The latest InBody Co., Ltd. earnings report for Q3 2025 presents a complex scenario for investors. The global leader in body composition analysis delivered strong revenue that surpassed market expectations, a testament to its growing global footprint. However, a simultaneous miss on operating profit has introduced a note of caution, leaving many to wonder about the future trajectory of InBody stock. Is this a temporary hurdle in a long-term growth story, or does it signal underlying challenges that warrant a closer look?

This comprehensive InBody earnings analysis will dissect the preliminary Q3 2025 figures, evaluate the company’s fundamental strengths and weaknesses, and provide a clear outlook on what these results mean for your investment strategy. We will explore the factors driving both the revenue growth and the profitability pressures to provide a balanced view.

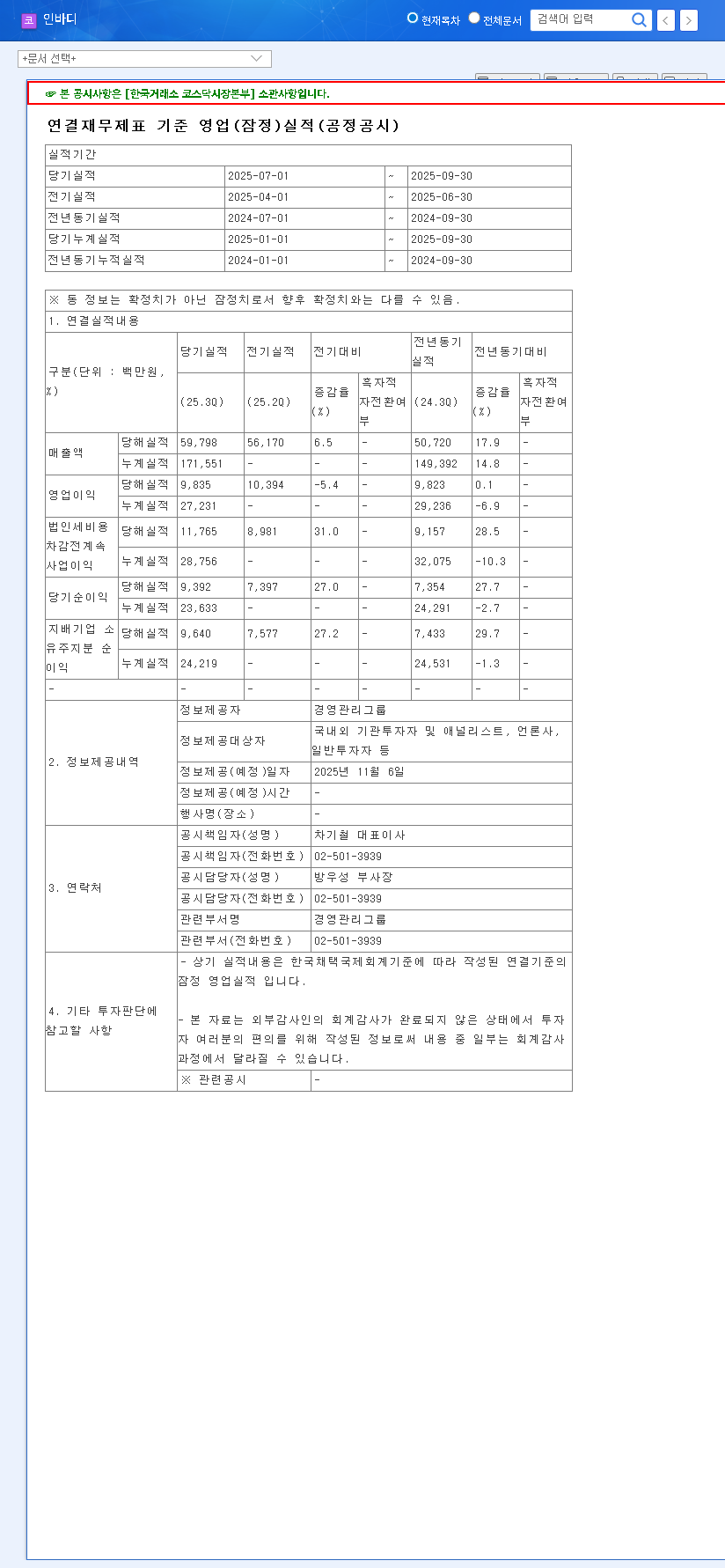

InBody Q3 2025 Earnings: The Official Numbers

On November 6, 2025, InBody Co., Ltd. (041830) released its preliminary consolidated earnings for the third quarter. The official disclosure, available via the DART system, provides the foundational data for our analysis (Source). Here are the key metrics compared to market consensus:

