The Hansol Logistics Q3 2025 earnings report presents a complex picture for current and potential investors. In a volatile global market, corporate earnings announcements are critical decision points, especially for companies in the dynamic logistics sector. While Hansol Logistics CO., Ltd. recently reported a decrease in quarterly revenue and net profit, a deeper analysis reveals a company with solid fundamentals and significant long-term growth potential. This comprehensive analysis will dissect the latest financial data, explore the underlying business strengths and weaknesses, and provide a clear action plan for investors navigating the road ahead.

What does this mixed performance signal for the Hansol Logistics stock? What are the key investment metrics to monitor amidst a revenue slowdown? This article will provide a thorough review of the company’s Q3 performance, its financial health, and its position within the broader market, empowering you to make well-informed investment decisions.

Hansol Logistics Q3 2025 Preliminary Earnings: The Official Numbers

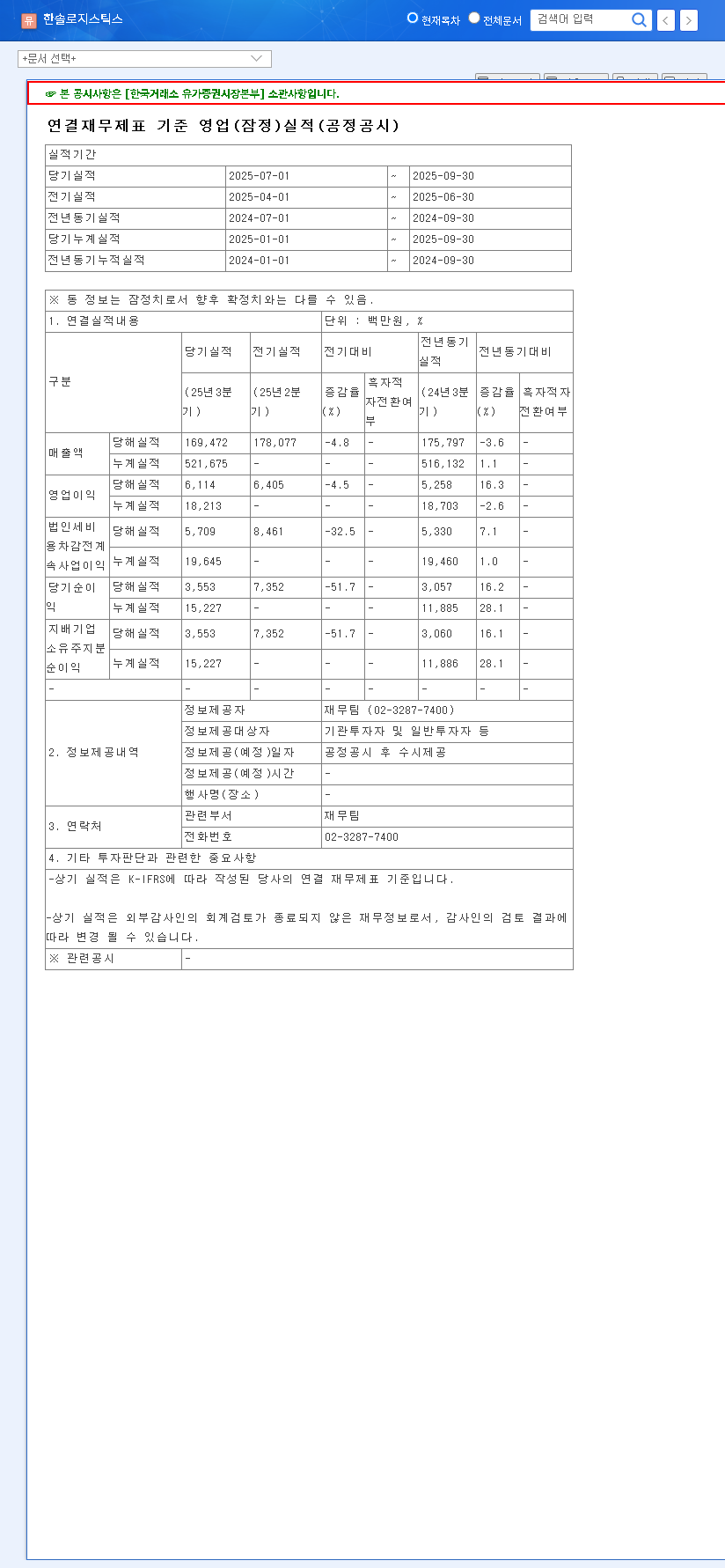

On October 30, 2025, Hansol Logistics released its preliminary consolidated operating results, offering a crucial glimpse into its recent performance. The full details can be reviewed in the company’s Official Disclosure (DART Report). The key performance indicators for the third quarter are as follows:

