This comprehensive KOREA UNITED PHARM investment analysis dissects the company’s preliminary Q3 2025 earnings report, which has sent mixed signals to the market. While a remarkable 29% net profit surprise suggests strong profitability management, a simultaneous miss in operating profit raises important questions about core operational health. For investors evaluating KOREA UNITED PHARM INC, understanding this dichotomy is crucial. We’ll explore the fundamental drivers, competitive advantages, potential risks, and the future outlook to provide a clear, actionable perspective on this intriguing pharmaceutical stock.

Q3 2025 Earnings: A Tale of Two Profits

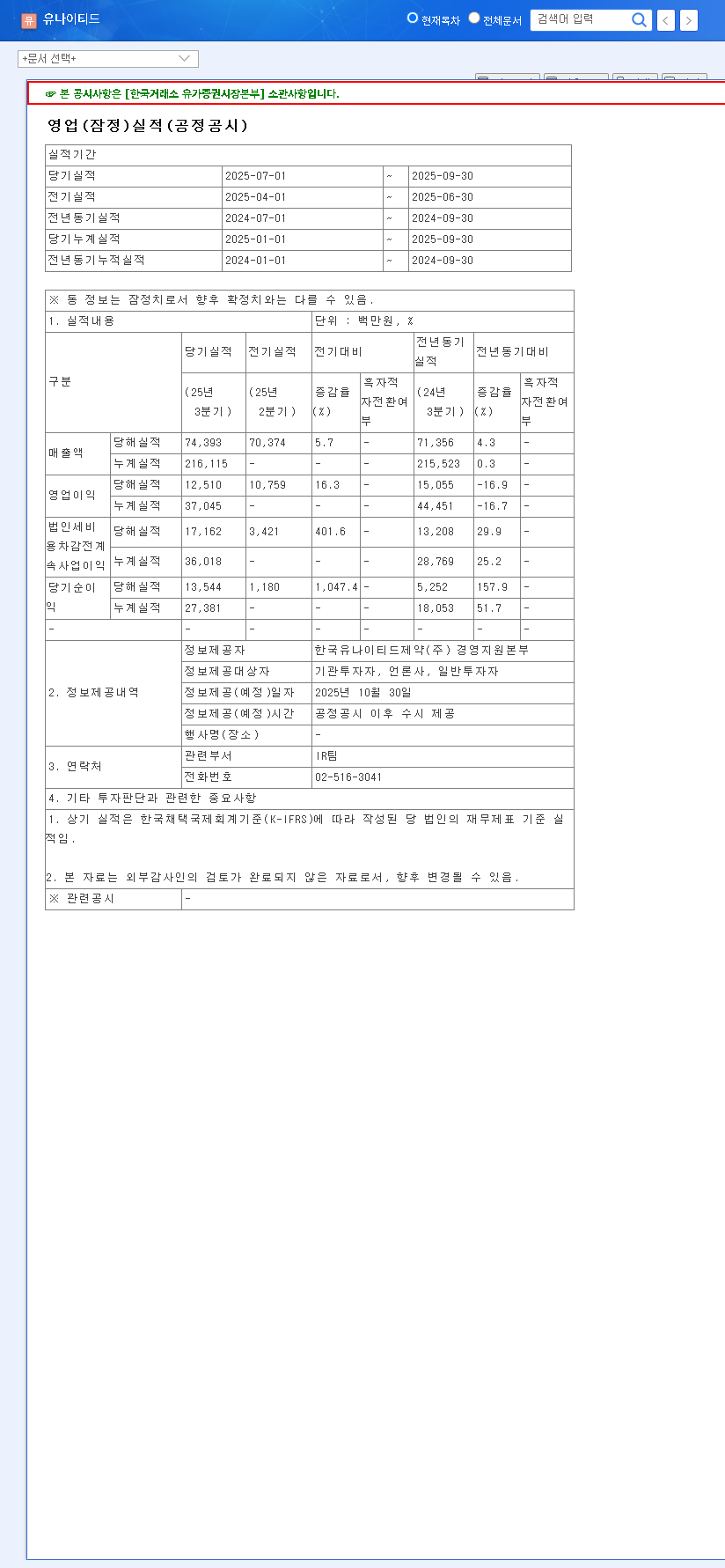

On October 30, 2025, KOREA UNITED PHARM INC released its preliminary Q3 earnings, painting a complex but fascinating picture. You can view the Official Disclosure (DART) for the raw data. Here’s a breakdown of the key figures against market estimates:

- •Revenue: ₩74.4 billion, a solid 2% beat that demonstrates consistent top-line growth.