- •Revenue: KRW 59.8 billion, a 5% beat against the expected KRW 57.1 billion.

- •Operating Profit: KRW 9.8 billion, a slight miss compared to the forecasted KRW 9.9 billion.

- •Net Profit: KRW 9.6 billion (no consensus estimate was available for comparison).

The strong revenue performance signals continued, robust demand for InBody’s products worldwide. However, the operating profit miss, while minor, is the focal point for investors as it raises questions about cost control and margin pressure.

Fundamental Analysis: The Pillars and Cracks in InBody’s Foundation

To understand the 041830 earnings report fully, we must look beyond a single quarter and analyze the company’s underlying fundamentals, drawing from its H1 2025 performance and long-term trends.

Positive Drivers: Why InBody Remains a Market Leader

- •Global Demand & Dominance: With over 82% of sales originating overseas, InBody has successfully cemented itself as a global standard. This geographic diversification provides a buffer against regional economic downturns.

- •Financial Fortress: A remarkably low debt-to-equity ratio of just 11.56% gives the company immense financial stability and flexibility to navigate challenges or seize opportunities.

- •Innovation Engine: A consistent R&D investment of nearly 7.7% of revenue fuels its technological edge in the competitive body composition analysis market, keeping it ahead of competitors.

- •Expanding Horizons: Strategic diversification into home-use devices opens up a vast new consumer market, complementing its traditional stronghold in professional settings like gyms and hospitals.

Headwinds & Risk Factors to Monitor

The Q3 profit miss was not an isolated event. It magnifies concerns that were already present in the first half of the year.

“While top-line growth is impressive, the market is now shifting its focus to profitability. The key question for InBody is whether they can translate strong sales into stronger earnings amidst rising costs.”

- •Profitability Squeeze: The primary concern is eroding profitability. Rising selling, general, and administrative (SG&A) expenses and a higher cost of goods sold are compressing margins. Investors need to see a clear strategy to manage these costs.

- •Inventory Management: A low inventory turnover ratio (1.3x) suggests that products are sitting on shelves for too long. This ties up capital, increases holding costs, and poses a risk if demand patterns shift.

- •Macroeconomic Pressures: As a global company, InBody is highly exposed to currency fluctuations and rising interest rates. A strong Korean Won or continued rate hikes globally could negatively impact future InBody Co., Ltd. earnings. For more on this, see analysis from authoritative financial news sources.

Investment Outlook: ‘Hold’ with Cautious Optimism

Considering the conflicting data points, a ‘Hold’ recommendation for InBody stock is prudent. The company’s strong revenue growth and market leadership are undeniable positives. However, the persistent profitability challenges cannot be ignored and are likely to cause short-term stock price volatility.

Key Points for Investors to Watch

The path forward for InBody stock will be determined by the company’s ability to address its current challenges. Keep a close eye on the following in upcoming reports:

- •Margin Improvement: Look for specific commentary and results showing improved control over SG&A and COGS in the Q4 and full-year 2025 earnings announcements.

- •Inventory Efficiency: Any improvement in the inventory turnover ratio will be a strong positive signal that management is effectively optimizing its supply chain.

- •Regional Sales Performance: Pay attention to the breakdown of sales across key markets like the US, Europe, and Asia to ensure growth drivers remain intact.

In conclusion, while the Q3 2025 InBody Co., Ltd. earnings report was mixed, the company’s long-term growth story remains plausible. The immediate priority must be a tangible improvement in profitability to restore full investor confidence.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. All investment decisions should be made based on your own research and risk tolerance.

Leave a Reply