This comprehensive CELL BIOTECH Q3 2025 earnings analysis provides investors with a critical look into the company’s latest performance. As a powerhouse in the probiotics market and a rising innovator in biotechnology with its development of new oncology drugs, CELL BIOTECH’s quarterly reports are a key indicator of its trajectory. We will dissect the financials, evaluate the strength of its core business, and project the potential of its future growth drivers.

Is the company’s recent performance a sign of sustained momentum, or are there underlying challenges investors should note? Let’s explore the data and what it means for the future of CELL BIOTECH.

CELL BIOTECH’s Q3 2025 Earnings Report: The Key Figures

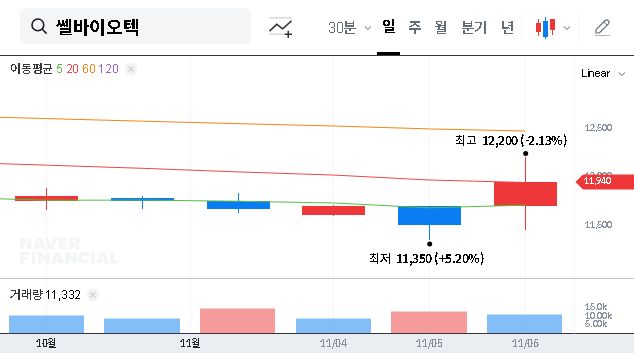

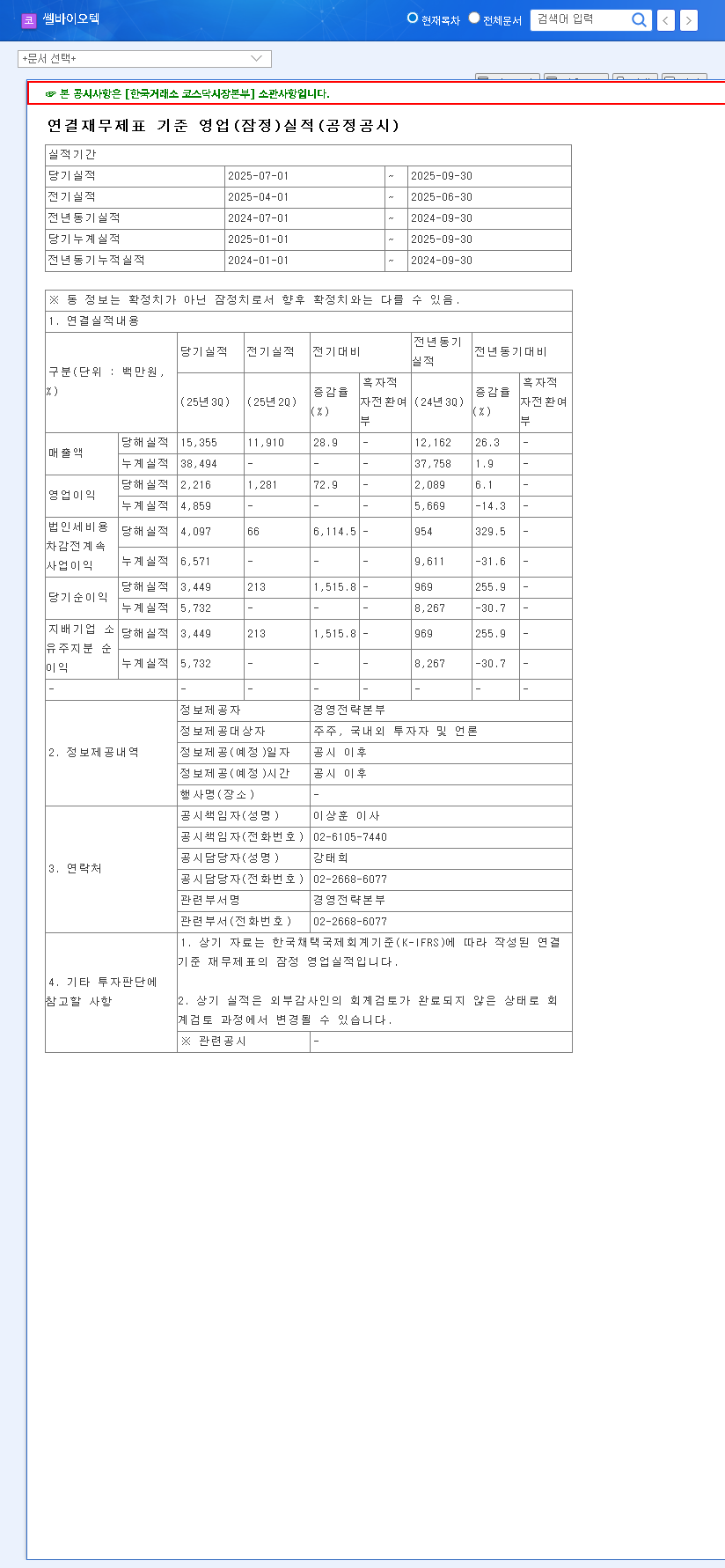

On November 6, 2025, CELL BIOTECH released its consolidated provisional earnings, offering a clear snapshot of its operational health. The quarter-over-quarter improvements signal a positive recovery and strengthening business fundamentals.

