SEBANG GLOBAL BATTERY IR Event: A Pivotal Moment for Investors

The upcoming SEBANG GLOBAL BATTERY IR event, scheduled for November 6, 2025, represents a critical juncture for the company and its investors. As a dominant force in the lead-acid battery market, Sebang is navigating a complex transition towards the high-growth electric vehicle (EV) sector. This investor relations event is more than a simple earnings call; it’s a window into the company’s future, offering crucial insights into its Q3 performance, strategic direction, and readiness to tackle macroeconomic headwinds. For those conducting a thorough Sebang investment analysis, this event will be the ultimate test of the company’s long-term vision and execution capability.

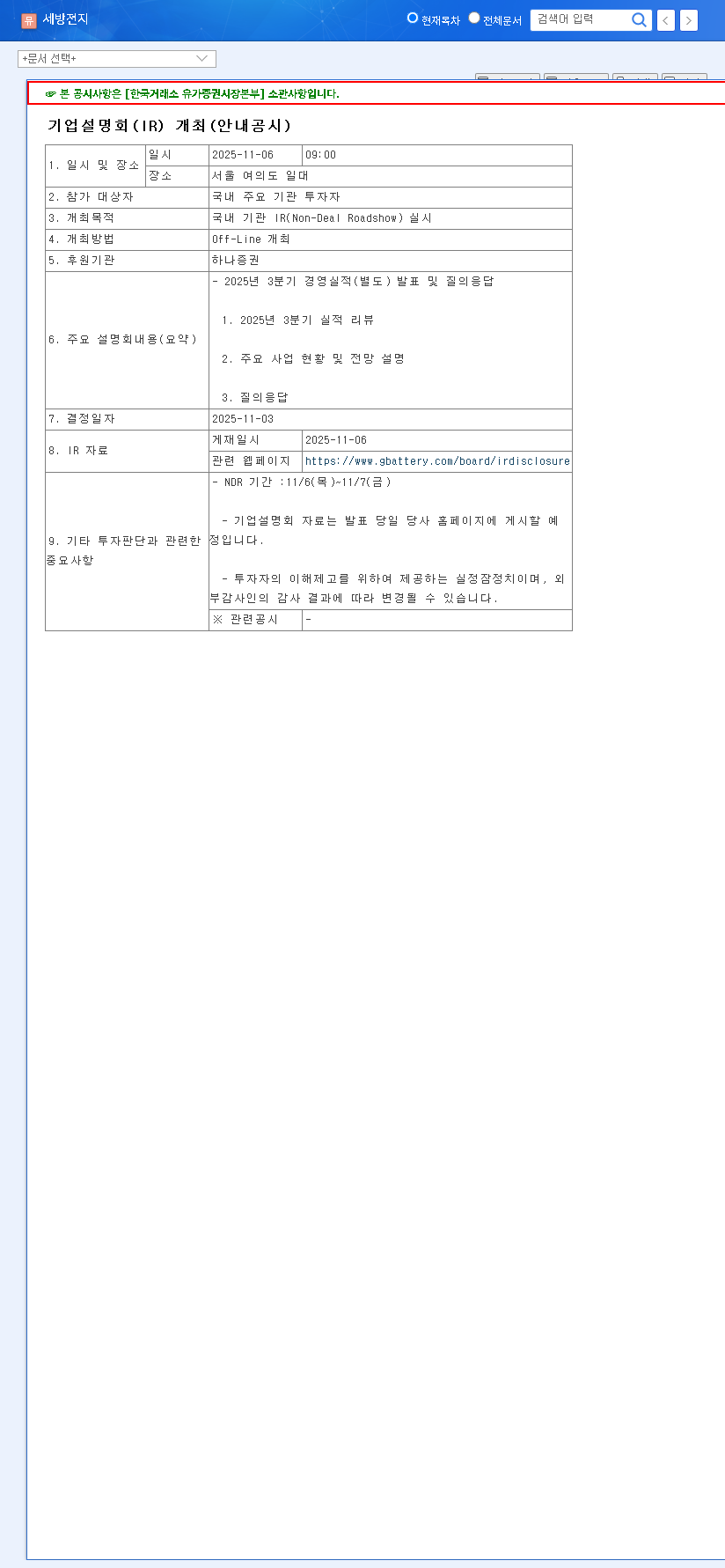

The event, targeting domestic institutional investors, will commence at 9:00 AM and cover Q3 2025 performance, a comprehensive business outlook, and an interactive Q&A session. Key details have been outlined in their Official Disclosure filed with DART.

