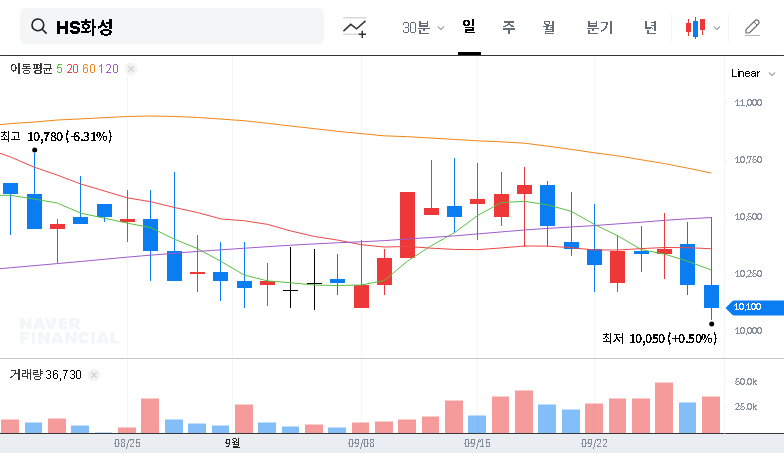

The announcement of the new HS HWASUNG reconstruction project has sent a significant signal through the investment community, especially given the current headwinds in the broader Korean construction market. HS HWASUNG CO., LTD. has successfully secured a landmark contract for the ‘Sinsung Yeonlip Small-scale Reconstruction Project,’ a deal valued at a substantial ₩102.3 billion. This development represents a critical moment for the company, and for investors, it begs the question: is this the catalyst for a major re-evaluation of HS HWASUNG stock?

This comprehensive investor analysis will dissect the contract’s details, explore the multifaceted impact on HS HWASUNG’s corporate value, weigh the potential risks, and provide a clear roadmap of key indicators to monitor moving forward.