- •Revenue: KRW 169.5 billion

- •Operating Profit: KRW 6.1 billion

- •Net Profit: KRW 3.6 billion

When compared to the previous quarter (Q2 2025), these figures represent a 4.8% decrease in revenue, a 4.7% drop in operating profit, and a steep 51.4% plunge in net profit. However, the year-on-year (YoY) comparison with Q3 2024 tells a different story: revenue was down 3.6%, but operating profit and net profit surged by 15.1% and 16.1%, respectively. This contradictory data highlights a short-term profitability challenge against a backdrop of longer-term operational improvements.

The key takeaway from the Q3 2025 corporate earnings is the immediate pressure on profitability. While YoY growth is positive, the sharp sequential decline in net profit signals potential headwinds that require careful monitoring.

In-Depth Hansol Logistics Analysis: Fundamentals & Risks

To understand the full picture, we must look beyond the quarterly numbers and examine the foundational strengths and weaknesses of the company.

Positive Factors: A Solid Foundation

- •Robust H1 2025 Performance: Revenue for the first half of the year grew 3.5% YoY, driven by comprehensive logistics services and expanding overseas subsidiaries.

- •Impressive Net Profit Growth: H1 2025 net profit soared by 32% YoY, aided by lower tax expenses and other non-operating income.

- •Stable Financial Structure: The company has demonstrated financial discipline, growing its total equity and slightly improving its debt-to-equity ratio.

- •Diversified Business & Certifications: A strong portfolio spanning international logistics, transport, and W&D, backed by AEO and ISO certifications, enhances market trust and resilience.

Negative Factors & Potential Risks

- •Margin Compression: Despite revenue growth in H1, operating profit declined, raising questions about cost control and pricing power. This is a critical area for a successful logistics investment.

- •High Debt-to-Equity Ratio: At 99.9%, the company’s debt load is significant. In an environment of fluctuating interest rates, this could become a major financial burden.

- •Market Volatility: The logistics industry is inherently sensitive to external shocks like shipping rate fluctuations, geopolitical events (e.g., the Red Sea crisis), and volatile oil prices.

- •Customer Concentration: A high dependence on a single key customer, Hansol Paper Co., Ltd., poses a concentration risk to revenue stability.

Future Outlook & Macroeconomic Headwinds

Hansol Logistics does not operate in a vacuum. Its future performance is closely tied to global economic trends. According to leading economic forecasts, persistent inflation and high interest rates continue to impact financial costs and consumer demand worldwide. Volatility in currency exchange rates and international oil prices directly affects the company’s bottom line by increasing transport and operational costs. For a deeper understanding of these market forces, you can explore our guide to logistics sector analysis.

In the short term, the market’s reaction to the Hansol Logistics Q3 2025 earnings may be negative due to the profitability dip. The mid-to-long-term valuation will hinge on the company’s ability to manage costs effectively, sustain its overseas growth, and navigate the challenging macroeconomic landscape.

Investor Action Plan: A ‘Neutral’ Stance with Key Watch Points

Given the balance of positive long-term fundamentals and negative short-term pressures, a ‘Neutral’ investment opinion on Hansol Logistics is prudent at this time. The H1 growth is encouraging, but the Q3 slowdown, combined with a high debt ratio and market volatility, calls for a cautious, wait-and-see approach.

Investors should keep a close eye on the following key areas in the upcoming quarters:

- •Q4 Earnings Report: Will the company reverse the revenue decline and stabilize its operating profit margin? The next report will be crucial.

- •Cost Efficiency Initiatives: Look for management commentary on specific strategies to control costs and improve profitability.

- •Overseas Business Performance: Continued strong growth from international subsidiaries is vital to offset any domestic weakness and drive long-term value.

- •Debt Management: Any steps taken to reduce the debt-to-equity ratio would be a strong positive signal.

In conclusion, while the Hansol Logistics Q3 2025 earnings report raises some flags, the company’s underlying strengths should not be overlooked. A patient and observant investment approach is the most sensible path forward.