A significant market event has put Gamsung Corp (036620) squarely in the spotlight: the National Pension Service (NPS) of Korea, the country’s largest and one of the world’s most influential institutional investors, has acquired a substantial 5.03% stake. This move is more than just a line item in a report; it’s a powerful signal of confidence in the company’s trajectory and future value. For savvy investors, this development warrants a deeper look.

This comprehensive Gamsung Corp stock analysis will unpack the implications of the NPS investment, dissect the company’s robust fundamentals, evaluate the surrounding market environment, and highlight the key opportunities and risks that lie ahead. Let’s explore why this apparel and mobile powerhouse is capturing institutional attention.

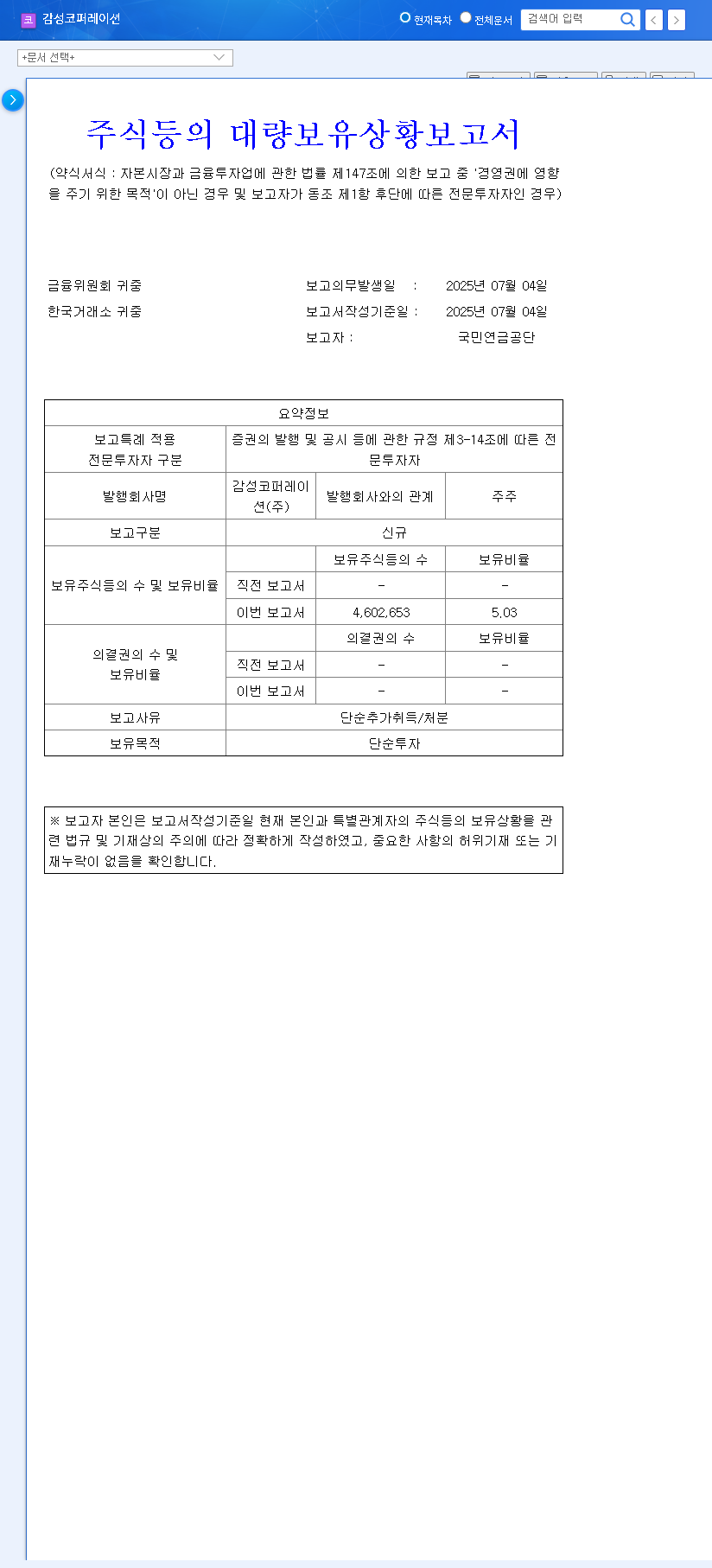

The NPS Investment: A Major Vote of Confidence

On October 26, 2024, the National Pension Service officially reported its large-scale shareholding in Gamsung Corp (036620). According to the Official Disclosure on DART, the NPS now holds a 5.03% stake for ‘simple investment purposes.’ For a company with a market capitalization of KRW 543 billion, this is a noteworthy move. Investments from the NPS are meticulously vetted and often signal a long-term positive outlook on a company’s fundamentals and governance, instantly boosting market credibility and attracting wider investor interest.

“When an institution like the NPS takes a significant position, it’s not just buying shares; it’s endorsing the company’s strategy and growth story. This action often acts as a catalyst, strengthening stock price momentum and placing a greater emphasis on shareholder value.”

Analyzing Gamsung Corp’s Strong Fundamentals

The NPS’s decision wasn’t made in a vacuum. Gamsung Corp (036620) is building a compelling growth narrative, primarily driven by its apparel division and strengthening financial health.

Revenue Growth Engine: The ‘Snow Peak Apparel’ Phenomenon

The star of the show is undeniably the Snow Peak Apparel brand, which accounts for over 96% of sales. The company’s recent success includes:

- •Explosive Growth: After turning profitable in 2023, sales are projected to hit KRW 196.3 billion in 2024, a stunning 27% year-over-year increase.

- •Soaring Profitability: The operating profit margin is forecast to jump from 2.42% in 2023 to an impressive 7.99% in 2024, with expectations to clear 10% in 2025.

- •Strategic Expansion: This growth is fueled by a successful push into overseas markets and a robust Direct-to-Consumer (D2C) strategy that enhances margins and brand control.

Strengthening Financial Health