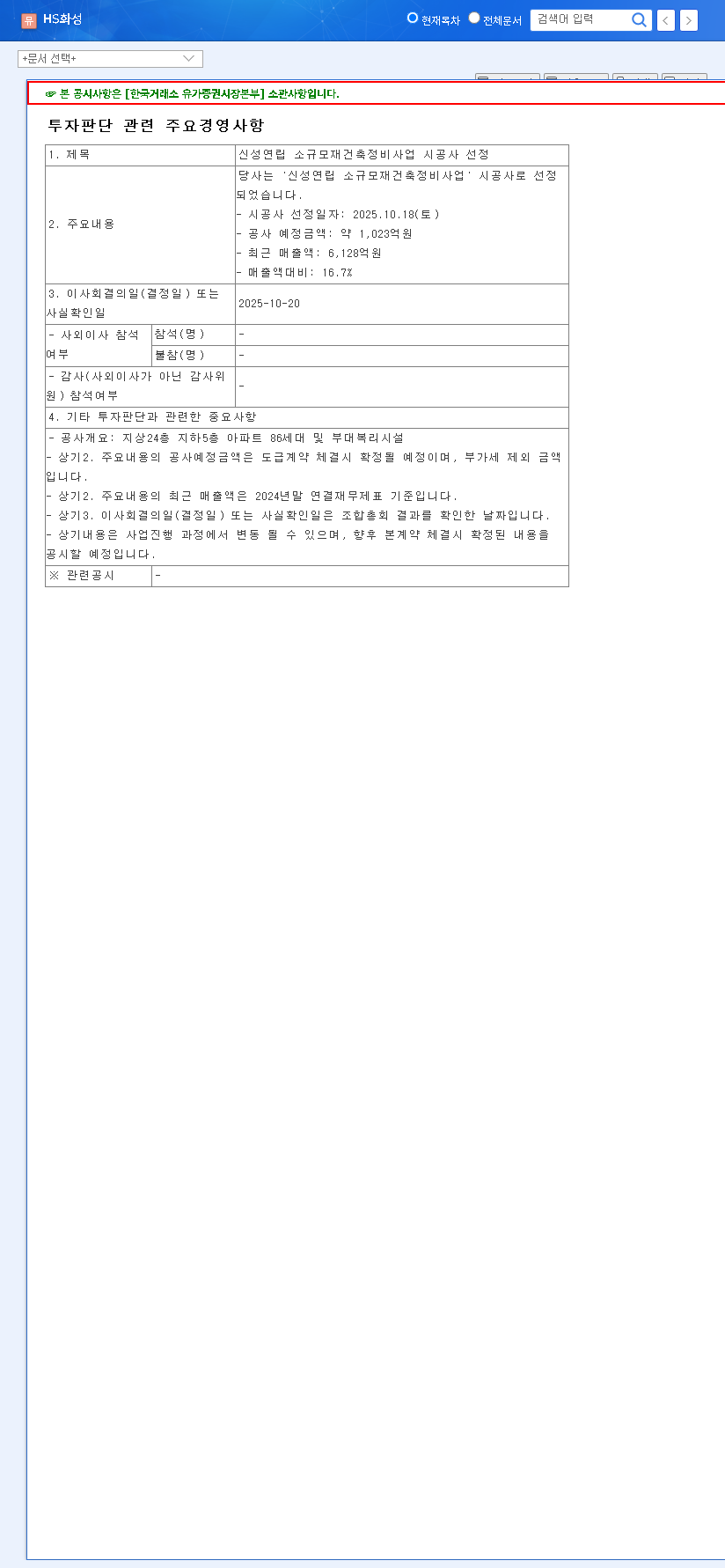

Unpacking the ₩102.3 Billion Sinsung Yeonlip Deal

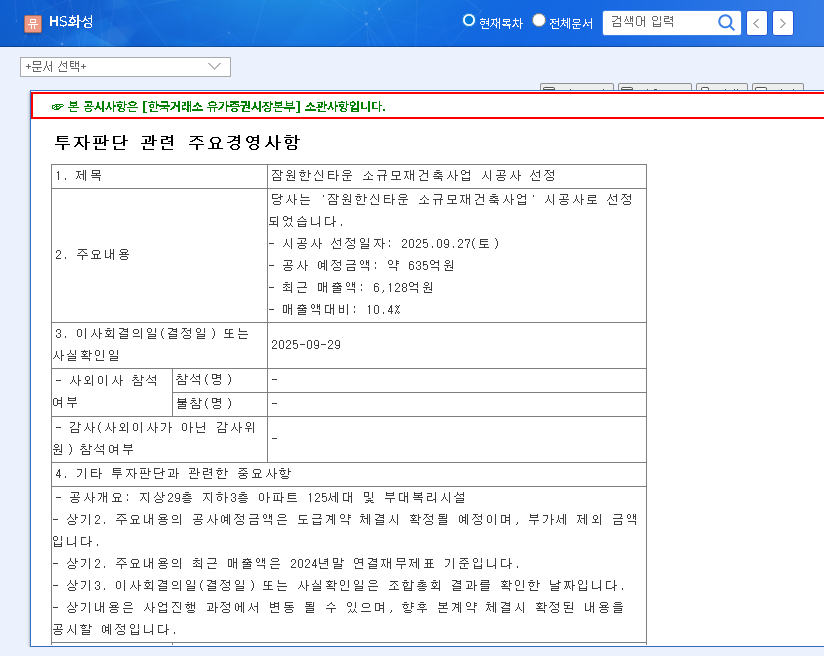

On October 20, 2025, HS HWASUNG officially disclosed its selection as the primary constructor for this pivotal urban regeneration project. The contract, with a formidable value of approximately ₩102.3 billion, is not merely another line item in their order book. It accounts for a staggering 16.7% of the company’s recent annual revenue of ₩612.8 billion. The full details of this significant agreement were made public via an Official Disclosure (DART Report), providing transparency for the market.

The ‘Sinsung Yeonlip’ project focuses on the redevelopment of an older low-rise apartment complex into a modern, high-value residential area. Such small-scale reconstruction projects are becoming increasingly important in mature urban centers, representing a stable and growing niche within the often-volatile construction sector.

“This win is more than just a financial boost; it’s a strategic validation of HS HWASUNG’s expertise in the complex urban regeneration space. Securing a project of this scale showcases their competitive edge and builds immense trust for future bids.”

The Bull Case: Positive Catalysts for HS HWASUNG Stock

For investors, the implications of this contract are overwhelmingly positive and extend far beyond the headline number. A thorough investor analysis reveals several key growth drivers.

