The latest ILSHIN SPINNING CO.,LTD earnings report for the third quarter of 2025 has revealed significant challenges, causing concern among investors. While revenue saw a marginal increase, a sharp and unexpected decline in operating profit has cast a shadow over the company’s short-term outlook. This comprehensive analysis will dissect the Q3 2025 results, explore the underlying causes for the performance dip, and outline a prudent investment strategy for navigating the path ahead.

Breaking Down the ILSHIN SPINNING CO.,LTD Q3 2025 Earnings Report

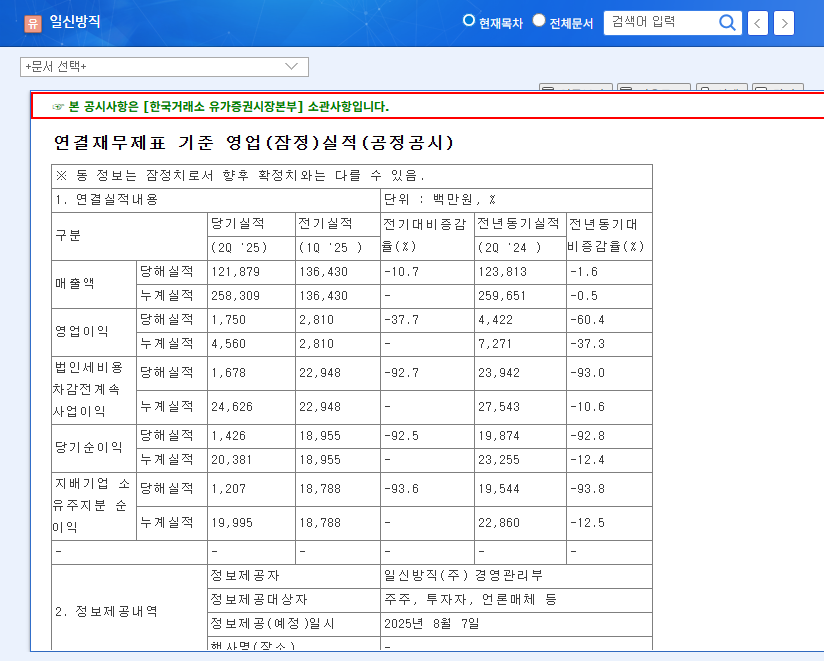

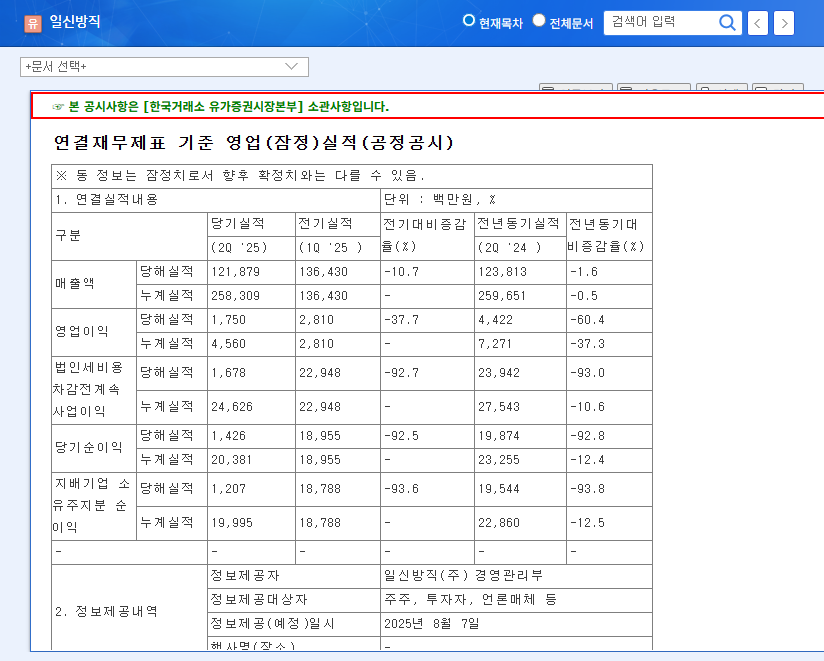

On November 10, 2025, ILSHIN SPINNING CO.,LTD released its provisional financial results, providing a critical snapshot of its health. The market reacted swiftly to the numbers, which pointed to a clear deterioration in profitability. The official figures, as filed with the regulator, can be found in the Official Disclosure on DART.

