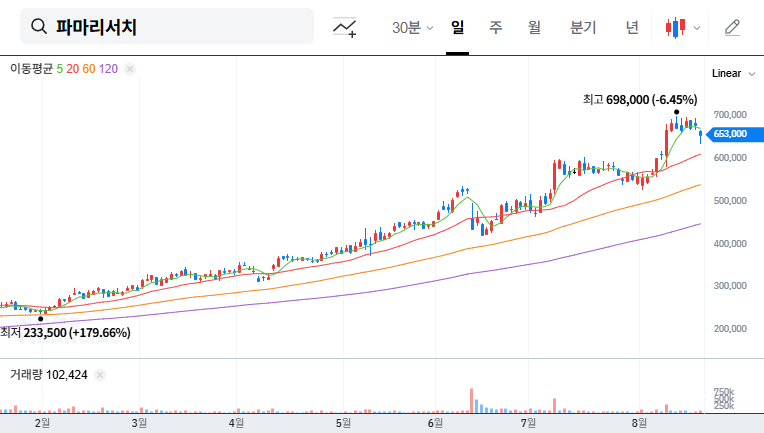

The latest PharmaResearch Q3 2025 earnings report has captured significant attention across the market, and for good reason. With an upcoming Investor Relations (IR) event scheduled for November 17, 2025, investors are keen to understand if the company’s remarkable growth trajectory is sustainable. Spearheaded by the powerhouse medical device ‘Rejuran’ and a rapidly expanding global cosmetics arm, PharmaResearch (KRX: 214450) appears to be firing on all cylinders. This in-depth PharmaResearch stock analysis will dissect the Q3 results, explore the underlying growth drivers, evaluate potential risks, and provide a clear investment outlook.