- •Operating Profit: ₩12.5 billion, a 3% miss that requires deeper investigation into the company’s operational efficiency.

- •Net Profit: ₩13.5 billion, an astonishing 29% beat that became the standout headline of the report.

The market’s immediate reaction is likely to be positive, fueled by the revenue and net profit surprises. However, savvy investors will look beyond the headlines to understand the underlying causes of the operating profit dip, which could signal challenges in cost of goods sold (COGS) or rising administrative expenses.

Analyzing KOREA UNITED PHARM INC’s Core Strengths

Despite the mixed Q3 results, the company’s fundamentals remain robust. A thorough pharmaceutical stock analysis reveals several key pillars supporting its long-term value proposition.

Stable Financials & Commitment to Innovation

The company’s financial health is excellent, marked by a low debt-to-equity ratio of just 12.4%. This provides a stable foundation to weather economic storms and fund future growth. Furthermore, a significant R&D investment, equating to 12% of revenue, signals a strong commitment to building a pipeline of future blockbuster drugs. This level of investment is critical for long-term relevance in the competitive pharmaceutical landscape.

A Competitive Moat in Modified Drugs and Global Expansion

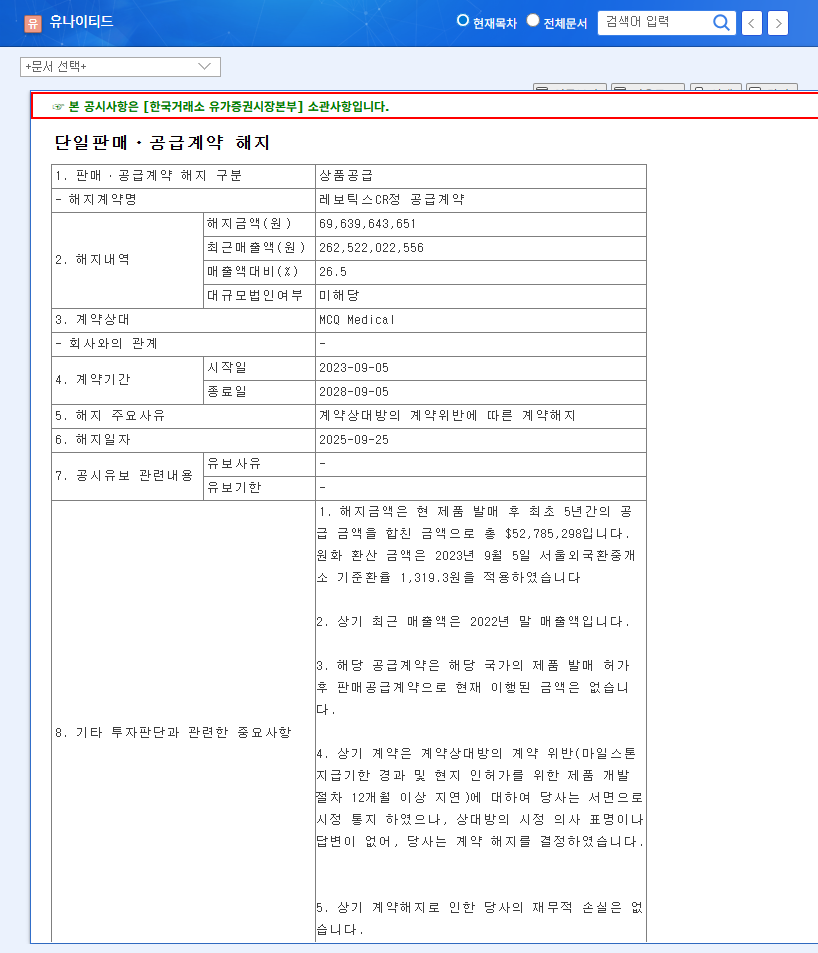

A key differentiator for KOREA UNITED PHARM INC is its leadership in modified drugs. With 17 products in this category, the company has carved out a unique and defensible market position. This is complemented by an aggressive global expansion strategy. Exports now account for 9% of total revenue, with products reaching over 40 countries. Strategic partnerships, such as those with Teva Pharmaceutical and MCQ Medical, are set to amplify this global reach, promising a significant future growth vector.

