The latest KCC Corporation earnings report for the third quarter of 2025 has captured the market’s attention, revealing a mixed but intriguing financial picture. While top-line figures like sales and operating profit came in slightly below consensus, a surprising surge in net profit suggests a more complex story beneath the surface. This in-depth analysis will dissect the official results, explore the core fundamentals driving the company, and provide a comprehensive KCC stock analysis for investors considering its long-term potential.

We will examine the pivotal role of the KCC silicon business, weigh the opportunities against the risks, and offer a strategic outlook on what investors can expect next.

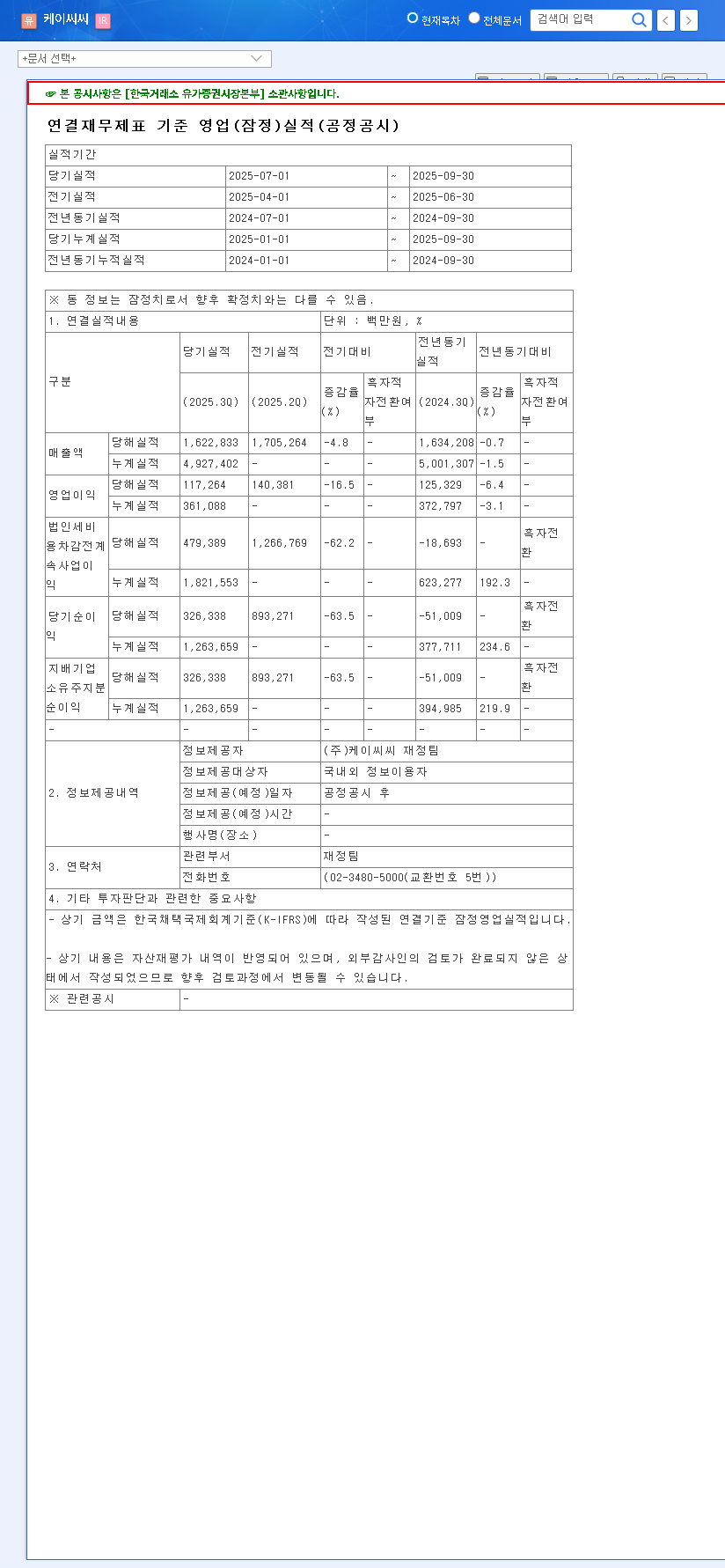

Dissecting the KCC Corporation Q3 2025 Earnings Report

For Q3 2025, KCC Corporation announced preliminary consolidated sales of KRW 1,622.8 billion and an operating profit of KRW 117.3 billion. These figures represented a 5% and 7% miss, respectively, compared to market expectations, which could understandably create short-term caution among investors. The full details of these results are available in the company’s regulatory filing (Source: Official Disclosure).

