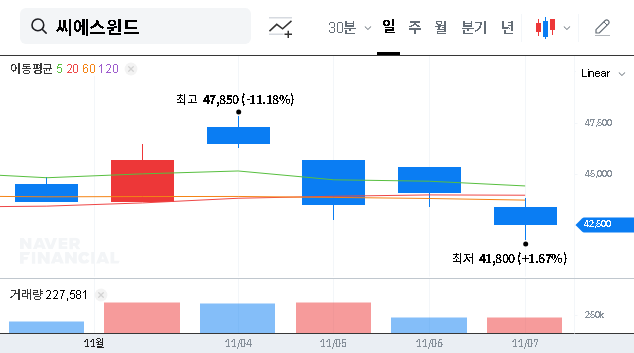

In a significant move that underscores its dominance in the global wind power market, CS Wind Corporation has announced a monumental supply contract with Vestas American Wind Technology. This deal, valued at ₩290.2 billion (approximately $210 million USD), is not just a major revenue driver but a strategic reinforcement of its critical position in the burgeoning US renewable energy sector. For investors, this development signals a pivotal moment, validating the company’s growth trajectory and solidifying its long-term potential.

This comprehensive analysis will delve into the specifics of the Vestas wind tower deal, evaluate CS Wind‘s robust fundamentals, and provide a clear outlook for a potential CS Wind investment. We will explore the company’s record-breaking 2024 performance, its strategic expansions, and the potential risks on the horizon, offering a 360-degree view for informed decision-making.

The Landmark Vestas Wind Tower Deal Explained

CS Wind has secured a contract to supply wind towers to Vestas for the US market. The agreement, valued at a substantial ₩290.2 billion, is set to run for approximately 13 months, from November 2025 to December 2026. This single contract represents a significant 9.4% of the company’s recent annual revenue, highlighting its immediate and impactful contribution to the bottom line. The full details of this agreement were confirmed in an Official Disclosure (Source: DART). Partnering with Vestas, a global leader in turbine manufacturing, not only provides a stable revenue base but also enhances CS Wind’s reputation and deepens its integration into the North American supply chain.

Why This Deal is a Game-Changer for CS Wind Investment

This contract is more than just a large order; it’s a powerful catalyst that reinforces CS Wind‘s core strengths and growth narrative.

1. Cementing Leadership in the US Market

The US is a critical battleground for renewable energy, driven by ambitious climate goals and supportive legislation like the Inflation Reduction Act (IRA). This deal positions CS Wind as a primary beneficiary of this transition. By supplying a key player like Vestas, the company solidifies its market share and becomes an indispensable part of America’s green energy infrastructure. This deepens its competitive moat and increases the likelihood of follow-on orders.

