The recent news cycle for ZINUS INC. has been dominated by a significant development that has investors on high alert. While the company issued a minor correction to a business report filing, the true story lies within the bombshell release of its preliminary ZINUS INC. Q3 2025 earnings report. This report paints a concerning picture of the company’s current financial health, revealing a major revenue shortfall and an unexpected swing to an operating loss.

This analysis will move beyond the administrative filing correction to dissect the critical details of the Q3 earnings, explore the underlying causes of this performance slump, and provide a comprehensive outlook for current and potential investors weighing their next move with Zinus stock.

The Filing Correction vs. The Real Story

It’s important to first clarify the nature of the business report correction submitted on March 12, 2025. This was a technical procedure involving adjustments to XBRL footnotes and content within financial statement notes to rectify system errors. This is not a material event impacting the company’s core business. The market’s attention, therefore, has rightly pivoted to the far more consequential release of the Q3 2025 preliminary earnings. For official details on the filing, you can view the Official Disclosure (DART).

Unpacking the ZINUS INC. Q3 2025 Earnings Shock

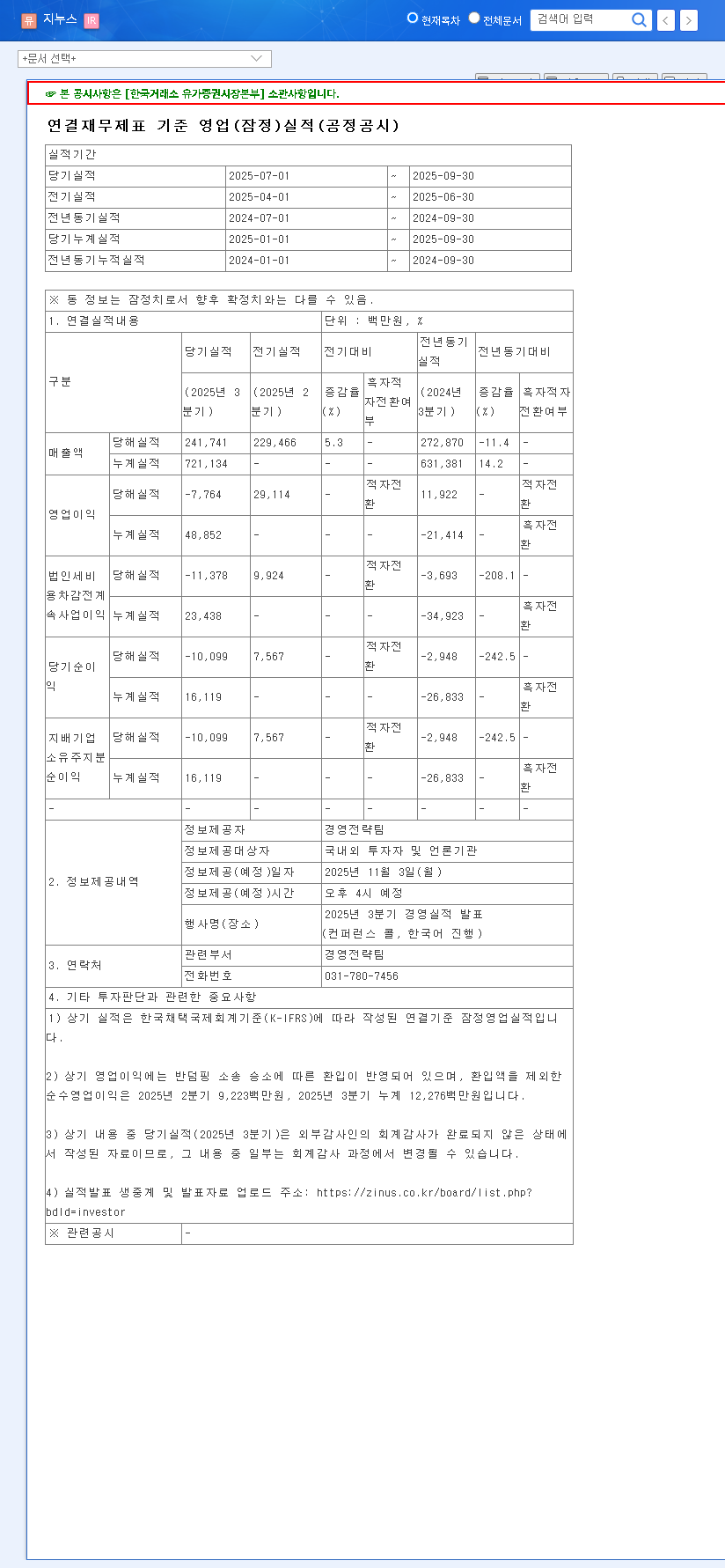

The preliminary results for Q3 2025 revealed a severe underperformance that caught the market by surprise, triggering what is commonly known as an ‘earnings shock’. The figures show a sharp deterioration not only against market consensus but also compared to previous quarters.

