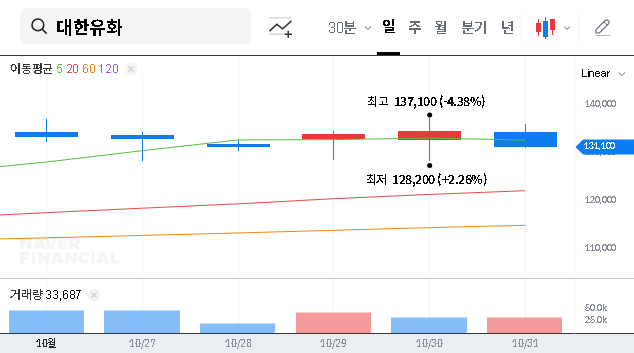

In a stunning announcement that sent ripples through the financial markets, KOREA PETRO CHEMICAL IND CO.,LTD (대한유화), hereafter referred to as KPC, revealed its preliminary Q3 2025 results on October 31, 2025. The report showcased a remarkable ‘earnings surprise’, with operating profits soaring an astonishing 161% above market consensus. This analysis unpacks the impressive KOREA PETRO CHEMICAL IND CO.,LTD earnings, exploring the strategic pillars behind this success and what it signals for the company’s future trajectory.

This 161% beat isn’t just a number; it’s a powerful statement of strategic resilience, operational excellence, and a well-executed turnaround story in a challenging global market.

KPC’s Q3 2025 Earnings: The Numbers at a Glance

KPC’s performance didn’t just meet expectations; it shattered them. The company demonstrated robust health across all key metrics, continuing the positive momentum from its return to profitability in Q1 2025. Here’s a breakdown of the headline figures:

