The current investment landscape for DAECHANG SOLUTION CO.,LTD. (096350) is fraught with significant challenges, creating a perfect storm for potential and current investors. The company is grappling with a severe downturn in financial performance, compounded by a significant stock sell-off from a major institutional shareholder. This comprehensive stock analysis provides a deep dive into the deteriorating fundamentals, the market implications of the recent divestment, and a forward-looking perspective on the 096350 stock outlook.

For those considering an investment or reassessing a current position in DAECHANG SOLUTION, understanding these interconnected issues is paramount. We will dissect the numbers, analyze the market signals, and offer a clear, objective viewpoint on what lies ahead.

The Double Blow: Shareholder Sell-Off & Financial Decline

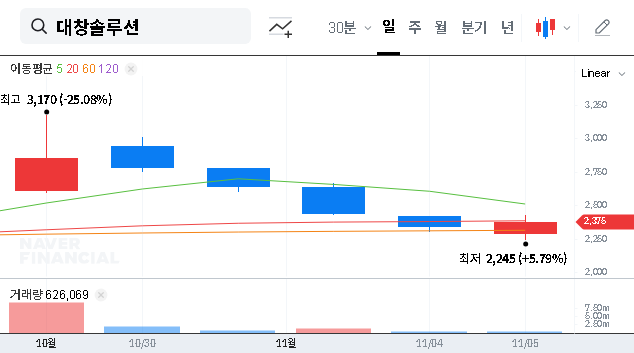

Two major events have recently cast a dark shadow over DAECHANG SOLUTION 096350, creating significant downward pressure on its stock price and raising alarms within the investment community.

1. The Major Shareholder Divestment: A Vote of No Confidence?

‘K&T-Daeshin New Technology Investment Association No. 3’, an institutional investor, recently sold a substantial block of shares, reducing its stake from 5.09% to 3.66%. While a single transaction is not always a definitive signal, the context here is crucial. The fund’s stated purpose was “simple investment,” meaning its decision to sell can be interpreted as a purely financial one, likely based on a negative assessment of the company’s future value. This action, officially documented in the company’s disclosure (Source: DART Report), sends a powerful bearish signal to the broader market, potentially triggering further selling from retail investors who follow institutional moves.

2. Severe Performance Collapse in H1 2025

The shareholder sell-off did not happen in a vacuum. It coincides with a catastrophic decline in the company’s performance. In the first half of 2025, DAECHANG SOLUTION’s financial results were deeply concerning:

- •Revenue Plunge: Sales plummeted by nearly 50% year-on-year to KRW 24.9 billion. This isn’t a minor dip; it’s a fundamental collapse in demand across its core business segments.

- •Operating Loss: The company swung from a profit to an operating loss of KRW 1.48 billion, indicating that its core operations are no longer profitable.

- •Expanding Net Loss: The net income deficit also widened, signaling further erosion of shareholder value.

Deep Dive: DAECHANG SOLUTION 096350 Financial Health Under Scrutiny

A closer look at the balance sheet reveals a company under immense financial strain. The poor income statement is not an isolated issue but a symptom of deeper, structural problems. To fully grasp the Daechang financial analysis, it’s essential to understand these red flags.

With a high debt ratio, rising inventory, and a massive accumulated deficit, the company’s financial foundation appears fragile, making it highly vulnerable to macroeconomic shocks like interest rate hikes.

- •Extremely High Debt Ratio (295.38%): This figure indicates that the company has nearly three times more debt than equity. Such high leverage magnifies risk, increases interest expense, and limits the company’s ability to invest in future growth or weather further downturns.

- •Bloating Inventory (+47.9%): A massive increase in inventory while sales are collapsing is a classic warning sign. It suggests products aren’t selling, leading to inefficient capital allocation, potential write-downs, and cash flow problems.

- •Accumulated Deficit (KRW 53.7 billion): This represents the sum of all past losses, which have completely eroded the company’s retained earnings. It’s a severe threat to long-term financial stability.

The revenue decline is widespread, affecting shipbuilding materials, power generation facilities, and industrial machinery. This reflects both company-specific issues and broader macroeconomic headwinds, such as the global shipbuilding slowdown discussed by industry experts at authoritative sources like Reuters.

Future Outlook: Can New Ventures Save the Day?

Despite the grim picture, there are a few potential bright spots. The company holds an order backlog of KRW 55.9 billion, which provides some revenue visibility. However, this is likely insufficient to reverse the current negative trajectory on its own. The real long-term hope lies in its strategic pivot towards new growth industries.

Investments in offshore wind power and hydrogen energy represent potential game-changers. These are high-growth sectors aligned with global energy transition trends. However, these are long-term plays that require significant capital and time to generate tangible results. Investors should view them as speculative bets on a future turnaround rather than a short-term solution to the current crisis. For more on this, you can read our guide on how to analyze growth stocks.

Conclusion: Extreme Caution Warranted for DAECHANG SOLUTION

The DAECHANG SOLUTION 096350 stock analysis reveals a company at a critical crossroads. The combination of a major shareholder sell-off and a severe fundamental deterioration presents a high-risk investment profile. Downward pressure on the stock is likely to persist until there is clear, undeniable evidence of a turnaround.

Key factors to monitor for any sign of recovery include:

- •A return to operating profitability in upcoming quarterly reports.

- •Concrete revenue contributions from its new offshore wind or hydrogen businesses.

- •A strategic plan to address the massive debt load and improve the financial structure.

Until these milestones are achieved, an approach of extreme caution is the most prudent investment strategy for DAECHANG SOLUTION CO.,LTD.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. All investment decisions should be made based on your own research and judgment.

Leave a Reply