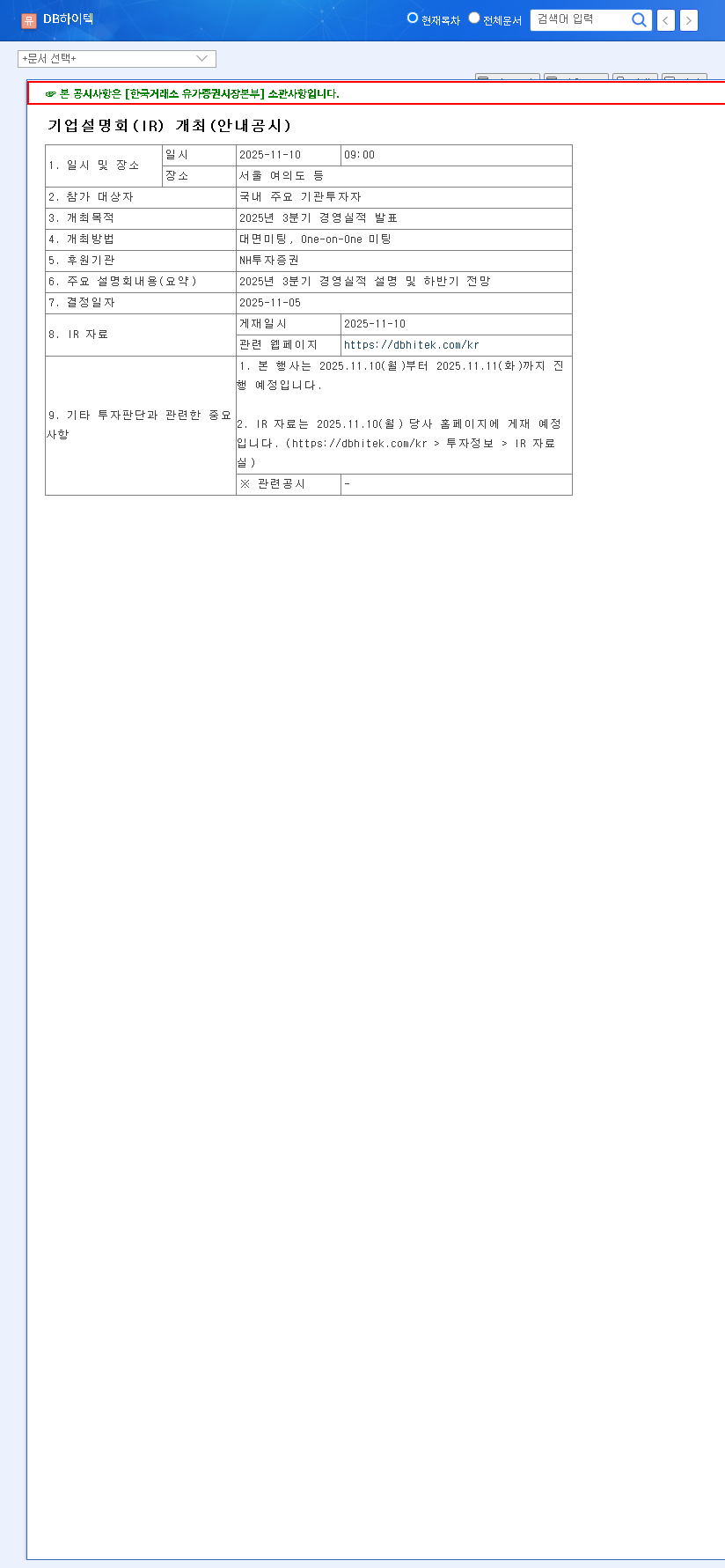

The upcoming DB HiTek Q3 earnings presentation, scheduled for November 10, 2025, is more than just a financial report; it’s a critical barometer for the company’s trajectory amidst significant semiconductor market volatility. As investors grapple with macroeconomic uncertainties, this investor relations (IR) conference will provide crucial insights into DB HiTek’s resilience, strategic pivots, and future growth drivers. Can the 8-inch foundry specialist navigate the headwinds and chart a course for renewed momentum?