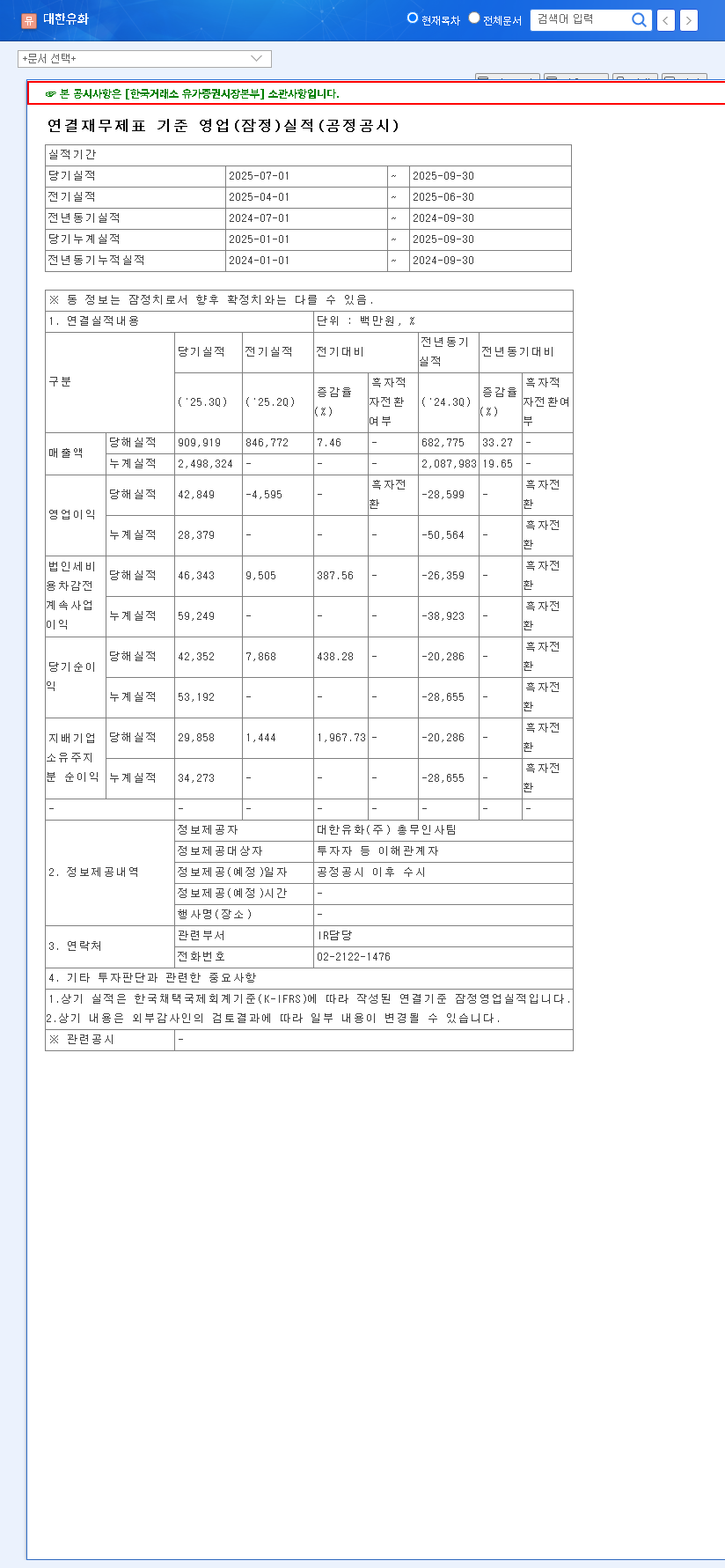

- •Revenue: KRW 909.9 billion, a 1% beat versus the estimated KRW 904.4 billion.

- •Operating Profit: KRW 42.8 billion, a massive +161% overperformance compared to the estimated KRW 16.4 billion.

- •Net Profit: KRW 29.9 billion, a +134% surprise against the estimated KRW 12.8 billion.

These preliminary results, detailed in the company’s Official Disclosure on DART, underscore a significant operational turnaround and highlight the company’s ability to navigate market complexities effectively.

The Core Drivers Behind the Stellar Performance

KPC’s success is not a stroke of luck but the result of a multi-faceted strategy combining internal fortification with the capitalization of favorable market conditions. Let’s explore the key drivers.

1. Strategic Synergy with Hanju Co., Ltd.

The integration of its consolidated subsidiary, Hanju Co., Ltd., has been a masterstroke, significantly boosting external revenue. The utility segment, driven by Hanju, is becoming a cornerstone of KPC’s growth. The recent completion of its first-phase LNG combined cycle power plant is a major step towards an eco-friendly energy transition, promising stable, long-term revenue streams that diversify KPC’s portfolio beyond the cyclical petrochemical market.

2. Mastering Efficiency in the Petrochemical Segment

Despite headwinds like volatile oil prices and a sluggish global economy, KPC drastically reduced the operating loss in its core petrochemical division. This achievement stems from rigorous cost management and the stable, efficient operation of its butadiene (BD) production facilities. By optimizing processes and likely securing more favorable feedstock contracts, the company has bolstered its margins and proven its resilience.

3. Expanding High-Value-Added Product Sales

The exceptional operating profit margin strongly suggests a successful strategic shift towards high-value-added products. This involves moving away from commodity-grade materials to specialized polymers and chemicals that command higher prices. This focus, backed by consistent R&D investment and patent acquisitions, solidifies KPC’s technological edge and future profitability. For a deeper understanding of market dynamics, you can review our analysis of the global petrochemical industry.

4. Capitalizing on Favorable External Factors

Several external tailwinds provided a welcome boost. The strong KRW/USD exchange rate positively impacted export profitability, while a decline in global logistics costs, evidenced by the falling China Container Freight Index, helped reduce operational expenses—a critical factor for a major exporter like KPC.

Future Outlook: Momentum and Potential Risks

The outstanding KPC Q3 2025 results are expected to fuel positive momentum, but savvy investors must also weigh the potential risks on the horizon.

- •Positive Impacts: The earnings surprise will likely enhance investor sentiment and could drive short-term stock appreciation. More importantly, it boosts market confidence in KPC’s management and strategic direction, solidifying its reputation as a competitive player.

- •Potential Risks: The key question is sustainability. The market will watch closely to see if this performance is a new baseline or a temporary peak. Persistent risks include global economic volatility, which could dampen demand, and the inherent instability of oil and naphtha prices. As noted in reports from leading financial news outlets, these macroeconomic factors remain a primary concern for the sector.

Frequently Asked Questions (FAQ)

What were KPC’s key Q3 2025 results?

KOREA PETRO CHEMICAL IND CO.,LTD reported revenue of KRW 909.9 billion, operating profit of KRW 42.8 billion (+161% vs. estimate), and net profit of KRW 29.9 billion (+134% vs. estimate), achieving a major earnings surprise.

What are the main reasons for this performance improvement?

Key factors include revenue growth from the Hanju Co., Ltd. subsidiary, significantly reduced losses in the petrochemical segment through cost control, and an increased sales mix of high-value-added products.

What risk factors should investors consider?

Investors should monitor the sustainability of this performance, volatility in oil and raw material prices, global economic conditions, exchange rate fluctuations, and the company’s debt levels.

In conclusion, the KOREA PETRO CHEMICAL IND CO.,LTD earnings for Q3 2025 have provided a compelling reason for market optimism. While continued vigilance is necessary, the company’s blend of strategic diversification and operational mastery positions it as a noteworthy entity for investors focused on long-term value and growth.

Leave a Reply