Analyzing the Landmark Seondo Electric Contract with KEPCO

The recent announcement of the Seondo Electric contract has sent ripples through the market. Seondo Electric (KRX: 007610) officially secured a significant ₩3.3 billion single sales and supply agreement with the Korea Electric Power Corporation (KEPCO), a cornerstone of South Korea’s energy infrastructure. This deal, representing a substantial 13.72% of the company’s 2024 revenue, raises a critical question for investors: is this a genuine turning point for the company or merely a temporary boost? This comprehensive analysis will delve into the contract’s specifics, Seondo Electric’s underlying financial health, and the broader implications for its stock performance.

Contract Details: A ₩3.3 Billion Eco-Friendly Boost

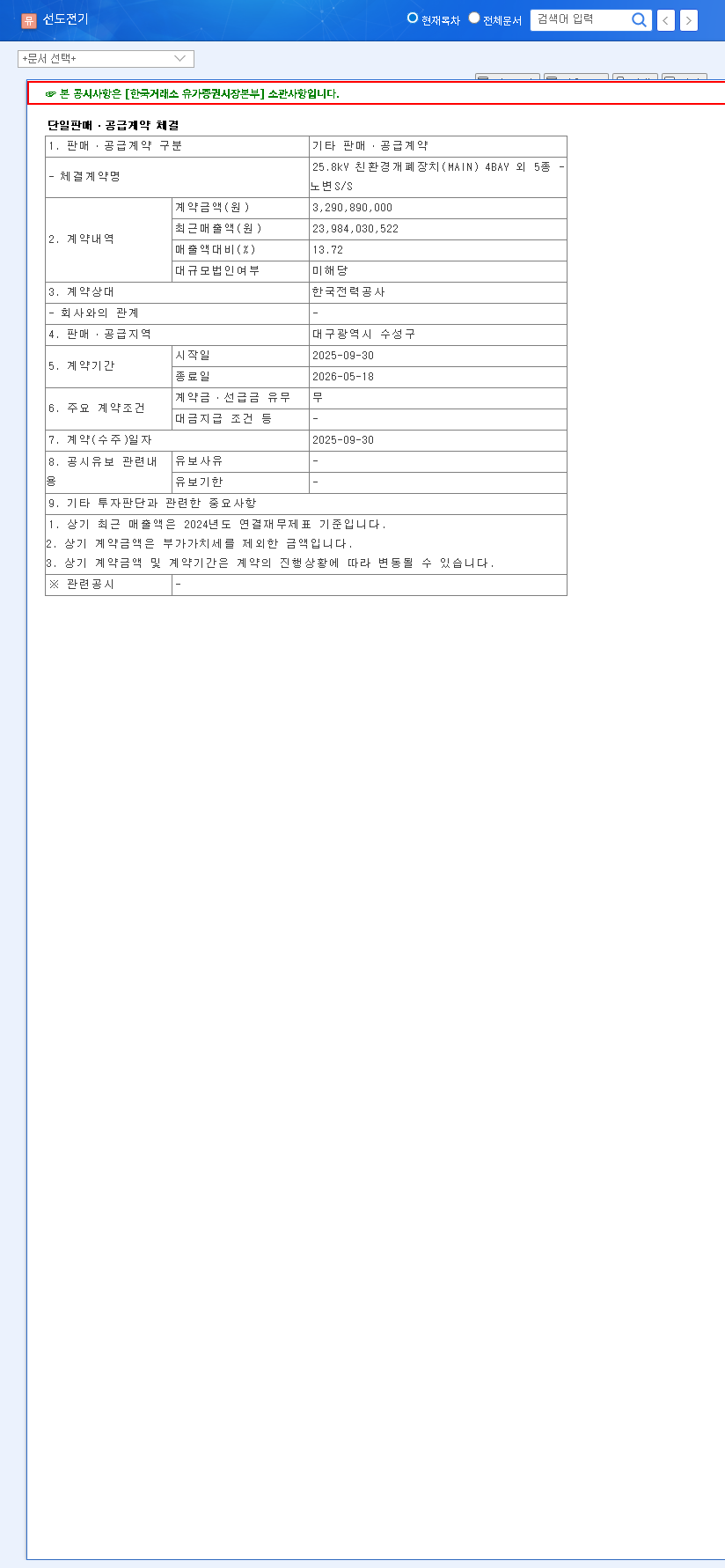

On September 30, 2025, Seondo Electric formalized the supply deal with KEPCO. The agreement centers on the provision of 25.8kV eco-friendly switchgear and other related items. This technology is crucial for modernizing power grids, enhancing safety, and reducing environmental impact. The key details of this pivotal agreement are outlined below:

- •Counterparty: Korea Electric Power Corporation (KEPCO)

- •Contract Value: ₩3.3 billion KRW

- •Contract Period: September 30, 2025, to May 18, 2026 (approx. 7.5 months)

- •Revenue Impact: 13.72% of 2024’s revenue (₩23.267 billion KRW)

- •Supply Region: Suseong-gu, Daegu Metropolitan City

This information is based on the company’s public filing. For complete transparency, investors can review the Official Disclosure (DART Report).

Financial Health: A Tale of Two Stories

While this KEPCO contract is undoubtedly a positive development, it’s crucial to place it within the context of Seondo Electric’s broader financial situation. The company faces significant headwinds that this single deal, however large, may not entirely mitigate.

The Upside: A Much-Needed Lifeline

The immediate impact is clear. A guaranteed revenue stream of this magnitude will bolster short-term performance and improve the company’s order book. Partnering with a stable, public-sector entity like KEPCO enhances credibility and demonstrates Seondo Electric’s technical capabilities. This revenue injection is expected to flow through to operating profit, assuming costs for raw materials and labor can be managed effectively.

The Challenge: Deep-Rooted Financial Risks