Strengthened Revenue Pipeline & Profitability

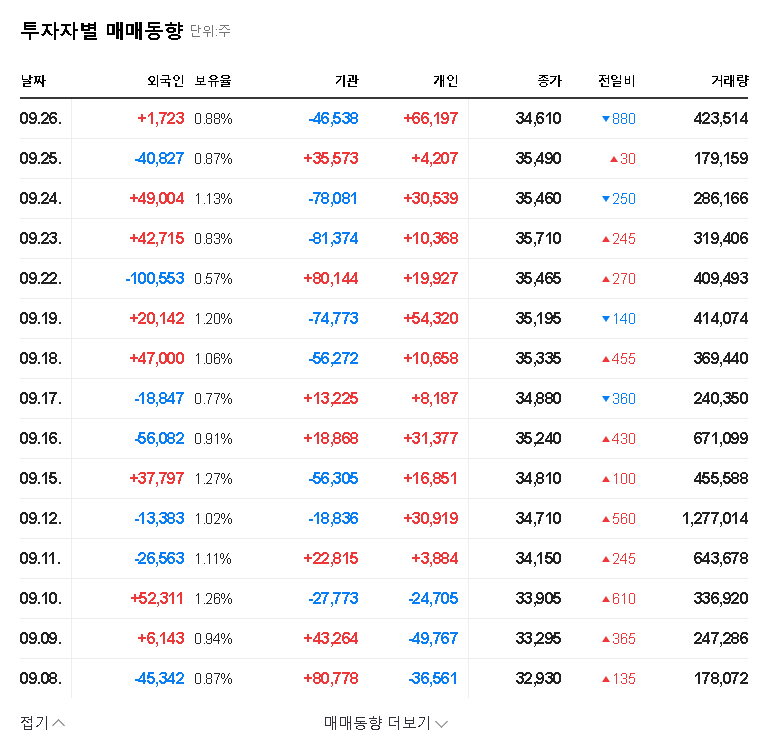

The most direct impact is the fortification of future revenue streams. This project provides a clear and stable source of income, significantly boosting the company’s order backlog and ensuring operational momentum for the coming years. This visibility is highly valued by investors, especially during periods of economic uncertainty.

Enhanced Market Position and Competitiveness

Successfully winning the Sinsung Yeonlip bid diversifies HS HWASUNG’s portfolio and demonstrates its capability in a lucrative market segment. It proves the company can compete and win against rivals, enhancing its brand reputation and making it a more formidable player in future tenders.

Navigating Headwinds: A Realistic Look at the Risks

While the outlook is bright, a prudent investor must also consider the inherent risks associated with large-scale construction ventures. Diligent management will be paramount for HS HWASUNG to translate this win into tangible profit.

- •Cost Control and Margin Pressure: The construction industry is susceptible to volatile raw material prices (steel, cement) and rising labor costs. Any unforeseen project delays or cost overruns could directly impact profitability, a key concern for any HS HWASUNG reconstruction project.

- •Financial & Operational Demands: A project of this magnitude requires significant upfront capital and flawless operational execution. Investors should monitor the company’s cash flow and debt-to-equity ratio to ensure financial health remains robust throughout the project’s lifecycle.

- •Macroeconomic Factors: Broader economic conditions, including interest rate fluctuations and government real estate policies, can influence the overall construction market. As major outlets like Bloomberg report, the global economic climate can impact domestic project viability.

Investor’s Roadmap: Monitoring HS HWASUNG’s Growth

For this positive development to translate into sustained growth for HS HWASUNG stock, investors should keep a close watch on several key performance indicators:

- •Quarterly Project Updates: Pay close attention to quarterly earnings reports for updates on the Sinsung Yeonlip project’s progress, budget adherence, and realized profit margins.

- •Financial Health Metrics: Continuously analyze the company’s balance sheet, focusing on cash flow from operations, debt levels, and overall liquidity.

- •New Order Announcements: The ability to leverage this success into securing additional reconstruction projects will be the ultimate test of sustained growth momentum.

Conclusion: A Strong Foundation for Future Growth

The ₩102.3 billion Sinsung Yeonlip deal is undeniably a significant positive catalyst for HS HWASUNG. It provides revenue stability, enhances market credibility, and validates its strategic focus on urban regeneration. While execution risk and market challenges remain, the successful management of this project could pave the way for a new era of growth and increased corporate value. For diligent investors, HS HWASUNG is certainly a company to watch closely in the coming quarters.