This comprehensive SGC E&C earnings analysis provides a deep dive into the company’s provisional third-quarter 2025 results, which have sent mixed signals to the market. While the year-over-year improvement offers a glimmer of hope, it’s crucial to look beyond the headline numbers. Significant underlying challenges, including valuation pressures and macroeconomic headwinds, demand a cautious approach from investors.

What is the true financial state of SGC E&C, and what story do the numbers tell about its future? This report examines the company’s fundamentals, recent workforce adjustments, and the broader economic landscape to formulate a clear-eyed investment strategy for the current environment. Let’s explore the critical data needed to accurately assess the SGC E&C stock outlook.

Unpacking the SGC E&C Q3 2025 Earnings Report

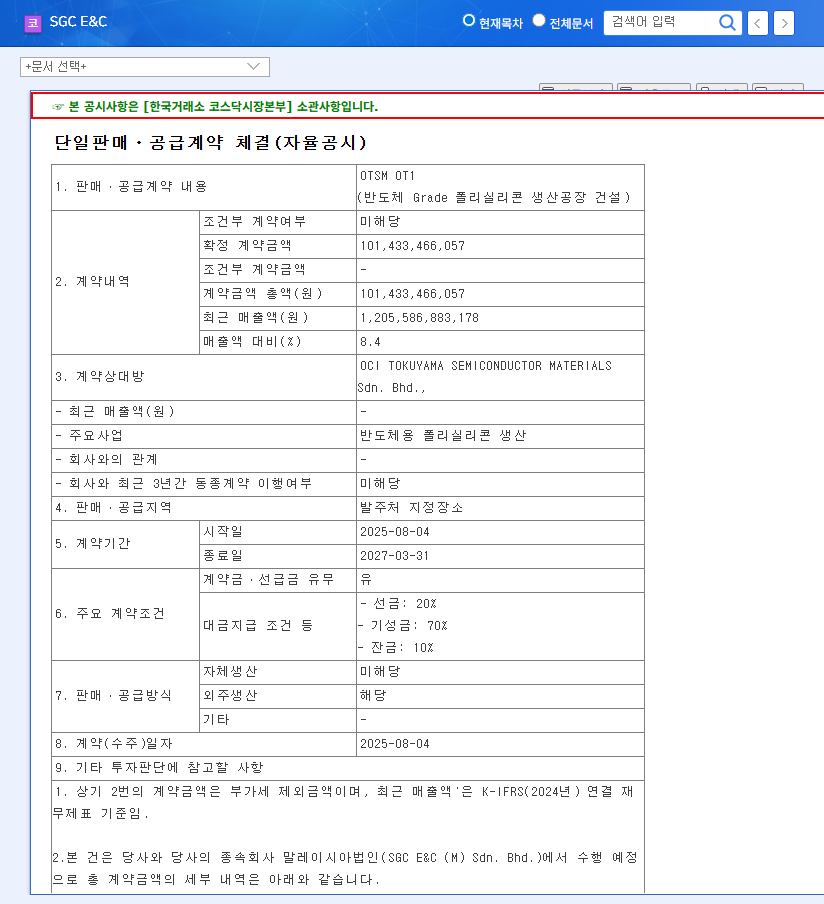

On November 12, 2025, SGC E&C Co., Ltd. released its provisional consolidated financial results for the third quarter. The official disclosure can be viewed directly from the source: Official Disclosure (DART).

Q3 2025 Provisional Results:

– Sales: 325.8 billion KRW

– Operating Profit: 11.6 billion KRW

While the operating profit shows a marked improvement from the 1.1 billion KRW reported in Q3 2024, this positive momentum is overshadowed by the massive losses incurred in the fourth quarter of 2024. The market’s reaction is likely to remain muted, as this single quarter of recovery is insufficient to erase concerns about full-year performance and the sky-high Price-to-Earnings (PER) ratio.

A Deep Dive into SGC E&C’s Financial Health

To understand the context behind the latest numbers, we must analyze the company’s recent performance trends and key financial indicators. The data reveals a story of volatility and a challenging road to recovery.

Quarterly Performance Trends

- •Q3 2025: Sales 325.8B KRW, Operating Profit 11.6B KRW

- •Q2 2025: Sales 336.0B KRW, Operating Profit 14.9B KRW

- •Q4 2024: Sales 378.3B KRW, Net Income -31.3B KRW

Key Financial Observations

- •Earnings Volatility: A pattern of recovery in 2025 is evident, but it follows a period of significant financial distress in late 2024. The sustainability of this recovery is the key question for any SGC E&C investment thesis.

- •Profitability Under Pressure: Key metrics like operating profit margin and Return on Equity (ROE) were severely damaged in 2024. While improving, they remain far below historical levels, indicating ongoing efficiency challenges.

- •Improved Financial Soundness: On a positive note, the debt-to-equity ratio has steadily declined, suggesting successful efforts to deleverage and strengthen the balance sheet.

- •Extreme Valuation: The estimated PER for 2025 stands at an exceptionally high 1,565.04x. This indicates that the current stock price is far ahead of its earnings, posing a significant risk of correction. For more on valuation metrics, investors can review resources from authoritative sites like Bloomberg.

Workforce and Macroeconomic Headwinds

Strategic Workforce Adjustments

Data from June 2025 shows a net decrease of 44 employees, primarily concentrated in the construction division. This could signal a strategic pivot or a response to a weaker order book in that sector. Positively, an increase in average service length and salary suggests the company is successfully retaining its experienced, high-value personnel, which is crucial for long-term stability.

Challenging Macro Environment

SGC E&C does not operate in a vacuum. Several external factors create significant headwinds:

- •High Exchange Rate: The strong USD against the KRW (around 1,466) increases the cost of imported raw materials and equipment, directly squeezing profit margins.

- •Interest Rate Uncertainty: While rates have shown a downward trend, any future freeze or hike could elevate borrowing costs and impact the financing of large-scale projects.

Investment Thesis: A Cautious Outlook

Considering the lingering financial burden from 2024, uncertainty around Q4 2025 performance, and extreme valuation pressure, a conservative and cautious approach is warranted for SGC E&C stock at this time. The positive earnings trend is a good sign, but it is not yet strong enough to justify the high stock price.

Action Plan for Astute Investors

Before committing capital, investors should seek clarity on the following points. For those new to this type of analysis, our guide on how to analyze construction company stocks provides a helpful framework.

- •Confirm the final, audited Q4 2025 earnings and management’s strategy for sustained profitability.

- •Monitor the order pipeline for the construction and plant divisions to gauge future revenue streams.

- •Assess the performance of new business ventures (e.g., logistics) as potential growth drivers.

- •Ensure the company continues to manage its debt and maintain healthy cash flow.

Frequently Asked Questions (FAQ)

What were SGC E&C’s provisional earnings for Q3 2025?

For the third quarter of 2025, SGC E&C Co., Ltd. reported consolidated sales of 325.8 billion KRW and an operating profit of 11.6 billion KRW, which is an improvement over the same period in the previous year.

How is SGC E&C’s current financial health?

The company’s financial soundness has improved, as evidenced by a consistently decreasing debt-to-equity ratio. However, concerns about overall profitability remain due to significant losses recorded in 2024.

What is the recommended investment approach for SGC E&C stock now?

Given the high valuation, past losses, and macroeconomic uncertainties, a cautious or conservative approach is recommended. Investors should wait for more clarity on sustained earnings recovery before making significant investment decisions.

Leave a Reply