The ongoing CAPRO delisting review has placed investors in CAPRO CORPORATION (006380) on high alert. With a final decision from the Korea Exchange expected by November 27, 2025, the company stands at a critical crossroads. This comprehensive analysis will dissect the factors leading to this review, evaluate the company’s dire financial state, and provide a clear outlook on the potential scenarios for shareholders. For anyone holding or considering an investment in CAPRO, understanding these details is not just important—it’s essential for capital preservation.

With severe financial deterioration and the looming threat of delisting, CAPRO CORPORATION represents one of the highest-risk investments on the market today. Investors must exercise extreme caution.

The Catalyst: Why a CAPRO Delisting Review Was Initiated

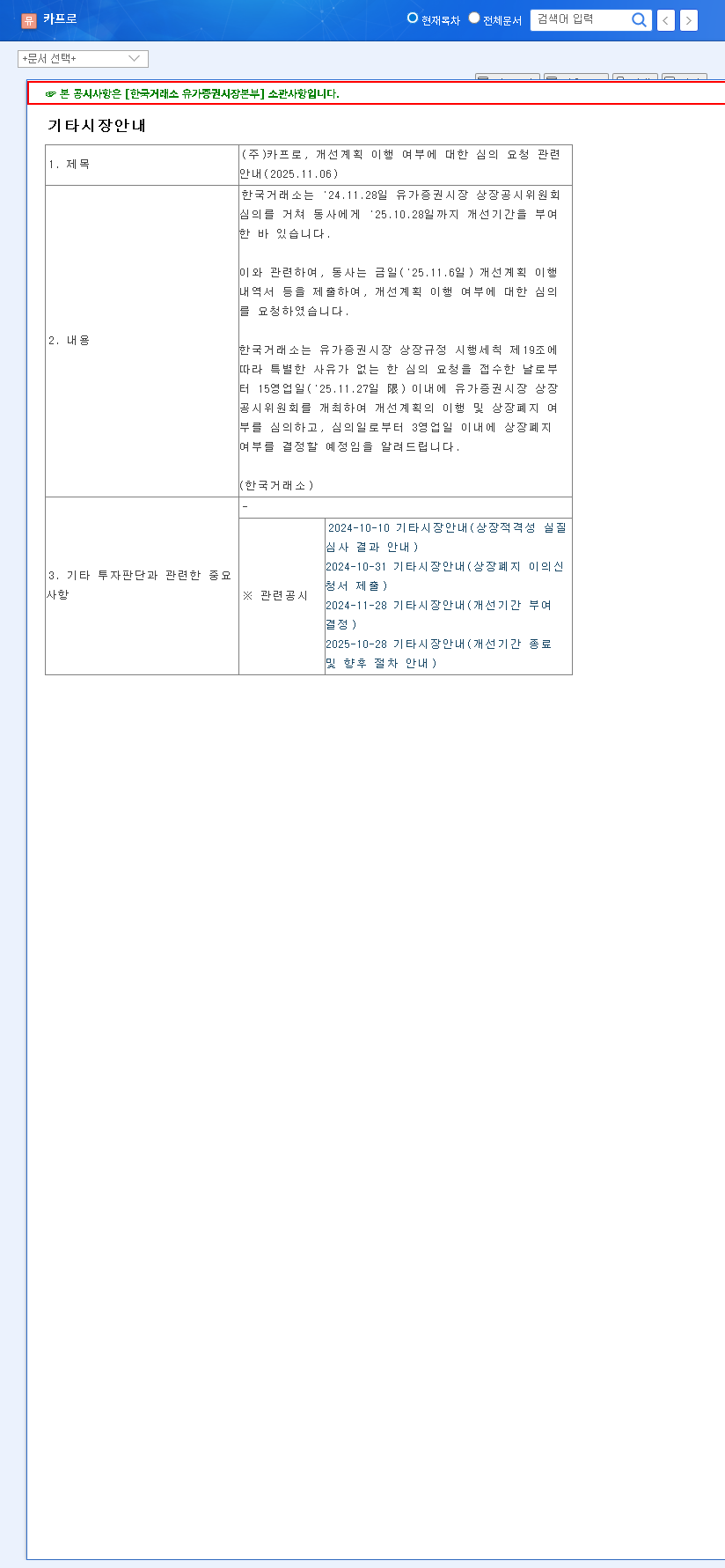

The situation escalated on November 6, 2025, when CAPRO CORPORATION formally submitted its improvement plan performance report to the Korea Exchange. This action triggered the official review process to determine if the company has sufficiently addressed the issues that led to its probationary status, which was granted back on November 28, 2024. The exchange now has until November 27, 2025, to convene its Listing Disclosure Committee and render a final verdict. The outcome of this CAPRO delisting review will decide whether the company’s stock continues to trade or is removed from the market entirely. You can view the Official Disclosure on the DART system for primary source information.

