The latest COSMECCA KOREA Q3 2025 earnings report has sent ripples through the investment community, showcasing results that didn’t just meet but dramatically exceeded market expectations. As a powerhouse in the cosmetics Original Design Manufacturer (ODM) and Original Equipment Manufacturer (OEM) sector, the company’s performance offers a crucial barometer for the health of the K-beauty industry and provides a compelling case study for savvy investors. This deep-dive analysis unpacks the preliminary numbers, explores the fundamental drivers behind this explosive growth, and outlines a strategic outlook for what comes next.

With operating profits soaring 36% above estimates, COSMECCA KOREA has demonstrated exceptional operational leverage and market adaptability, signaling a new phase of robust profitability.

Deconstructing the Q3 2025 Earnings Beat

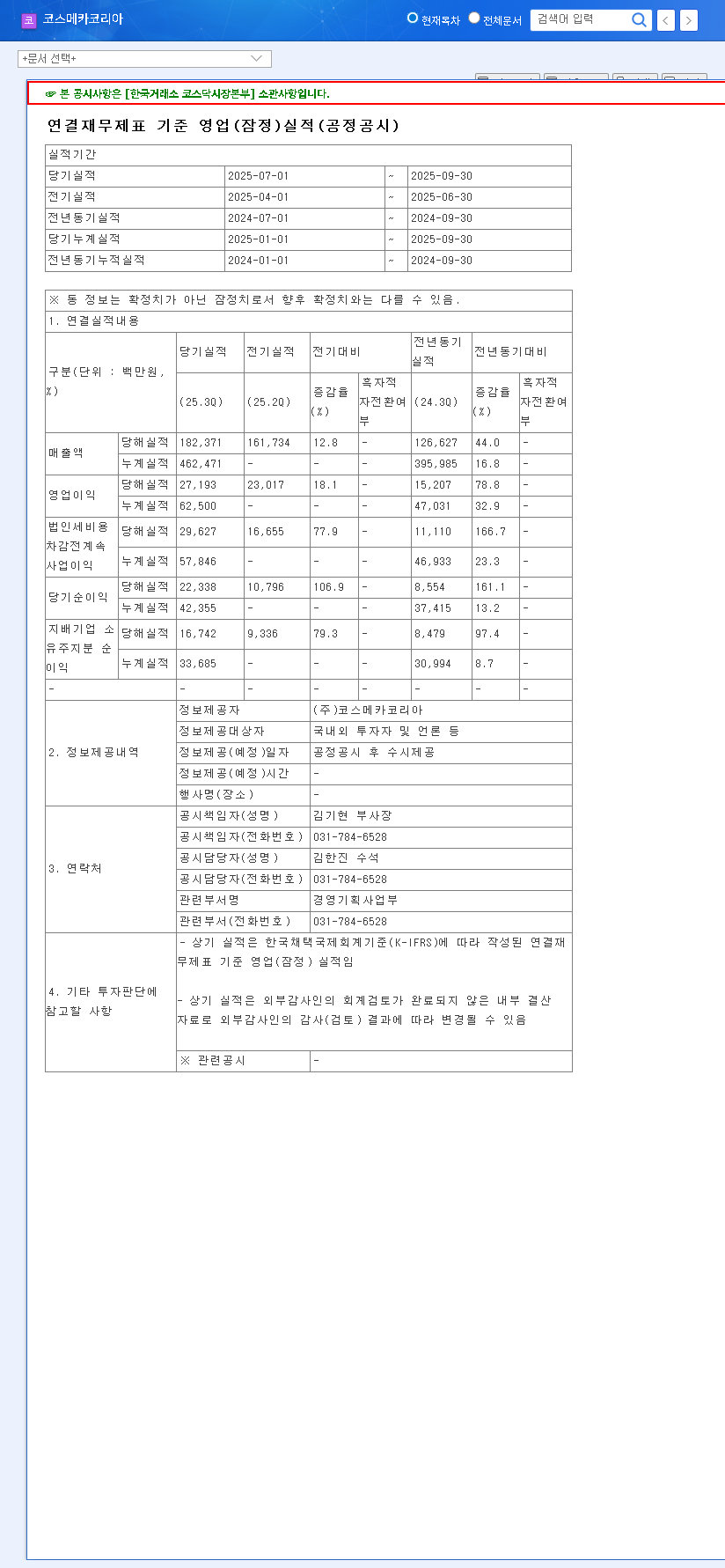

On November 6, 2024, COSMECCA KOREA released its preliminary Q3 results, which can be viewed in the Official Disclosure (DART Report). The figures paint a clear picture of a company firing on all cylinders. The sheer scale of the outperformance against consensus estimates is the key story here, highlighting a significant disconnect between market perception and operational reality.

