In a construction sector marked by volatility, HL D&I HALLA CORPORATION (KRX: 014790) has delivered a significant Q3 2025 ‘earnings surprise’, capturing the attention of the market. The company’s preliminary operating results have not only surpassed analyst expectations but also signaled a potential turning point for investors who have been cautiously watching its performance. This comprehensive analysis will dissect the official figures, explore the underlying drivers of this success, and evaluate the financial health and future outlook for HL D&I HALLA CORPORATION.

We will examine whether this performance marks the beginning of a sustained ascent or if significant risks still warrant a cautious approach. For investors following construction sector stocks, this report provides critical insights for making informed decisions.

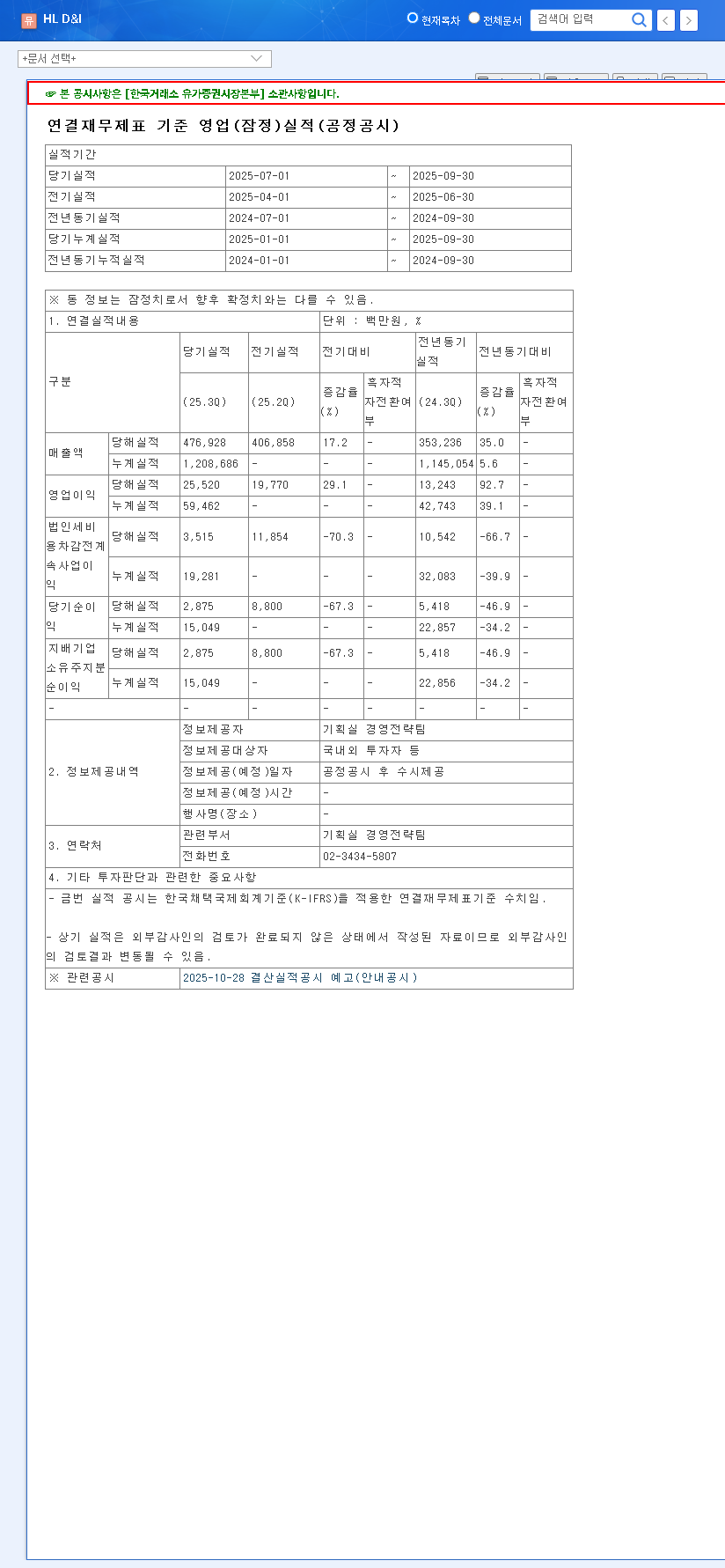

Unpacking the Q3 2025 Earnings Surprise

According to the company’s official filing, HL D&I HALLA CORPORATION announced robust results for the third quarter of 2025. The key figures are as follows:

- •Sales: 476.9 billion KRW (exceeding market consensus of 378.3 billion KRW by 26%).

