The latest SONGWON INDUSTRIAL earnings report for Q3 2025 has sent ripples through the investment community. After a challenging first half of the year, the company’s preliminary report shows a significant turnaround to profitability. While this news is a welcome sign of recovery, seasoned investors are asking the critical question: Is this a sustainable rebound or merely a temporary reprieve from deeper structural challenges? This comprehensive SONGWON INDUSTRIAL financial analysis will dissect the numbers, evaluate the underlying fundamentals, and provide a clear outlook on what lies ahead for ticker 004430.

Dissecting the Q3 2025 SONGWON INDUSTRIAL Earnings Report

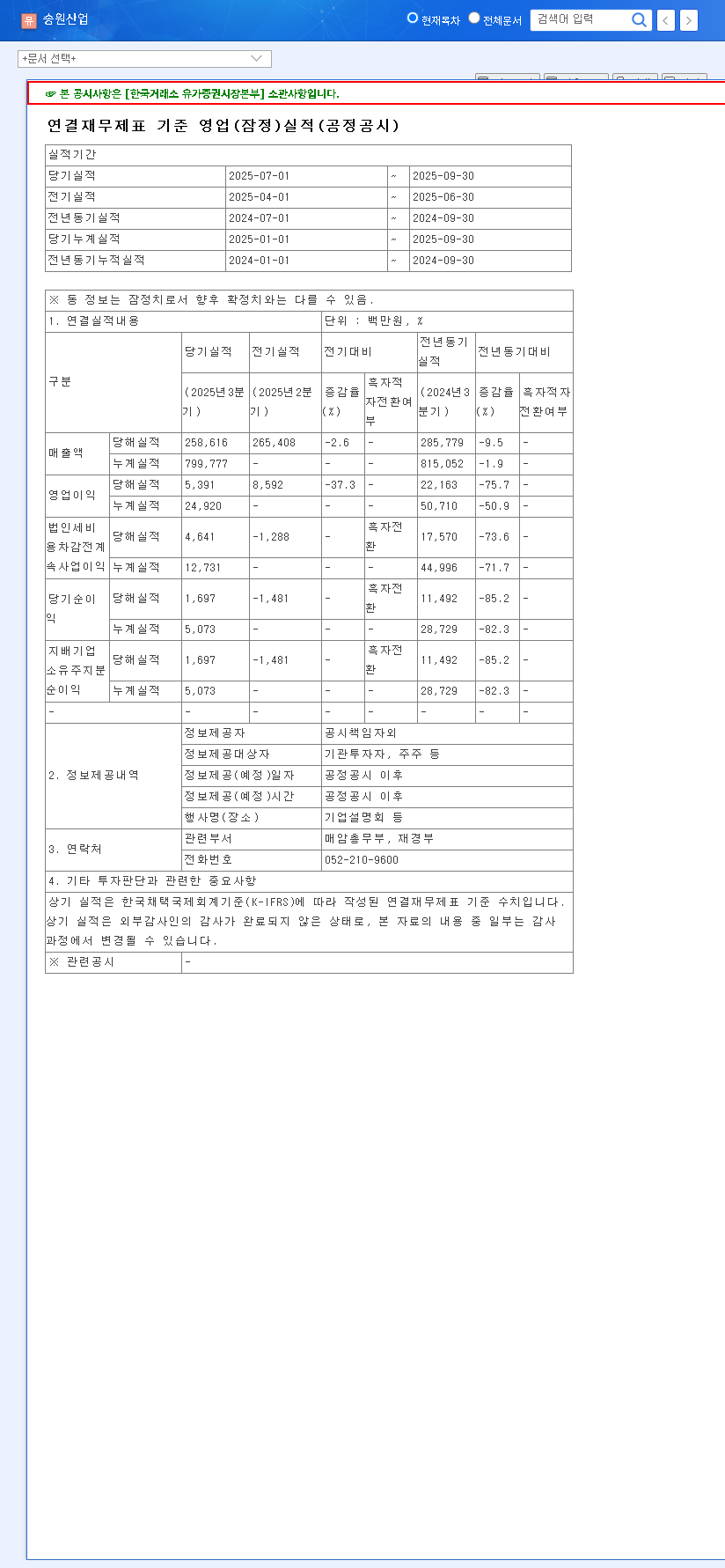

On October 31, 2025, SONGWON INDUSTRIAL CO., LTD (004430) released its preliminary Q3 earnings, which marked a pivotal shift from the losses reported in Q1 and Q2. The key figures, as per the official disclosure, reveal a notable improvement in operational efficiency. (Source: Official DART Disclosure)

