The recent DCKSUNG Indonesia expansion represents a pivotal moment for the South Korean synthetic leather giant. As DCKSUNG CO.,LTD confronts weakening domestic fundamentals, its ₩13.8 billion acquisition of an Indonesian subsidiary is a bold move to secure a new growth engine. But is this a strategic masterstroke or a risky bet that could further strain its finances? This comprehensive analysis explores every facet of the deal to provide investors with a clear, data-driven perspective.

We will dissect the acquisition’s background, evaluate the potential rewards against the inherent risks, analyze the macroeconomic landscape, and offer a conclusive investment recommendation for DCKSUNG CO.,LTD.

The Landmark Announcement: A New Chapter in Indonesia

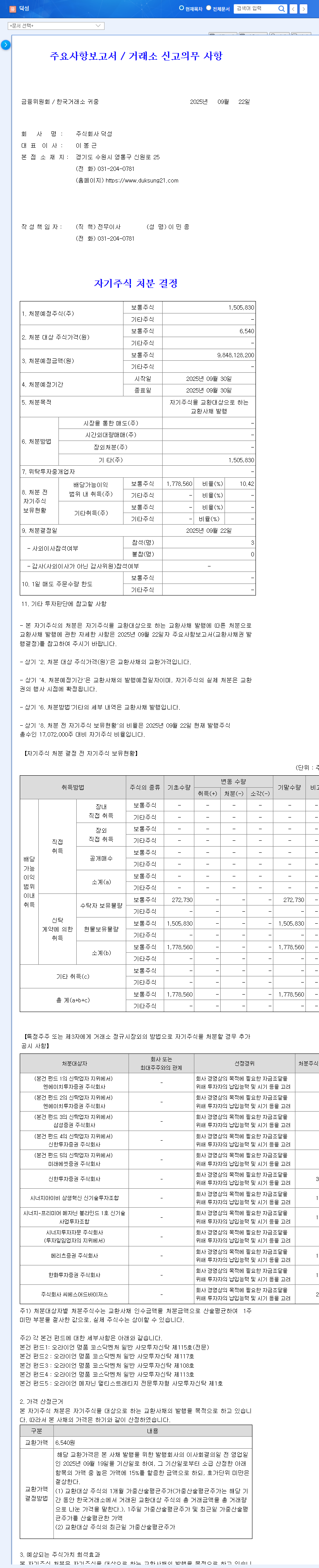

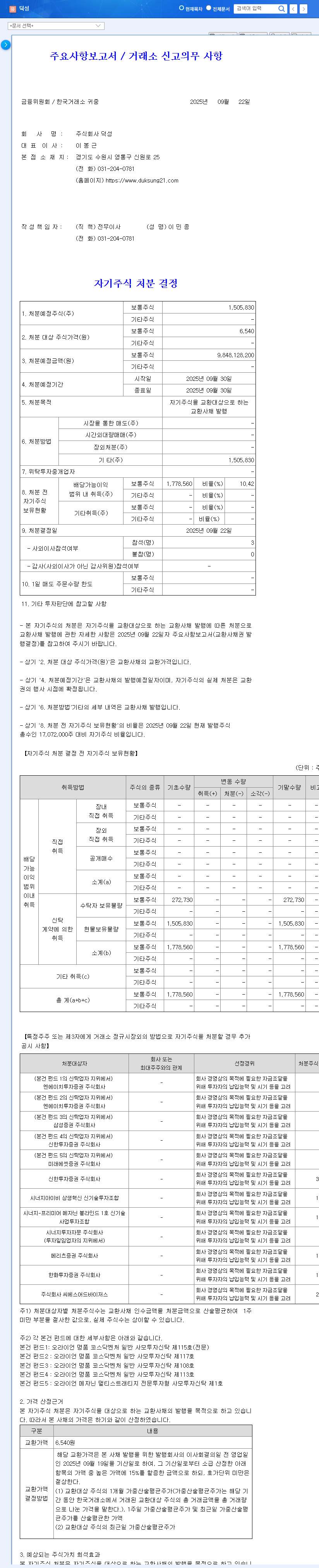

On November 6, 2025, DCKSUNG CO.,LTD officially disclosed its decision to acquire a 99.9% stake in the newly formed PT. DUKSUNG ECOTECH INDONESIA. The ₩13.8 billion (approx. 15% of total capital) cash investment, detailed in the Official Disclosure (DART), is a strategic play to penetrate the burgeoning Southeast Asian synthetic leather market. The final acquisition is slated for completion by December 31, 2026.

This isn’t just an acquisition; it’s a calculated pivot towards global markets, designed to offset domestic challenges and unlock new revenue streams in one of the world’s most dynamic economic regions.

Why Now? The Rationale Behind the Expansion

The timing of the DCKSUNG Indonesia expansion is driven by a combination of internal pressures and external opportunities. Understanding both is key to evaluating the strategy.

Internal Pressures: Weakening Financial Health

DCKSUNG’s financial performance in the first half of 2025 painted a concerning picture, necessitating a strategic breakthrough:

- •Declining Revenue: H1 2025 revenue fell to ₩73.9 billion, a sharp 41% decrease year-over-year.

- •Shrinking Profitability: Operating profit dropped by 43.4% to ₩5.04 billion, with the profit margin contracting from 6.8% to 5.1%.

- •Rising Debt Concerns: A staggering 282.6% increase in short-term borrowings has raised red flags regarding financial soundness, despite a manageable debt-to-equity ratio.

External Opportunity: The Indonesian Market Potential

