The latest Dongwon Systems earnings report for Q3 2025, released on November 5, 2025, has presented a nuanced and complex narrative for investors. While the company showcased improved year-over-year profitability despite lower revenue, a sequential dip in performance has cast a shadow of short-term uncertainty. For those closely watching the Dongwon Systems stock, the central question remains: how much weight should be given to the immense promise of its burgeoning secondary battery materials business versus the immediate financial realities? This comprehensive analysis will dissect the Q3 results, evaluate the company’s core operations, and provide a strategic outlook to help investors navigate what comes next.

Dongwon Systems’ Q3 2025 Earnings at a Glance

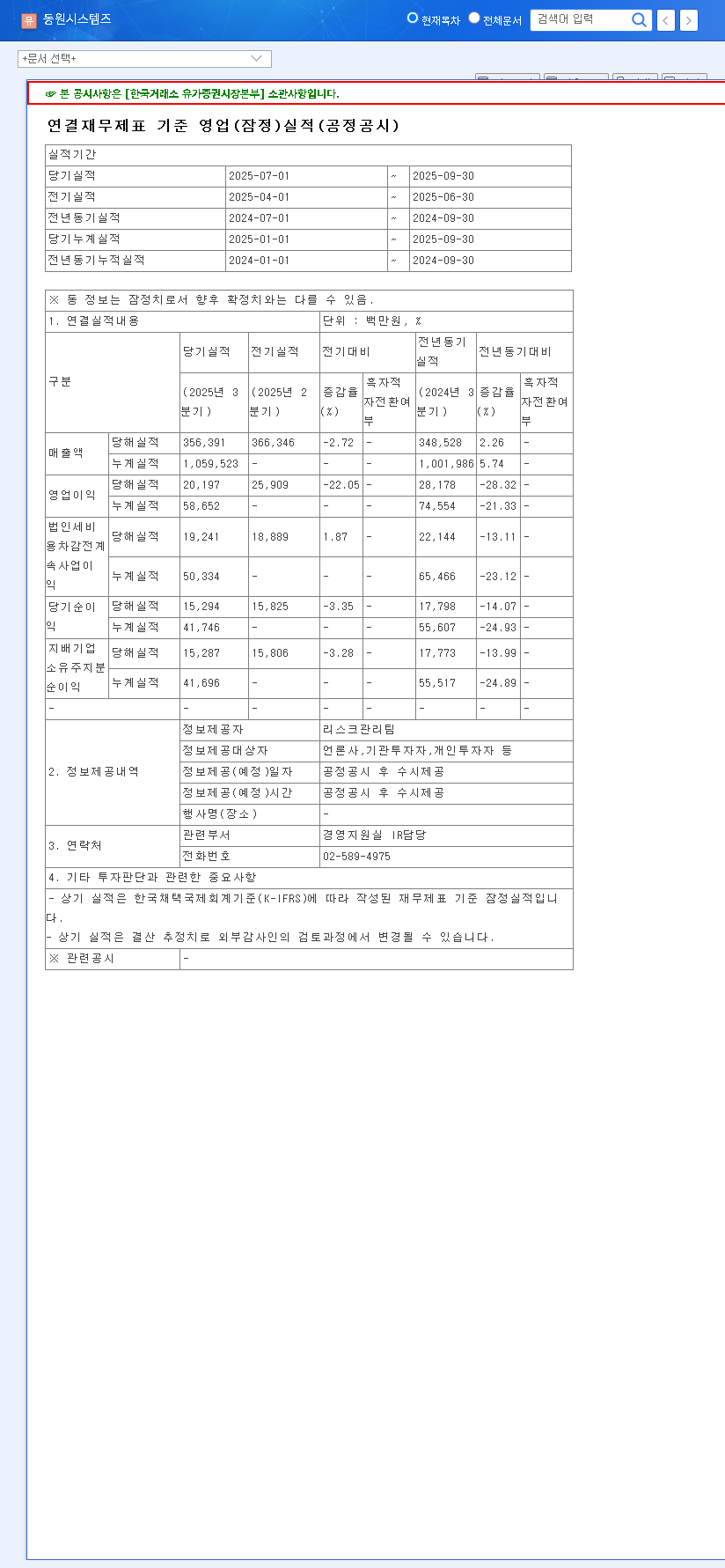

Dongwon Systems reported its preliminary consolidated earnings for the third quarter, revealing a mixed bag of results. Here are the key figures from the official filing (Source: Official DART Disclosure):

- •Revenue: KRW 356.4 billion (a decrease year-over-year).