This in-depth analysis of DB HiTek fundamentals explores the challenges highlighted in recent reports and the underlying strengths that could propel its long-term success. From enhancing shareholder value to fortifying its competitive edge in the foundry business, we will dissect the key factors that will define DB HiTek’s path forward.

Analyzing DB HiTek’s Financial Health

Navigating Revenue Headwinds and Profitability Concerns

A review of DB HiTek’s H1 2025 performance reveals significant challenges. The company has faced a year-over-year revenue decline, largely attributed to the broader macroeconomic slowdown and ongoing inventory corrections by key clients in the consumer electronics sector. The 2025 forecast anticipates a transition to an operating deficit, a stark contrast to previous years and a major point of concern for investors.

The pivotal question for the DB HiTek Q3 earnings call is whether the company can demonstrate a clear and credible strategy to reverse this trend and return to profitable growth in 2026.

- •Revenue Trajectory: Projected to fall from KRW 1,147.7 billion in 2022 to KRW 469.4 billion in 2025.

- •Operating Profit: Expected to shift from a KRW 175.8 billion profit in 2022 to a KRW -30.8 billion loss in 2025.

- •Profit Margin Erosion: Operating profit margin is forecasted to plummet from 15.32% to -6.55%.

Investors can view the official filings for more detailed information. (Official Disclosure)

Underlying Strengths and Growth Catalysts

Despite the concerning short-term outlook, DB HiTek possesses fundamental strengths that form its long-term growth thesis. The company is strategically investing in high-value process technologies like Gallium Nitride (GaN) and Silicon Carbide (SiC). These next-generation materials are crucial for high-efficiency power electronics used in electric vehicles (EVs), 5G infrastructure, and data centers—markets with robust secular growth. For more on this trend, see the latest analysis from the Semiconductor Industry Association.

Furthermore, strengthening its Analog & Power process competitiveness and expanding its international client base are key initiatives. A commitment to shareholder-friendly policies, including share buybacks, also provides a degree of support for its stock analysis.

Market Dynamics & External Factors

The semiconductor foundry market is notoriously cyclical, and DB HiTek is exposed to several external variables. Intense price competition in the 8-inch foundry space continues to pressure margins. Competitors are vying for market share, making operational efficiency and technological differentiation paramount. For a deeper look, you can read our Deep Dive into the 8-inch Foundry Market.

Key Macroeconomic Pressures

- •Exchange Rates: A strong KRW/USD exchange rate can boost export revenues but simultaneously increases the cost of imported raw materials and equipment.

- •Interest Rates: Global interest rate policies affect capital expenditure costs and overall market sentiment, influencing stock valuations.

- •Geopolitical Risks: Ongoing global tensions and trade disputes can disrupt supply chains and impact end-market demand, creating an unpredictable environment.

Key Questions for the DB HiTek Investor Relations Call

The upcoming DB HiTek investor relations event is a chance for management to address market anxieties. Investors should listen closely for clear, data-driven answers to the following:

- •Foundry Business Outlook: What is the current order book status? Are there signs of demand recovery from key overseas markets like China and the US?

- •Technology Roadmap: What is the commercialization timeline for GaN and SiC technologies? How will these high-value products contribute to future revenue and margins?

- •Forward Guidance: What are the specific financial projections for Q4 2025 and the full year 2026? How does management plan to navigate the projected operating loss?

- •Shareholder Returns: Beyond existing policies, are there new initiatives planned to enhance shareholder value and improve corporate governance?

Conclusion: A Pivotal Moment for DB HiTek

The DB HiTek Q3 earnings report will be a moment of truth. While short-term financial metrics are under pressure, the company’s long-term value hinges on its ability to execute its technology roadmap and capitalize on next-generation semiconductor trends. The clarity and confidence of the management team’s message during the IR conference will be just as important as the numbers themselves. A compelling and transparent growth story could reassure the market and set the stage for a future recovery, making this a must-watch event for any serious investor in the semiconductor space.

Leave a Reply