Indonesia presents a compelling case. As a major manufacturing hub for global footwear and apparel brands, it offers a large, growing domestic market for synthetic leather. By establishing a local presence, DCKSUNG aims to gain a competitive edge through reduced logistics costs, local sourcing, and proximity to major clients. This move aligns with broader trends in our analysis of the synthetic leather market, which points to significant growth in Southeast Asia.

A Balanced Scorecard: Risks vs. Rewards

Any major international venture carries a mix of potential upsides and significant risks. The DCKSUNG Indonesia expansion is no exception.

Potential Positives (The Rewards)

- •New Growth Engine: Tapping into the ASEAN market can offset declining domestic sales and create a vital new revenue stream.

- •Enhanced Competitiveness: Local production reduces shipping costs and tariffs, allowing for more competitive pricing for global brands manufacturing in the region.

- •Risk Diversification: Geographic expansion reduces dependence on the South Korean market and mitigates regional economic risks.

Potential Negatives (The Risks)

- •Financial Strain: The ₩13.8 billion cash outlay could exacerbate existing financial weaknesses and increase liquidity risk in the short term.

- •Execution & Integration: Navigating cultural differences, local regulations, and integrating a new workforce presents significant operational challenges.

- •Currency Volatility: Fluctuations between the Indonesian Rupiah (IDR) and the Korean Won (KRW) could adversely affect profitability and the value of repatriated earnings.

Investor Action Plan & Final Recommendation

Given the high stakes, a cautious and informed approach is essential. While the long-term strategic vision is sound, the short-term execution risks are substantial. The market, as noted by sources like Reuters, remains skeptical pending tangible results.

Investment Opinion: Conservative Approach Recommended. The potential for future growth is clear, but it is overshadowed by the immediate financial burden and operational uncertainties. Investors should wait for concrete signs of successful integration and profitability from the Indonesian subsidiary before considering a position.

Key monitoring points for the future include:

- •Quarterly performance reports from PT. DUKSUNG ECOTECH INDONESIA.

- •Management’s progress on improving the core business’s profitability.

- •Updates on financial structure and debt management.

Ultimately, the success of the DCKSUNG Indonesia expansion will depend on meticulous execution, transparent communication with shareholders, and a swift return to financial stability. Until then, caution is the wisest course of action.