The transition from a consistent operating profit in the first half of 2025 to a significant operating loss of KRW 7.8 billion in Q3 marks a critical inflection point, raising serious concerns among investors about the company’s near-term trajectory.

Key Performance Metrics vs. Market Expectations

- •Revenue: KRW 241.7 billion, a staggering 19.4% below the market expectation of KRW 300 billion.

- •Operating Profit: KRW -7.8 billion. This represents a shocking reversal from the market’s anticipated profit of KRW 14.5 billion.

- •Net Income: KRW -10.1 billion, confirming the switch to a significant loss.

Analyzing the Root Causes of the Slump

The poor Q3 performance isn’t the result of a single factor but a confluence of internal vulnerabilities and external pressures. While macroeconomic indicators like stabilizing freight costs and favorable exchange rates should have provided some tailwinds, they were insufficient to counteract more fundamental issues.

Core Business and Market Headwinds

The core of the earnings deterioration appears to stem from a structural decline in revenue and profitability. Key contributing factors include:

- •Weakening Consumer Sentiment: Key markets, especially in North America, are experiencing a slowdown in discretionary spending, which directly impacts furniture and mattress sales. This aligns with broader market trends reported by sources like leading financial news outlets.

- •Major Client Order Restrictions: Zinus has a high reliance on specific large retail partners (accounting for 42.9% of sales in 2024). When these major clients restrict or reduce order volumes to manage their own inventory, Zinus’s performance is significantly impacted.

- •Increased Market Competition: The online ‘mattress-in-a-box’ market, which Zinus pioneered, has become increasingly saturated, putting pressure on pricing and market share.

Investor Outlook: Short-Term Pain vs. Long-Term Potential

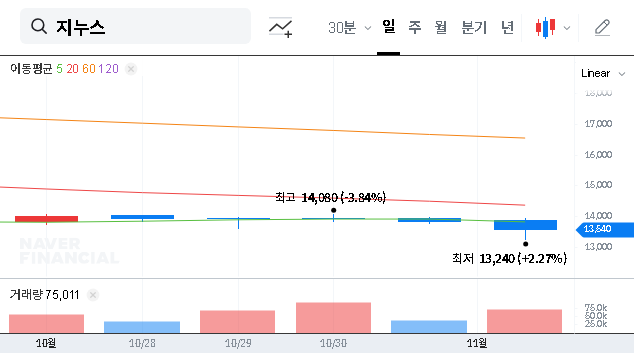

The ZINUS INC. Q3 2025 earnings will undoubtedly cast a shadow on investor sentiment in the short term. However, a complete Zinus stock analysis requires balancing these immediate headwinds against the company’s long-term fundamental strengths. To gain a deeper understanding, investors may want to learn more about analyzing quarterly reports for deeper insights.

Short-Term Risks to Consider

- •Negative Market Reaction: A sharp decline in stock price is anticipated as the market digests the earnings miss.

- •Analyst Downgrades: The significant discrepancy with market expectations could lead to target price downgrades from financial analysts.

- •Continued Uncertainty: Persistent macroeconomic uncertainty could delay the recovery in consumer spending.

Long-Term Positive Factors

- •Robust Business Model: Zinus’s core strengths—its innovative ‘Mattress-in-a-box’ technology, leadership in the online furniture market, and vertically integrated supply chain—remain intact.

- •Synergy with Parent Group: Support and synergy from the Hyundai Department Store Group can provide financial stability and new growth avenues.

- •Global Expansion: The company’s capabilities for global expansion position it well to capitalize on an eventual market recovery.

Investment Strategy: Navigating Zinus Stock

Given the Q3 earnings shock, a cautious and patient approach is warranted. While the company’s long-term business model has merit, investors should wait for clear signs of an earnings turnaround before considering a new or expanded position. Key monitoring points include:

- •Future Earnings Reports: Closely watch Q4 2025 and 2026 earnings for evidence of stabilization and recovery.

- •Revenue Diversification: Look for strategic efforts to acquire new customers and reduce reliance on a few large clients.

- •Profitability Initiatives: Monitor the company’s plans to improve its cost structure and enhance efficiency to protect margins.

In conclusion, while the business model’s long-term competitiveness is not fundamentally broken, the severity of the Q3 2025 earnings deterioration has significantly reduced Zinus’s short-term investment appeal. Prudence and diligent monitoring are the best strategies for now.