The Numbers at a Glance:

- •Revenue: Reached KRW 182.4 billion, a staggering 22.0% above the KRW 149.7 billion estimate. This points to surging demand and successful client acquisition.

- •Operating Profit: Hit KRW 27.2 billion, trouncing the KRW 20.0 billion forecast by 36.0%. This significant margin beat indicates powerful improvements in production efficiency and cost control.

- •Net Profit: Came in at KRW 16.7 billion, slightly ahead of the KRW 16.1 billion estimate by 3.7%, solidifying the bottom-line strength.

This performance confirms that the recovery momentum first seen in Q1 2025 has not only been sustained but has accelerated dramatically. The successful turnaround from the challenges of late 2022 is now complete, replaced by a new era of growth.

Core Strengths & Strategic Wins Fueling Growth

This blowout quarter wasn’t a fluke. It’s the result of a multi-pronged strategy focused on innovation, market alignment, and global expansion. A detailed COSMECCA KOREA stock analysis reveals several key pillars supporting this success.

1. Riding the Wave of Modern Cosmetic Trends

COSMECCA KOREA has expertly positioned itself to capitalize on the biggest trends in the beauty industry. Their ‘OGM (Original Global Standard)’ service model is a comprehensive solution for brands, especially the rapidly growing segment of indie brands. By investing nearly 5% of revenue into R&D, they are leading in high-demand areas like:

- •Clean Beauty: Formulations that prioritize safe, non-toxic, and sustainable ingredients.

- •Cosmeceuticals: Products that bridge the gap between cosmetics and pharmaceuticals, offering tangible skin benefits backed by science.

2. Strategic Global Expansion via Englewood Lab

The acquisition of US-based Englewood Lab is a cornerstone of COSMECCA’s long-term strategy. This move provides a critical production base in North America, one of the world’s largest beauty markets. It allows the company to better serve its global clients, reduce logistical complexities, and tap directly into US market trends. While this move increased short-term debt, its strategic value as a long-term growth engine cannot be overstated.

Investor Outlook: Balancing Opportunity and Risk

While the COSMECCA KOREA Q3 2025 earnings are overwhelmingly positive, a prudent investor must consider the full picture. The macroeconomic environment presents both tailwinds and headwinds. For a more detailed look at market dynamics, you can explore insights on the global cosmetics market growth from authoritative sources like Forbes.

Potential Headwinds to Monitor:

The primary risk factors revolve around financial management in a volatile global economy:

- •Interest Rate Pressure: Elevated interest rates globally increase the cost of servicing debt, which rose to a debt ratio of 99.05% following the Englewood Lab acquisition.

- •Currency Fluctuations: As a global exporter and importer of raw materials, volatility in KRW/USD and KRW/EUR exchange rates can impact margins.

- •One-Off Costs: Integration costs related to acquisitions could present short-term, non-recurring expenses that affect quarterly profit statements.

Conclusion: A Compelling “BUY” for the Long Term

The outstanding Q3 2025 results serve as powerful validation of COSMECCA KOREA’s strategy. The company has proven its ability to innovate, adapt, and execute at a high level. The impressive cosmetics ODM growth trajectory, combined with its expanding global footprint, establishes a strong foundation for sustained future success.

While investors should remain vigilant about the financial and macroeconomic risks, the mid-to-long-term growth potential is undeniable. The company is perfectly positioned at the intersection of K-beauty’s global appeal and the rise of agile indie brands. Therefore, from a long-term investment perspective, the outlook remains a confident “BUY”. For more investment ideas in this space, check out our guide on Top K-Beauty Stocks to Watch.

Leave a Reply