Here are the key takeaways from the announcement:

- •Revenue: KRW 124.3 billion, showing a minor increase from the previous quarter.

- •Operating Profit: KRW 0.9 billion, a significant and concerning plunge compared to the prior quarter.

- •Net Profit: KRW 1.1 billion, also marking a sequential decrease.

The dramatic fall in ILSHIN SPINNING operating profit is the central story of this report. It marks the second straight quarter of decline and signals deep-seated issues that revenue growth alone cannot mask.

Core Factors Behind the Profitability Decline

The weak performance isn’t due to a single issue but a convergence of internal business struggles and harsh external economic conditions. Understanding these factors is crucial for any ILSHIN SPINNING stock analysis.

Persistent Headwinds in the Core Textile Business

The company’s primary textile segment has been underperforming for some time, posting an operating loss of KRW 3.6 billion in the first half of 2025. The Q3 results suggest this trend has continued, if not worsened. Structural issues within the global textile industry, coupled with sluggish domestic and international demand, have compressed margins and limited growth.

Challenging Macroeconomic Environment

A perfect storm of macroeconomic factors has exacerbated the company’s problems. As reported by leading financial outlets like Bloomberg, the global economic climate has been unforgiving.

- •Adverse Exchange Rates: High EUR/KRW and USD/KRW rates directly increase the cost of importing essential raw materials like cotton, squeezing profitability at the source.

- •High Interest Rates: Elevated benchmark rates in both Korea and the U.S. amplify financial costs, making debt servicing more expensive and pressuring the bottom line.

- •Raw Material Volatility: Fluctuations in the price of crude oil and other key inputs create uncertainty and make cost management a significant challenge.

The Real Estate Business: A Stabilizing Force

On a more positive note, the company’s real estate leasing and management division continues to be a reliable source of income. It generated KRW 6.2 billion in operating profit during H1 2025, providing a crucial buffer against the losses in the textile segment. However, its stable contribution was not enough to offset the severe downturn in the core business, highlighting the need for diversification or a textile turnaround.

A Prudent Investment Strategy for ILSHIN SPINNING

Given the recent ILSHIN SPINNING CO.,LTD earnings, investors should adopt a cautious and observant stance. While short-term volatility and downward pressure on the stock price are likely, a long-term perspective requires monitoring several key indicators. For more background, you can read our guide to investing in the South Korean textile industry.

- •Textile Turnaround Strategy: Watch for any new management initiatives, cost-cutting measures, or shifts in market strategy aimed at reviving the core business in Q4 and beyond.

- •Diversified Business Growth: Monitor the performance of other ventures, such as cosmetics and alcoholic beverages, to see if they can become meaningful growth engines.

- •Macroeconomic Response: Assess the company’s risk management and its ability to adapt to ongoing changes in currency exchange rates and interest rates.

- •Shareholder Value: Pay attention to the company’s dividend policy and any other actions taken to enhance shareholder returns, as this can indicate management’s confidence.

Frequently Asked Questions (FAQ)

What were the key figures from ILSHIN SPINNING’s Q3 2025 earnings?

ILSHIN SPINNING reported revenue of KRW 124.3 billion, an operating profit of just KRW 0.9 billion, and a net profit of KRW 1.1 billion. The most notable figure was the sharp decline in operating profit from the previous quarter.

What is the primary cause of the poor operating profit?

The decline is attributed to a combination of persistent struggles in its core textile business and significant macroeconomic pressures, including high raw material costs, unfavorable currency exchange rates, and rising interest rates.

What is the expected impact on ILSHIN SPINNING’s stock price?

In the short term, the disappointing earnings are likely to increase market concerns and put downward pressure on the stock price. A long-term recovery will depend on a fundamental turnaround in its core operations and overall market conditions.