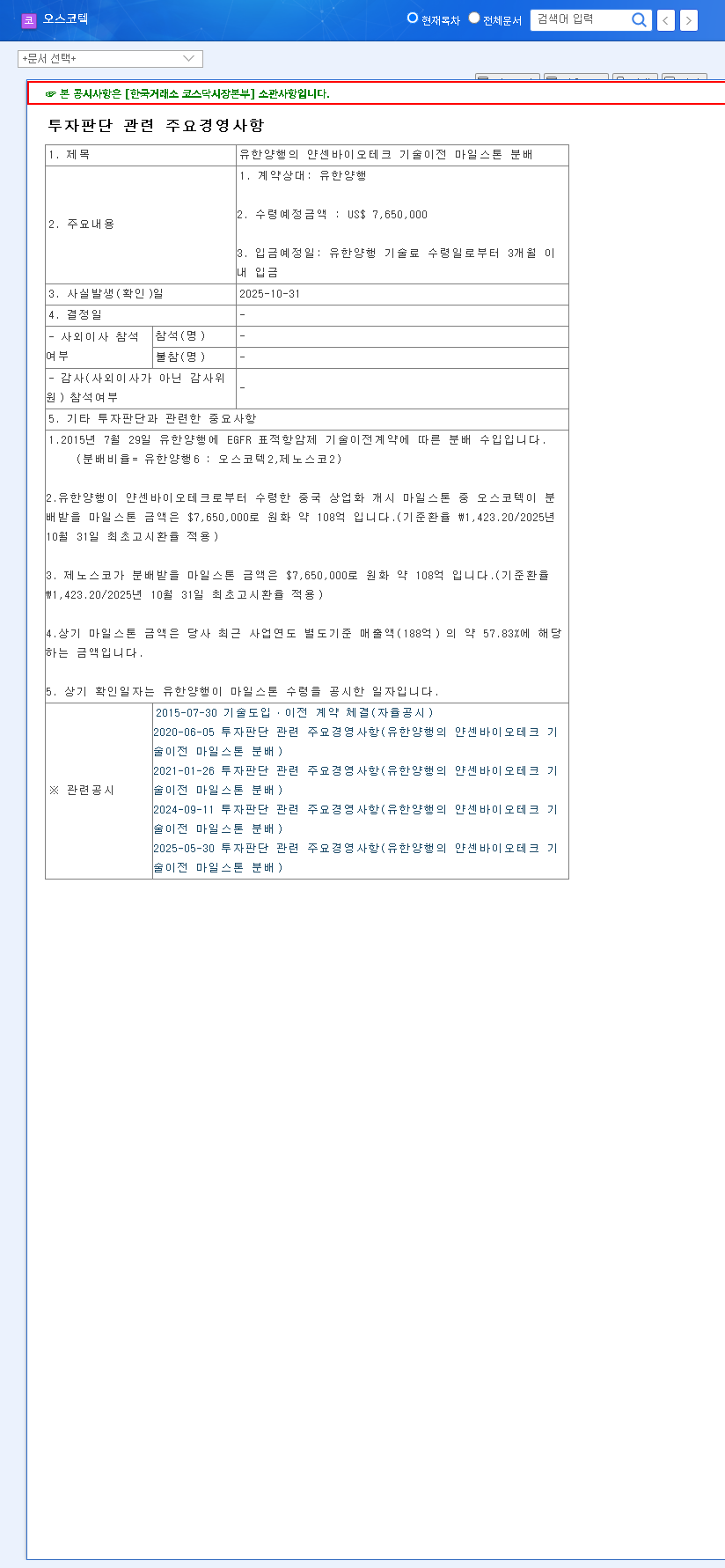

- •Proven Commercialization: The company isn’t just a research lab. Stable milestone and royalty revenues from its Lazertinib technology transfer agreement provide non-dilutive cash flow and, more importantly, prove its ability to successfully commercialize its discoveries.

2. The Foundation: Stable Revenue from Existing Businesses

Unlike many of its peers, OSCOTECInc. is not solely reliant on its pipeline. It has established, profitable business segments that provide a stable financial floor.

- •Dental Business: Flagship products like InduCera and BioCera-F generate consistent sales in the dental bone graft and membrane market. Expansion into overseas markets like Japan further bolsters this revenue stream.

- •Functional Materials: Leveraging its R&D prowess, this division creates differentiated materials for various industries, securing another layer of stable growth potential.

3. Financial Considerations and Challenges

A balanced biotech stock analysis requires acknowledging the risks. Drug development is incredibly capital-intensive. OSCOTECInc.’s R&D expenses are high, leading to an operating loss in H1 2025. This cash burn is a necessary investment in the future but remains a key metric for investors to monitor. Furthermore, the company carries financial liabilities like convertible bonds that require careful management to ensure long-term financial health.

Outlook: What This Means for OSCOTECInc. Stockholders

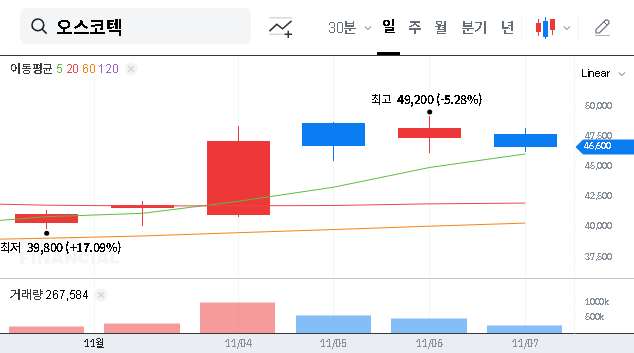

The immediate impact of Meritz’s disclosure is a boost to investor sentiment. It validates the company’s strategy and can attract more institutional interest. However, seasoned investors know that fundamentals drive long-term value. While the news provides positive momentum, the share price will ultimately be determined by tangible progress.

Investors should adopt a mid-to-long-term perspective, focusing on key catalysts that will shape the company’s trajectory. For those interested in this sector, understanding the nuances of how to evaluate biotech stocks is crucial.

- •Clinical Trial Data: Upcoming results from OCT-598 and ADEL-Y01 will be the most significant value-inflection points. Positive data can lead to substantial re-ratings of the stock.

- •Partnerships & Licensing: New technology transfer or licensing-out agreements would further validate the pipeline and provide significant capital injections.

- •Business Growth: Continued market share gains and international expansion in the dental business will demonstrate operational excellence and strengthen the balance sheet.

In conclusion, Meritz Securities’ investment in OSCOTECInc. is a clear signal that the company’s blend of high-potential R&D and stable commercial operations is resonating with smart money. While the path of any biotech is fraught with risk, the institutional validation of the OSCOTECInc. investment thesis suggests a compelling future. Investors should focus on the execution of its pipeline and business strategy rather than short-term market noise.