- •Operating Profit: 25.5 billion KRW (a remarkable 66% above the expected 15.4 billion KRW).

- •Net Profit: 2.9 billion KRW, marking a significant return to profitability from previous net losses.

These numbers can be verified via the Official Disclosure (DART). The most impressive metric is the operating profit margin, which surged to 8.09%. This figure is a testament to the company’s enhanced operational efficiency and a significant improvement over both the previous quarter and the same period last year.

The strong Q3 performance is a clear indicator that HL D&I HALLA CORPORATION’s strategic focus on profitability and cost management is yielding substantial results, setting a positive tone for its near-term outlook.

Core Drivers Behind the Strong Performance

Success in the Construction Division & Profitability Management

The primary engine for this growth was the solid performance of the core construction division. This was amplified by synergistic effects from other business segments. The notable jump in operating profit was not merely a result of increased sales but a direct consequence of rigorous cost control and strategic efforts to enhance profitability on projects. Maintaining an operating profit margin above 5% for consecutive quarters suggests that the company’s internal restructuring and efficiency measures have taken firm root.

Favorable Market Conditions and Strategic Initiatives

External factors provided a favorable tailwind. A general recovery in the South Korean construction market, buoyed by increased government investment in Social Overhead Capital (SOC) projects, created a positive environment. Furthermore, strategic corporate initiatives are poised to accelerate growth:

- •Launch of ‘E-FIT’ Brand: The market’s reception of the new residential brand, ‘E-FIT’, will be crucial. A positive response could significantly boost the construction division’s market share and brand equity.

- •Enhanced ESG Profile: Securing an A+ rating in the KCGS ESG evaluation enhances the company’s reputation, making it more attractive to institutional and ESG-focused investors. For more on this, you can read about the growing importance of ESG in corporate valuation.

Financial Health and Stock Analysis for 014790

An 014790 stock analysis reveals a company on the mend. The debt-to-equity ratio improved to 49.38% as of December 2024, down from 55.85% the previous year, signaling a significant reduction in financial risk. Other stability indicators, like the current ratio and retained earnings, are also trending positively. This financial strengthening suggests that the company is successfully managing past burdens.

The stock price for HL D&I HALLA CORPORATION has reflected this optimism, showing a steady upward trend throughout 2025, with a notable acceleration after April. While foreign ownership remains low at 1.31%, the recent uptick alongside the price surge indicates nascent interest from international investors, which could provide further momentum if the positive earnings trend continues.

Key Risk Factors Investors Must Monitor

Despite the positive results, a prudent investor must remain aware of potential headwinds. The following risks require continuous monitoring:

- •Debt and Borrowings: While improving, the company’s debt levels historically have been a concern. It’s crucial to see if the improved profitability translates into accelerated debt repayment.

- •Litigation Risks: The potential financial impact of any ongoing legal disputes cannot be overlooked and could affect future earnings.

- •Macroeconomic Headwinds: The construction industry is sensitive to broader economic shifts. Rising interest rates, currency fluctuations, and volatile raw material prices (e.g., steel, cement) could pressure margins in future quarters.

Conclusion: An Investment Opinion of ‘Hold’

The Q3 2025 HL D&I HALLA earnings report is undeniably positive. It showcases fundamental improvements in profitability and financial stability, which should provide a short-term boost to the stock price. The combination of strong execution, strategic branding, and a supportive market environment creates a compelling narrative for growth.

However, the persistent risks related to debt, litigation, and macroeconomic factors justify a cautious stance. Time is needed to confirm that these improvements are sustainable and that the company can effectively navigate future challenges. Therefore, the recommended investment action for HL D&I HALLA CORPORATION is ‘Hold‘. Investors should continue to monitor the company’s progress on risk management and its ability to maintain this newfound profitability before committing to a long-term position.

Leave a Reply