Investors performing a Seondo Electric stock analysis must look beyond this single contract. In 2024, the company saw its revenue decline by 44.3% year-over-year, culminating in an operating loss of ₩5.748 billion. This downturn is a result of a wider industry slump and rising material costs. More critically, the company’s current liabilities exceed its current assets, raising concerns about its ability to continue as a going concern. While management is pursuing financial restructuring, the clock is ticking, with an improvement period for its listing eligibility set to expire in April 2025.

The ₩3.3 billion KEPCO contract provides a crucial revenue boost, but it must be viewed against a backdrop of significant financial challenges and an urgent need to secure long-term stability and profitability.

Macroeconomic & Strategic Outlook

No company operates in a vacuum. Seondo Electric’s future will also be shaped by external forces. Volatility in the KRW/USD exchange rate can inflate the cost of imported raw materials, squeezing margins. Furthermore, while the trend towards eco-friendly infrastructure is a major tailwind, as noted by organizations like the International Energy Agency (IEA), the company must navigate fluctuating commodity prices and global interest rate policies that can impact capital investment.

Strategically, the Seondo Electric contract serves as a powerful proof of concept for its green technology, potentially opening doors to further public and private sector projects focused on grid modernization.

Action Plan for Investors: A ‘Conservatively Positive’ Stance

Given the circumstances, a ‘conservatively positive’ outlook is warranted. The contract will likely provide a short-term lift to investor sentiment and the stock price. However, long-term success hinges on the company’s ability to address its fundamental financial weaknesses. Sustainable recovery requires more than one successful deal.

Key Monitoring Points for Seondo Electric 007610

- •Profitability Tracking: Closely monitor quarterly reports to see if this contract’s revenue translates into actual profit and positive cash flow.

- •New Order Pipeline: Look for announcements of additional contracts to demonstrate sustained business momentum beyond the KEPCO deal.

- •Listing Eligibility Progress: Pay strict attention to any news regarding the resolution of listing eligibility issues before the April 2025 deadline.

- •Financial Health Metrics: For a deeper dive, read our guide on Understanding Financial Health in the Electrical Components Industry.

Leave a Reply