The core of this Q3 earnings analysis lies in balancing the impressive net profit, likely boosted by savvy financial management or non-operational gains, against the slight erosion in operating profit, which reflects the day-to-day business of making and selling medicine.

Risks and Future Outlook

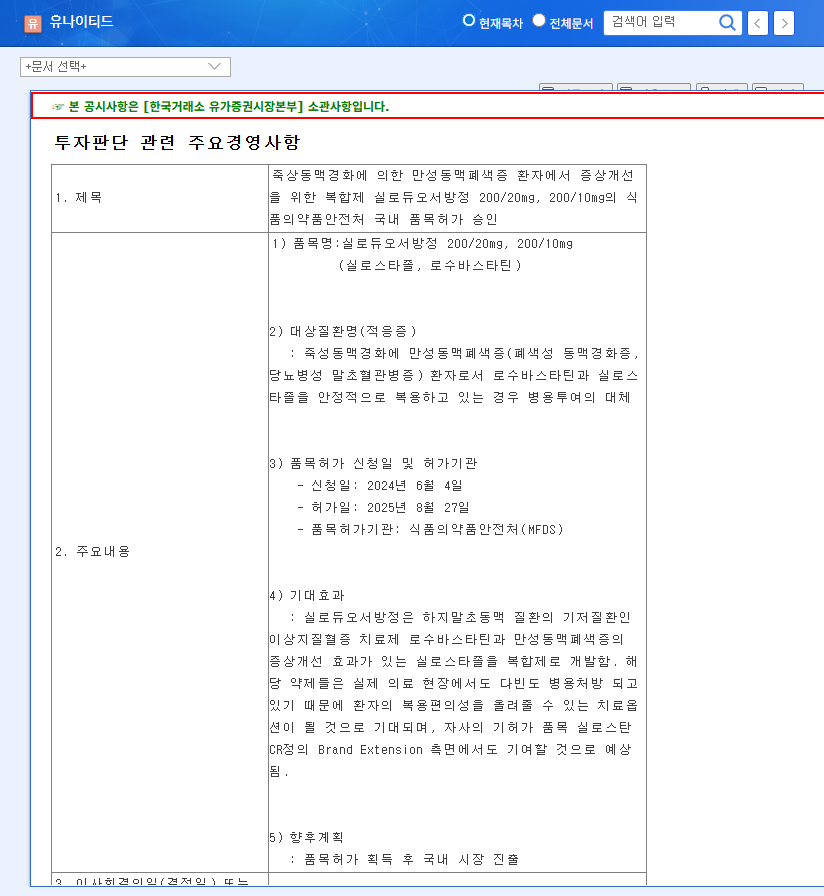

No investment is without risk. For the KOREA UNITED PHARM stock, investors must carefully monitor the factors behind the operating profit miss. Was it a one-off increase in marketing spend for a new product launch, or a more systemic issue like rising raw material costs? Understanding the dynamics of operating margins is crucial. Additionally, external factors like government drug pricing policies, foreign exchange volatility, and the inherent uncertainty of clinical trials for pipeline drugs like UI022, UI023, and UI064 must be considered.

Looking ahead, the company’s trajectory will be heavily influenced by its ability to convert its high R&D spending into commercially successful products and to continue its impressive expansion into overseas markets. Success in these areas could easily overshadow the minor concerns from the Q3 operating profit.

Frequently Asked Questions (FAQ)

What were the key highlights of KOREA UNITED PHARM INC’s Q3 earnings?

The main highlight was a 29% beat on net profit, reaching ₩13.5 billion. Revenue also slightly exceeded expectations at ₩74.4 billion. However, operating profit of ₩12.5 billion slightly missed estimates.

What are the primary strengths of KOREA UNITED PHARM INC?

The company’s key strengths include a very stable financial structure with low debt, a strong commitment to R&D, market leadership in modified drugs, and a rapidly expanding global footprint in over 40 countries.

What potential risks should investors watch for?

Investors should monitor for pressure on operating margins, macroeconomic risks like interest rate changes, and industry-specific challenges such as clinical trial outcomes and regulatory hurdles. For more on this, consider our guide on evaluating pharmaceutical stocks.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The final responsibility for investment decisions rests with the individual investor. For expert financial guidance, consult with a qualified professional like those at Fidelity Investments.