The company’s balance sheet is becoming increasingly solid, providing a stable foundation for growth. The debt-to-equity ratio has improved, falling from 32.02% in 2023 to 25.82% in 2024. Simultaneously, Return on Equity (ROE) has more than doubled from 3.77% to 8.32%, indicating highly efficient use of shareholder capital. These are metrics that institutional investors like the NPS watch closely. For more on financial metrics, consider this guide to analyzing retail stocks.

Navigating the Market: Opportunities and Risks

The NPS investment brings positive momentum, but a complete Gamsung Corp stock analysis requires a clear-eyed view of both external factors and internal challenges.

Positive Tailwinds

- •Enhanced Credibility: The NPS’s backing is likely to attract more institutional and retail investors, potentially sustaining the stock’s upward trend.

- •Shareholder Activism: The NPS may encourage better ESG practices, more transparent governance, and increased shareholder returns (e.g., dividends, buybacks).

- •Favorable Macro-Environment: Stable global shipping costs and a trend towards lower interest rates, as seen in global economic reports, could reduce costs and boost consumer spending.

Potential Risk Factors to Monitor

Despite the positive outlook, investors must remain vigilant of potential challenges that could impact the 036620 stock price.

- •Rising Inventory Levels: Inventory increased 15.9% year-over-year, and a low turnover ratio of 0.9x could signal a sales slowdown or overstocking, potentially leading to future margin pressure from discounts.

- •High Business Dependency: With the apparel business contributing over 96% of sales, the company is highly exposed to economic downturns and the fickle nature of fashion trends.

- •Underperforming Investments: The investment in an associate, Virtual Mining Co., Ltd., continues to drag on profitability and requires close monitoring.

Investment Outlook for Gamsung Corp (036620)

Gamsung Corporation presents a compelling case. The company is delivering solid earnings improvement, strengthening its financial position, and has now earned a significant endorsement from the National Pension Service. The short-to-medium-term outlook appears positive, with potential for further stock price appreciation driven by strong fundamentals and renewed investor confidence. However, a smart investment strategy involves continuous monitoring of the identified risk factors. Keeping a close watch on the growth of Snow Peak Apparel, inventory management efficiency, and any future shareholder actions by the NPS will be crucial to navigating this investment opportunity successfully.

Disclaimer: This analysis is for informational purposes only and is based on publicly available data. All investment decisions are the sole responsibility of the investor.

Leave a Reply