- •Revenue: 15.4 billion KRW (A notable increase from 11.9 billion KRW in Q2 2025)

- •Operating Profit: 2.2 billion KRW (Up significantly from 1.3 billion KRW in Q2 2025)

- •Net Income: 3.4 billion KRW (A dramatic improvement from 0.2 billion KRW in Q2 2025)

These figures, particularly the sharp rise in net income, highlight not only core business recovery but also effective financial management. For a complete breakdown, refer to the Official Disclosure (DART).

Fundamental Strengths: The Twin Pillars of Growth

A thorough CELL BIOTECH analysis reveals two primary drivers of its value: a dominant position in the established probiotics market and a high-potential pipeline in oncology.

1. Global Dominance in the Probiotics Market

For over a quarter-century, CELL BIOTECH has honed its expertise in probiotics. Its flagship ‘Dual Coating’ technology is a significant competitive advantage, protecting probiotics from stomach acid and bile salts to ensure their delivery to the gut. This innovation is the bedrock of its success, culminating in an impressive 11-year streak as the world’s #1 exporter of probiotics. This isn’t just a revenue stream; it’s a testament to the company’s quality, stability, and global trust.

2. The Future: Oncology Drugs and Microbiome Innovation

The most exciting catalyst for future growth is the company’s foray into oncology drugs. The anti-cancer drug candidate, PP-P8, represents a paradigm shift, leveraging the microbiome to potentially treat diseases like colorectal cancer. The commencement of Phase 1 clinical trials at Seoul National University Hospital in March 2025 was a pivotal milestone. As of November 2025, patient recruitment is actively underway, a crucial step in advancing this promising therapy. The potential market for effective cancer treatments is immense, as detailed by organizations like the World Health Organization, making PP-P8 a key asset to watch.

CELL BIOTECH’s strategy smartly combines a stable, cash-generating probiotics business with the high-growth, transformative potential of its oncology drug pipeline. This provides both a solid foundation and a significant upside for investors.

Financial Health & Market Headwinds

Beyond the income statement, CELL BIOTECH’s balance sheet is exceptionally robust. With a debt-to-equity ratio of just 4.91% and over 86 billion KRW in cash and short-term financial instruments, the company is well-capitalized. This financial fortitude is critical, as it allows CELL BIOTECH to fund its long-term R&D for oncology drugs like PP-P8 without relying on dilutive financing. However, the company must navigate a complex macroeconomic environment, including high interest rates that could temper investment returns and a volatile KRW/USD exchange rate, which, given its export focus, can positively impact profitability.

Investor Outlook & Strategic Action Plan

The CELL BIOTECH Q3 2025 earnings paint a picture of a company in a strong position but facing key inflection points. The quarter-over-quarter recovery is reassuring, but the limited year-over-year operating profit growth suggests that investments in new ventures are impacting short-term margins.

What Investors Should Monitor:

- •Clinical Trial Progress: Any updates on the Phase 1 trial for PP-P8 will be a major stock catalyst. Positive data could significantly de-risk the pipeline.

- •Margin Expansion: Keep an eye on operating profit in upcoming quarters. Investors will want to see if the company can translate revenue growth into stronger profitability as new ventures mature.

- •Diversification Success: Monitor the growth of newer segments like the ‘Cellbiome’ service and pet-focused products. To learn more, read our analysis on the pet wellness market.

In conclusion, CELL BIOTECH presents a compelling long-term investment case grounded in proven market leadership and transformative innovation. While short-term macroeconomic factors and R&D costs warrant consideration, the positive signals from the Q3 2025 earnings reaffirm the company’s solid growth trajectory.

Frequently Asked Questions (FAQ)

What were CELL BIOTECH’s key Q3 2025 financial results?

For Q3 2025, CELL BIOTECH reported revenue of 15.4 billion KRW, operating profit of 2.2 billion KRW, and net income of 3.4 billion KRW, all showing strong improvement from the previous quarter.

What is the status of the PP-P8 anti-cancer drug trial?

As of November 2025, the Phase 1 clinical trial for PP-P8 is actively recruiting patients at Seoul National University Hospital after receiving IND approval earlier in the year.

Why is CELL BIOTECH a leader in the probiotics market?

Its globally recognized ‘Dual Coating’ technology ensures the effectiveness of its products, leading to its position as the world’s #1 exporter of probiotics for 11 consecutive years.

Leave a Reply