- •Operating Profit: KRW 20.2 billion (an increase year-over-year).

- •Net Profit: KRW 15.3 billion (an increase year-over-year).

The key takeaway is a classic ‘good news, bad news’ scenario. The ‘good news’ is the improved profitability compared to the same quarter last year, which suggests better cost controls or a more favorable product mix. However, the ‘bad news’ is that all three metrics declined compared to the preceding quarter (Q2 2025), signaling a potential loss of short-term momentum. This sequential slowdown warrants a closer look at the underlying business segments.

Analyzing the Core Business Drivers

The Stable Foundation: Comprehensive Packaging

Dongwon Systems’ traditional packaging business remains its bedrock. This division, covering everything from food cans and aluminum to resin and printing, provides a stable and predictable revenue stream. Its long-standing relationships with major corporate clients create a defensive moat. Critically, the company’s proactive pivot towards eco-friendly packaging materials aligns with global ESG (Environmental, Social, and Governance) trends, positioning this cash-cow division for sustainable, long-term relevance.

The Growth Engine: Secondary Battery Materials

The excitement surrounding the Dongwon Systems stock is almost entirely focused on its strategic expansion into EV battery materials. This venture, bolstered by the acquisition of MKC and significant capital investment in new facilities, represents the company’s primary future growth driver. Two areas are particularly crucial:

- •4680 Battery Can Production: The company is gearing up for mass production of the next-generation 4680-format battery can. This cylindrical cell format is a game-changer, promising higher energy density and lower costs, and is central to the plans of EV leaders like Tesla. Successfully scaling production would make Dongwon a key player in a high-growth market segment.

- •Aluminum Cathode Foil: This component is vital for lithium-ion battery performance. Dongwon’s expansion of its aluminum foil business taps directly into the surging global demand for EVs and energy storage solutions. For more context, you can review our guide to investing in the EV supply chain.

The core investment thesis for Dongwon Systems rests on its ability to successfully transition from a stable packaging company into a high-growth leader in the secondary battery materials space. The Q3 earnings reflect this pivotal moment of transition.

Investment Outlook: Navigating Hope and Headwinds

The latest Dongwon Systems earnings create a delicate balance for investors. On one hand, the promise of the EV battery business is immense. On the other, macroeconomic pressures and investment-related financial burdens are undeniable risks.

Short-Term Caution Advised

The sequential decline in performance could lead to short-term volatility for the stock. The market will be hungry for tangible proof points, such as major contract announcements for the 4680 battery can or clear signs of a performance rebound in Q4. Until then, a prudent, watchful approach is warranted.

Long-Term Optimism with Caveats

For long-term investors, the focus should remain squarely on the execution within the secondary battery materials division. If the company delivers on its production goals, the potential for significant value creation is high. However, risks such as rising raw material costs, fluctuating exchange rates, and intense competition from global players, as often covered by outlets like Reuters, must be continuously monitored.

Actionable Investment Strategy

Investors should adopt a strategy based on diligent monitoring rather than reactive trades:

- •Track Key Milestones: Pay close attention to announcements regarding factory ramp-ups, customer qualifications, and supply agreements for battery components.

- •Analyze Financial Health: Monitor the company’s debt levels and cash flow statements in subsequent quarters to ensure its investment phase remains manageable.

- •Adopt a Long-Term View: Base your investment decisions on the successful execution of the long-term growth strategy, not on the short-term noise of quarterly earnings fluctuations.

Disclaimer: This analysis is for informational purposes only. The ultimate responsibility for investment decisions rests with the individual investor.

Leave a Reply