However, the highlight of the announcement was the net profit, which reached KRW 326.3 billion, a notable 3% increase over market estimates. This outperformance in net profit suggests effective cost management, favorable non-operating gains, or other efficiencies that are crucial for understanding the company’s true financial health beyond the headline numbers.

Despite a slight dip in revenue, KCC’s robust net profit and strengthening fundamentals suggest its long-term growth narrative, primarily driven by the high-demand silicon sector, remains firmly intact.

Fundamental Health Check: Growth Drivers vs. Headwinds

Positive Catalysts: The Engines of Future Growth

- •Dominant Silicon Segment: The KCC silicon business is the company’s crown jewel, contributing nearly half of total revenue. Its growth is directly tied to secular trends like the electric vehicle (EV) revolution, where silicones are essential for battery packs, and the rising demand for advanced medical devices in an aging global population. This strategic positioning provides a powerful, long-term tailwind.

- •Rock-Solid Core Businesses: The building materials and paints segments act as a stabilizing force. With a leading market share and trusted brand power, these divisions provide consistent cash flow, balancing the portfolio and mitigating cyclicality in other areas. This stability is a key part of any positive KCC stock analysis.

- •Fortified Financials: KCC has actively improved its balance sheet. The consolidated debt-to-equity ratio has been reduced to a manageable 120.53%, and its cash reserves have swelled to KRW 781.6 billion. This financial fortification provides a crucial buffer against macroeconomic shocks and enables strategic investments. For more on evaluating company financials, see our guide on how to analyze a balance sheet.

Negative Factors & Potential Risks

- •Raw Material Price Volatility: The profitability of the silicon business is sensitive to fluctuations in the prices of key inputs like metal silicon and methanol. Supply chain disruptions or sudden demand spikes could compress margins.

- •Macroeconomic Headwinds: No company is immune to the broader economic environment. As noted by leading financial publications like Bloomberg, factors like global interest rate hikes, currency volatility, and geopolitical tensions can impact everything from overseas sales to raw material procurement costs.

- •Short-Term Investor Sentiment: The miss on revenue and operating profit could weigh on the stock price in the immediate term. It will be crucial to monitor trading activity, especially from foreign investors whose ownership has declined in recent years.

Investment Thesis & Strategic Outlook

Despite the short-term noise from the KCC Corporation earnings miss, the long-term investment thesis remains compelling. The structural growth story of its silicon business is powerful, its financial health is solid, and its core segments provide a stable foundation. While near-term volatility is expected, the company’s long-term value creation potential is significant.

For prospective investors, a phased investment strategy is recommended. Instead of reacting to daily price swings, consider accumulating a position over time, especially during periods of market weakness. Watch for key catalysts, such as updates on the expansion of the high-value-added silicon product portfolio and the company’s guidance for the upcoming quarters, before making significant capital commitments.

Frequently Asked Questions

What were KCC Corporation’s headline Q3 2025 results?

KCC reported sales of KRW 1,622.8 billion and an operating profit of KRW 117.3 billion, both below market estimates. However, net profit was a bright spot at KRW 326.3 billion, exceeding expectations by 3%.

What is KCC Corporation’s main growth engine?

The company’s primary growth driver is its silicon segment, which benefits from the expansion of the EV market and increased demand for medical-grade silicones. This segment accounts for nearly half of the company’s revenue.

How is KCC Corporation’s financial stability?

KCC’s financial health has improved significantly, with a consolidated debt-to-equity ratio of 120.53% and cash reserves of KRW 781.6 billion, enhancing its ability to navigate economic uncertainty.

What is the long-term investment outlook for KCC stock?

The long-term outlook is positive. Despite potential short-term stock price volatility, KCC’s strong position in the growing silicon market, stable core businesses, and solid financial footing support a valid long-term growth narrative.

Leave a Reply