Financial Collapse: A Look at the Numbers

The primary driver behind the delisting concern is CAPRO’s catastrophic financial performance. The numbers paint a grim picture of a company struggling for survival. A deep dive into its financial statements reveals multiple red flags that cannot be ignored.

Plummeting Revenue and Deepening Losses

The company’s top line has been in freefall. Revenue collapsed from KRW 1,147.7 billion in 2022 to just KRW 627.2 billion in 2024, with projections for 2025 showing a further slide to KRW 469.4 billion. More alarming is the shift from an operating profit of KRW 175.8 billion in 2022 to a projected operating loss of KRW -30.8 billion in 2025. This indicates a fundamental breakdown in the company’s core business profitability, a key metric for any sustainable enterprise. For more context on evaluating company health, you can learn about analyzing financial statements in our internal guide.

Worsening Balance Sheet and Debt Burden

CAPRO’s financial foundation is eroding. The debt-to-equity ratio, a critical measure of financial leverage, has surged from 92.27% in 2022 to a worrying 114.65% in 2024. This signals that the company is increasingly reliant on borrowing to stay afloat, a risky strategy in a high-interest-rate environment. The continuous decline in retained earnings further highlights a lack of internal financial capacity to weather this storm.

A Desperate Pivot: Business Restructuring Efforts

In a bid for survival, CAPRO is undertaking a radical business transformation. The company is shuttering its legacy core operations in caprolactam and ammonium sulfate fertilizer. It is attempting to pivot to new, potentially high-growth sectors:

- •Hydrogen: Tapping into the global push for clean energy.

- •Sulfuric Acid: A key industrial chemical with diverse applications.

- •Scrap Metal: A play on the circular economy and raw material markets.

While ambitious, the success of these new ventures is highly uncertain and will require significant capital investment—something the company desperately lacks. Efforts to attract new investment and change the largest shareholder are underway, but the profitability and timeline for these new businesses remain speculative at best.

Impact Analysis: Potential Outcomes for Investors

Investors face two starkly different futures depending on the Korea Exchange’s decision. The uncertainty leading up to the announcement will fuel extreme volatility.

Scenario 1: Listing is Maintained

If CAPRO passes the review, a significant relief rally is possible. Investor focus would shift to the viability of its new hydrogen and sulfuric acid ventures. However, the path to recovery would be long and fraught with challenges. The company’s heavy debt load and ongoing losses would continue to weigh on the stock price. Sustainable recovery would depend entirely on the tangible, profitable success of its business pivot, not just on promises.

Scenario 2: Company is Delisted

A delisting decision would be catastrophic for current shareholders. Trading of stock 006380 would be immediately suspended, trapping investors and making it nearly impossible to liquidate their positions. Shareholder value would likely be wiped out, with investors facing the real possibility of a total loss of their investment capital. The company’s future would become uncertain, likely leading to restructuring or bankruptcy proceedings. For a broader understanding of market risks, authoritative sources like Bloomberg provide extensive financial analysis.

Conclusion: A Strong ‘Highly Not Recommended’ Rating

Given the overwhelming evidence of financial instability, the uncertainty of its business transition, and the existential threat posed by the CAPRO delisting review, investing in CAPRO CORPORATION at this moment involves an unacceptable level of risk. The potential for a complete loss of principal far outweighs any speculative upside.

Our investment opinion is unequivocally Highly Not Recommended. We strongly advise existing shareholders to re-evaluate their positions and potential investors to avoid this stock until there is concrete, undeniable evidence of a sustainable turnaround. Prudent decision-making is paramount when facing such a high-stakes event.

Leave a Reply