Current Financial Health: A Tale of Growth and Pressure

A review of Sebang’s H1 2025 performance reveals a classic dilemma: impressive top-line growth coupled with shrinking profitability. While sales surged by 9.4% to KRW 1.078 trillion, driven by strong demand for both conventional and new battery products, operating profit fell by 17.4%. This highlights the intense pressure from external factors that investors must scrutinize during the SEBANG GLOBAL BATTERY IR.

Key Strengths to Consider

- •Robust Sales Momentum: Continued growth in core vehicle lead-acid batteries and emerging power auxiliary packs signals strong market demand.

- •Market Leadership: Unwavering dominance in the domestic lead-acid battery market provides a stable revenue foundation.

- •Future-Forward Investment: Ongoing R&D and facility investments demonstrate a commitment to innovation and scaling the Sebang EV battery strategy.

Significant Challenges and Risks

- •Profitability Squeeze: The decline in operating profit, attributed to US tariffs and currency fluctuations, is a primary concern.

- •High Dependency on Legacy Products: With lead-acid batteries still forming 85% of sales, the pressure is on the EV segment to accelerate growth.

- •Financial Leverage: A relatively high debt-to-equity ratio (230.13%) could limit financial flexibility in a volatile market. For more on this, read our guide to analyzing corporate debt.

The core question for investors is whether Sebang can successfully leverage its established manufacturing prowess to build a profitable, large-scale EV battery business that can offset the margin pressures in its legacy operations.

Navigating External Economic Volatility

As a major exporter, Sebang’s performance is intrinsically linked to global macroeconomic trends. The company’s strategy for mitigating these risks will be a focal point of the IR presentation.

- •Currency Headwinds: The rising USD/KRW exchange rate directly inflates costs and creates potential foreign exchange losses. Investors will look for details on hedging strategies.

- •Raw Material Costs: While lead (Pb) prices have moderated, volatility in other commodities and rising global inflation could still pressure margins. Supply chain resilience is key.

- •Logistics Stabilization: A silver lining appears in logistics, with major freight indices trending downwards, which could provide some cost relief. For broader market context, see the latest reports from authoritative sources like Reuters.

Potential Stock Impact Post-IR Event

This SEBANG GLOBAL BATTERY IR event could serve as a major catalyst for the stock price, with outcomes hinging on the clarity and credibility of the management’s presentation.

The Bull Case (Positive Scenario)

A positive re-rating could occur if management delivers a detailed and convincing roadmap for its Sebang EV battery strategy, demonstrates tangible progress in improving profit margins despite headwinds, and provides transparent, confidence-boosting forward guidance. This could enhance investor sentiment and attract new capital.

The Bear Case (Negative Scenario)

Conversely, the stock could face downward pressure if the Sebang Q3 earnings fall significantly below expectations, if the EV strategy lacks specifics, or if the company fails to present a robust plan to counter external risks. Highlighting increased competition or R&D burdens without a clear path to profitability could also trigger a negative reaction.

Actionable Investor Checklist for the IR

To make an informed decision, investors should approach the SEBANG GLOBAL BATTERY IR with a clear checklist of questions to be answered:

- •Profitability Plan: What specific, measurable steps is management taking to improve operating margins?

- •EV Business Vision: How does Sebang plan to compete in the crowded EV battery market? What is their technological edge and timeline for scaling?

- •Risk Mitigation: What are the company’s concrete strategies for managing currency, raw material, and geopolitical risks?

- •Capital Allocation: How will future cash flows be allocated between debt reduction, R&D, and shareholder returns?

By closely monitoring the company’s answers to these points and observing the subsequent market reaction, you can position yourself to make a well-reasoned investment decision. This event offers a rare opportunity for a comprehensive Sebang investment analysis based on the latest company data and forward-looking statements.

Leave a Reply