2. Building on Record-Breaking Financial Performance

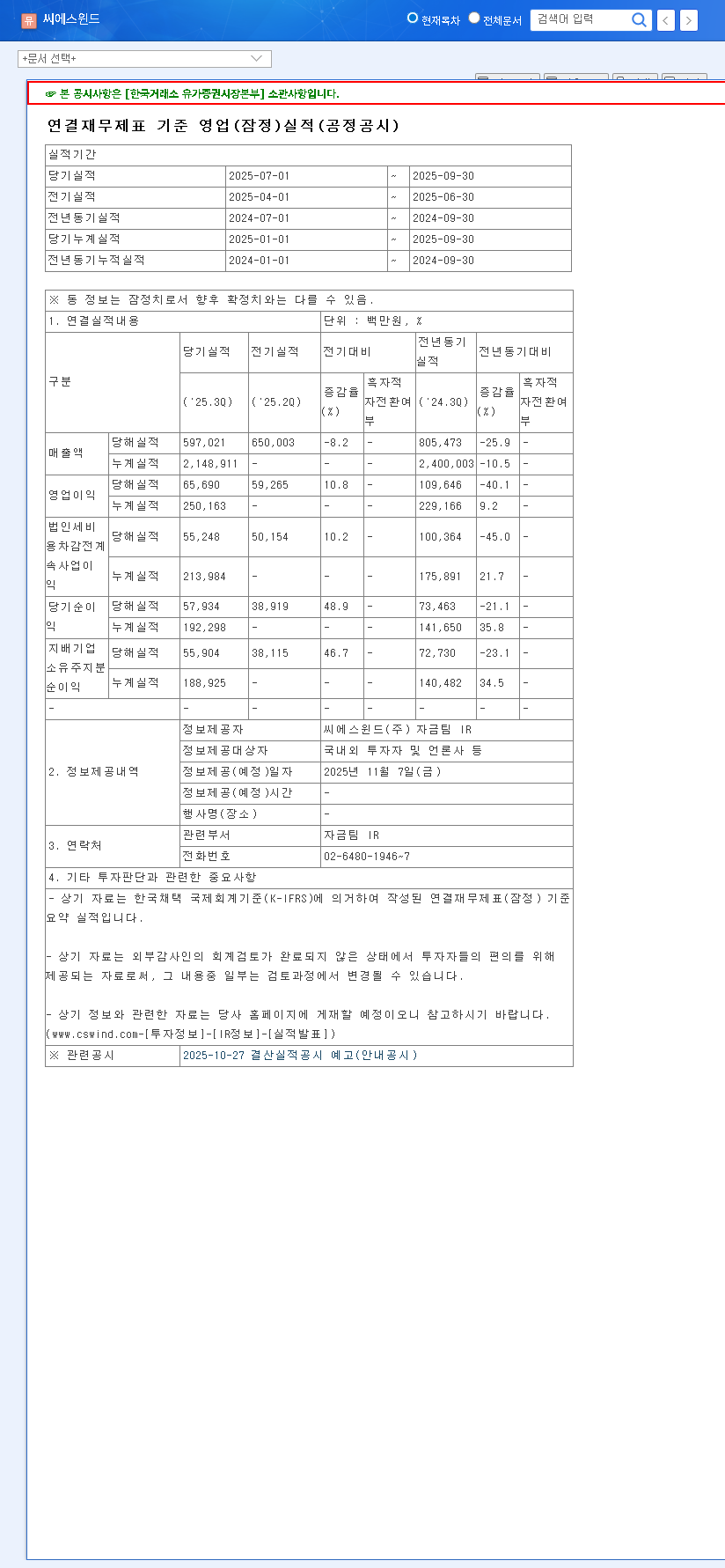

The Vestas contract lands on the heels of a stellar year for CS Wind. In 2024, the company achieved record-high performance with revenues hitting ₩3.07 trillion and an operating profit of ₩255.5 billion. A significant portion of this growth came from the newly acquired offshore wind substructure business, which impressively generated ₩1.13 trillion in its first year. This demonstrates the company’s ability to successfully integrate major acquisitions and capitalize on the high-growth offshore sector, a key area in the global renewable energy market.

3. Strategic Global Expansion

CS Wind is not just focused on the US. The company is actively expanding its global production capacity with significant facility upgrades at its subsidiaries in Vietnam and Portugal. This global footprint allows for optimized logistics, diversified manufacturing, and enhanced competitiveness, enabling it to serve both North American and European markets effectively. This strategy mitigates regional risks and positions the company to capture growth wherever it occurs.

Financial Health and Potential Risk Factors

While the outlook is overwhelmingly positive, a prudent CS Wind investment thesis requires a balanced view of its financial health and potential headwinds.

Financial Health Check

The company’s net debt-to-equity ratio rose to 70.48% at the end of 2024, primarily due to investments in expansion and acquisitions. While this figure requires monitoring, it appears manageable within the context of soaring revenues and profits. Furthermore, a recent decline in steel plate prices—a key raw material—provides a welcome cost tailwind. The company’s effective management of its foreign exchange positions also reduces sensitivity to currency volatility, a crucial capability for a global exporter.

Key Risks to Monitor

- •Raw Material Volatility: Sudden spikes in the price of steel plates could compress profit margins if not managed effectively through hedging or contractual pass-through clauses.

- •Exchange Rate Fluctuations: As the Vestas contract is denominated in USD, significant shifts in the KRW/USD exchange rate could impact the final converted revenue and profitability.

- •Macroeconomic Headwinds: Changes in US energy policy, global interest rate movements, or geopolitical instability could affect project timelines and overall demand in the wind power market. Explore our guide to investing in renewable energy stocks for more on this topic.

Investor Outlook & Final Verdict

The large-scale contract with Vestas is a powerful reaffirmation of CS Wind‘s premier status in the global wind tower industry. This, combined with its record financial performance and the successful pivot into the high-margin offshore substructure market, paints a compelling picture of a company firing on all cylinders.

Given the structural, long-term growth of the global wind power market, CS Wind is exceptionally well-positioned to deliver sustained growth. We maintain a positive long-term investment opinion, viewing any short-term market volatility as a potential buying opportunity for this best-in-class renewable energy stock.

Investors should continue to monitor new contract signings, the ongoing impact of the US IRA, and trends in raw material costs to stay ahead of the curve.

Leave a Reply