Deep Dive: PharmaResearch Q3 2025 Earnings Breakdown

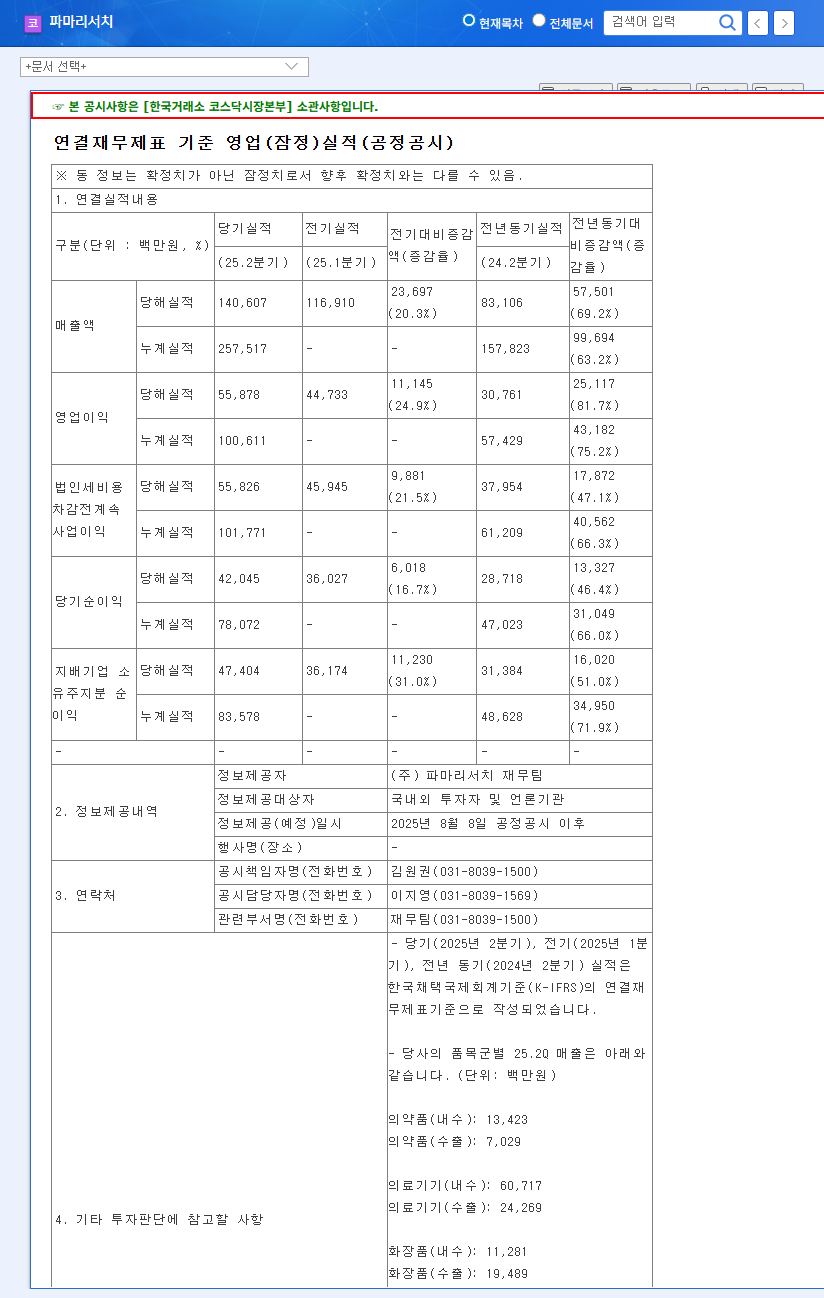

PharmaResearch delivered a stellar financial performance in the third quarter of 2025, demonstrating robust top-line growth and a significant improvement in profitability. The results underscore the company’s strong market position and operational efficiency. The official figures, as detailed in the company’s disclosure, paint a very positive picture. (Official Disclosure: DART Report)

Explosive Growth in Core Divisions

The primary engine of this growth was the Medical Device division, which is the cornerstone of the PharmaResearch investment thesis. Let’s examine the key segments:

- •Medical Device Division: This segment posted an incredible 231,188 million KRW in sales, marking a 58.8% increase year-over-year. This surge was led by exceptional demand for its flagship products, ‘Rejuran’ and ‘ConjuRan’, solidifying their market leadership.

- •Cosmetics Division: Not to be outdone, the cosmetics arm achieved 93,867 million KRW in sales, a healthy 23.9% year-over-year growth. A key factor here was the successful expansion into overseas markets, increasing the proportion of international exports.

- •Pharmaceutical Division: While this division saw a decrease of 15.2%, the company anticipates a rebound following new domestic and international approvals for ‘LienToc inj. 100 units’.

Stunning Profitability and R&D Commitment

PharmaResearch’s consolidated operating profit soared to 162,482 million KRW, with a net profit of 128,925 million KRW. This represents a staggering growth of over 30% year-over-year, showcasing a powerful combination of external growth and disciplined internal cost management. Furthermore, the company continues to invest in its future, dedicating approximately 6.44% of total revenue to R&D for promising new pipelines like IRC_M126 and IRC_D105.

The ‘Why’ Behind the Growth: Market Trends & Product Strength

This robust performance isn’t accidental. It’s the result of strategic positioning within a favorable market and the unique strength of its core products.

PharmaResearch is perfectly positioned to capitalize on two powerful forces: a rapidly growing global anti-aging market and the unique clinical efficacy of its proprietary PN-based products like Rejuran.

The medical device market for aesthetics is booming. As the global population ages and societal emphasis on appearance management increases, the demand for skin boosters and anti-aging treatments is projected to see continued high growth. According to the World Health Organization, the proportion of the world’s population over 60 years will nearly double by 2050, providing a long-term tailwind for this sector. At the heart of this trend is ‘Rejuran’, which utilizes an exclusive regenerative material, PN (Polynucleotide), to establish a dominant position in the skin booster market. To learn more about this sector, see our guide to investing in the aesthetics industry.

Navigating Potential Risks for Investors

Despite the overwhelmingly positive results, prudent investors must not overlook potential risk factors that could impact PharmaResearch’s stock performance.

- •High Financial Debt: The company carries a significant amount of financial debt, including convertible redeemable preferred shares. This requires careful monitoring of interest burdens and overall financial health management, especially in a fluctuating rate environment.

- •Exchange Rate Volatility: With a growing share of international sales, currency fluctuations pose a tangible risk. As of Q3 2025, a 10% change in the exchange rate is estimated to impact net income by approximately 9.24 billion KRW.

- •Interest Rate Sensitivity: Macroeconomic factors, such as the US and European benchmark interest rates, directly affect borrowing costs. Any future rate hikes could increase pressure on the company’s bottom line.

Investor Takeaway & Action Plan

The PharmaResearch Q3 2025 earnings report solidifies the company’s status as a high-growth leader in the aesthetics and medical device space. The explosive growth of Rejuran and the successful overseas expansion of its cosmetics line are set to drive sustained revenue for the foreseeable future. Coupled with consistent R&D investment, the company’s long-term outlook appears bright.

Based on these strong fundamentals, our overall opinion remains a ‘Buy’. The upcoming IR event is a critical catalyst that could re-affirm the company’s value and further boost investor confidence. However, investors should pay close attention to management’s commentary on the key risks. A clear and convincing strategy for managing debt and mitigating currency exposure could significantly influence the stock’s short-term trajectory. Failure to adequately address these concerns could introduce volatility. Ultimately, investment decisions should be based on individual risk tolerance and a thorough review of the IR proceedings.