The recent court ruling involving Seobu T&D (KRX: 006730) and Daewoo E&C has sent ripples through the investment community. While the headline figure of a ₩16.5 billion payment seems manageable compared to the initial claim, a deeper financial analysis reveals that this verdict is merely a symptom of more significant, underlying challenges facing the company. This comprehensive report cuts through the noise to examine the true state of Seobu T&D’s financial health, the verdict’s real implications, and the critical factors investors must monitor moving forward.

Deconstructing the Daewoo E&C Lawsuit Verdict

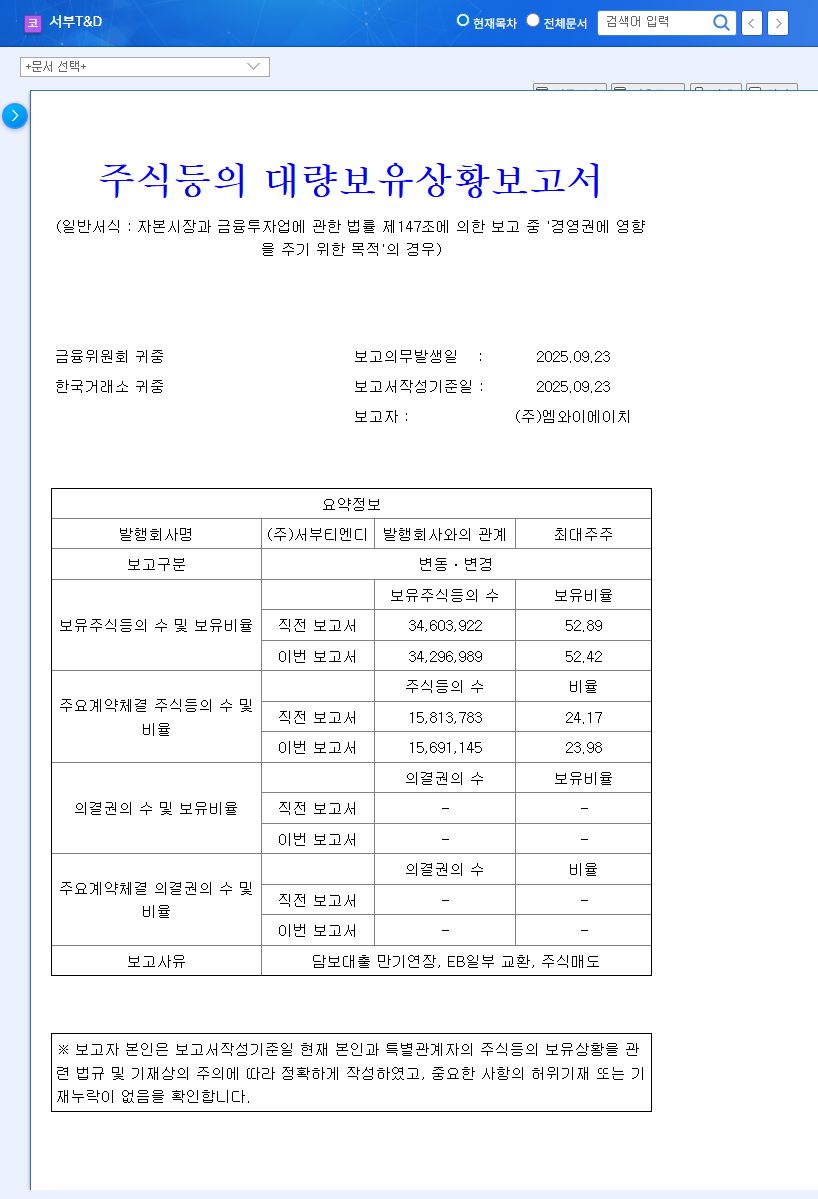

Seobu T&D has been ordered to pay ₩16.5 billion in a lawsuit over hotel construction payments filed by Daewoo E&C. This figure is substantially lower than the initial ₩44.5 billion claim, which has led to some optimistic interpretations. This verdict stems from case 2018gahap552450, as detailed in the Official Disclosure on DART. Let’s break down the key financial components:

- •Final Payment: An obligation of ₩16,522,114,984 plus related interest to be paid to Daewoo E&C. This represents approximately 1.33% of the company’s equity.

- •Debt Exemption Profit: The nearly ₩28 billion difference between the initial claim and the final verdict is expected to be recorded as a one-time ‘debt exemption profit’. This is an accounting gain, not a cash inflow, but it will positively impact the net income on paper for the reporting period.

- •Litigation Costs: Seobu T&D is responsible for 65% of the litigation costs, adding another layer of cash outflow.

While the verdict is a sigh of relief compared to the worst-case scenario, investors must not mistake a one-time accounting gain for a fundamental improvement in business operations. The core challenges for Seobu T&D remain firmly in place.

The True Financial Picture: Beyond the Verdict

The Seobu T&D lawsuit is a critical event, but it’s a sideshow to the main story: the company’s deteriorating financial health and operational struggles. A prudent Seobu T&D financial analysis must look deeper.

Challenge 1: Ailing Core Business

The company’s performance is heavily tied to its tourism hotel business, which has been severely underperforming. As of the first half of 2025, revenue from this segment plummeted by 41% year-on-year. This is not just a company-specific issue but reflects broader challenges in the post-pandemic tourism sector. With declining revenue and rising administrative costs, Seobu T&D reported a consolidated net loss of ₩4.27 billion, a stark reversal into deficit. Other segments, such as shopping malls and logistics, have also failed to offset this decline.

Challenge 2: Alarming Debt Levels

Perhaps the most significant red flag is the company’s high financial leverage. The debt ratio has climbed to a concerning 142.33%. This level of debt makes the company vulnerable to interest rate fluctuations and economic downturns. The ₩16.5 billion lawsuit payment, while manageable, will further strain a balance sheet that is already stretched thin. This could negatively impact Seobu T&D’s credit rating, making future fundraising more expensive and difficult. For more information on assessing company debt, review our guide to financial ratios.

Investor Playbook for Seobu T&D (006730)

Given the complex situation, investors should adopt a cautious and long-term perspective. The resolution of the Daewoo E&C lawsuit removes a major uncertainty, but it does not fix the underlying business.

Key Monitoring Points for a Turnaround:

- •Tourism Business Revival: Watch for a tangible recovery in hotel occupancy rates and revenue. Is management implementing a clear strategy to adapt to new travel trends?

- •Financial Deleveraging Plan: Look for a credible plan to reduce the 142.33% debt ratio. This could include asset sales, cost-cutting initiatives, or strategic capital raising.

- •Profitability Improvements: Monitor operating margins and the company’s ability to return to net profitability without relying on one-off gains like the debt exemption profit.

Based on this analysis, the current investment recommendation is a Hold or Cautious Buy. The risk profile remains elevated until there is clear evidence of a sustainable recovery in its core operations and a significant improvement in its financial structure. Investors should proceed with prudence and diligence.

Leave a Reply