- •Revenue: KRW 258.6 billion

- •Operating Profit: KRW 5.4 billion (A significant turnaround to profitability)

- •Net Income: KRW 1.7 billion (Return to positive territory)

This return to the black is primarily attributed to two factors: the reduced impact of one-time costs associated with ordinary wage provisions that heavily impacted Q2, and a modest recovery in demand for specific product lines. However, a slight quarter-over-quarter revenue decrease suggests that top-line growth remains a challenge.

While the Q3 turnaround is a positive signal, it’s essential to look beyond the headline numbers. The core issue remains whether SONGWON has addressed the fundamental weaknesses that led to the earlier slump.

In-Depth Analysis: Structural Strengths vs. Persistent Headwinds

To truly understand the company’s trajectory, we must weigh the positive Q3 results against the persistent challenges identified in previous quarters and the broader market environment. The global chemical industry outlook remains complex.

1. Profitability and Cost Structure Concerns

The pressure on margins is a multi-faceted problem. While the one-time wage costs have subsided, the Supreme Court ruling has created a new, higher baseline for structural labor costs, which will continue to impact profitability. Furthermore, sluggish global demand, particularly in key markets, and geopolitical tensions have led to cautious purchasing behavior from customers, compressing margins. There’s a clear performance gap between SONGWON’s divisions: industrial chemicals like polymer stabilizers face intense competition and weak demand, while functional chemicals (TPU, SPU) are showing more resilience.

2. Financial Health and Cash Flow Red Flags

A look at the balance sheet reveals areas requiring diligent management. A high inventory-to-revenue ratio suggests that working capital is tied up and poses a risk of write-downs if demand doesn’t materialize. The year-on-year increase in interest-bearing debt is particularly concerning in a rising interest rate environment, as it leads to higher interest expenses that eat into net income. The negative operating cash flow seen in Q2, driven by lower profits and higher inventory, needs to be reversed. Investors will be keenly watching the full Q3 report to see if this trend has improved. Finally, a slowdown in capital expenditures could hinder the development of future growth drivers, a critical component for long-term competitiveness in the chemical sector.

3. Macroeconomic and Competitive Landscape

SONGWON does not operate in a vacuum. The broader economic climate presents significant risks. Lingering concerns over China’s economic slowdown and ongoing geopolitical instability, as noted by leading economic analysts, continue to suppress global demand for chemicals. Volatility in raw material prices (PHENOL, TBA, etc.) and major currency exchange rates (USD, EUR) directly impacts the company’s cost of goods sold and profitability. On the competitive front, the polymer stabilizer market is highly contested, while the push for eco-friendly PVC stabilizers adds R&D pressure. Moreover, the increasing presence of low-cost Chinese competitors in the functional chemicals space threatens market share and pricing power.

Future Outlook & Investor Action Plan

Given the mixed signals, a neutral, wait-and-see approach is prudent. The Q3 earnings provide a short-term positive catalyst and a potential bottom for the company’s performance. However, long-term, sustainable growth for SONGWON INDUSTRIAL hinges on its ability to execute on key strategic imperatives.

Key Items for Investors to Monitor:

- •Q4 Earnings & 2026 Guidance: This will be the ultimate test of the recovery’s sustainability. Look for continued profitability and a positive outlook from management.

- •Margin Improvement: Monitor gross and operating margins to see if the company can effectively manage its cost structure and maintain pricing power.

- •Cash Flow Generation: Check for a return to positive operating cash flow, indicating efficient management of working capital, especially inventory.

- •Growth in Functional Chemicals: Track the performance of high-value segments like TPU/SPU, which are crucial for diversifying revenue and improving overall profitability.

In conclusion, while the Q3 2025 SONGWON INDUSTRIAL earnings offer a glimmer of hope, the path ahead is fraught with challenges. Careful and continuous monitoring of the key financial and operational metrics listed above is essential before making any investment decisions.