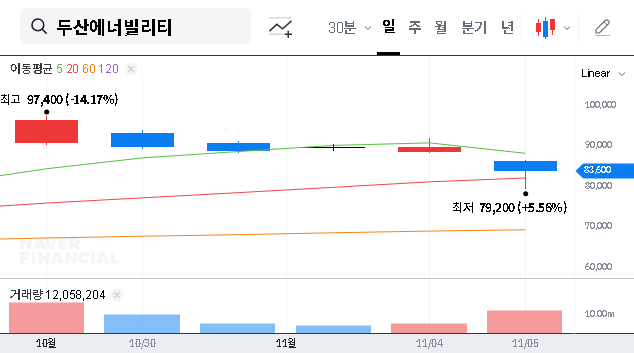

The latest Doosan Enerbility Q3 earnings report for 2025, released on November 5th, sent a shockwave through the market. The preliminary results for DOOSAN ENERBILITY CO., LTD. (034020) fell dramatically short of analyst consensus, revealing significant operational and financial headwinds. For investors, this moment is critical. It raises urgent questions about the company’s profitability, its strategic direction, and the viability of a near-term recovery. This comprehensive Doosan Enerbility stock analysis will dissect the disappointing numbers, explore the underlying causes, and provide a clear, actionable investment outlook.

Q3 2025 Performance: A Stunning Miss

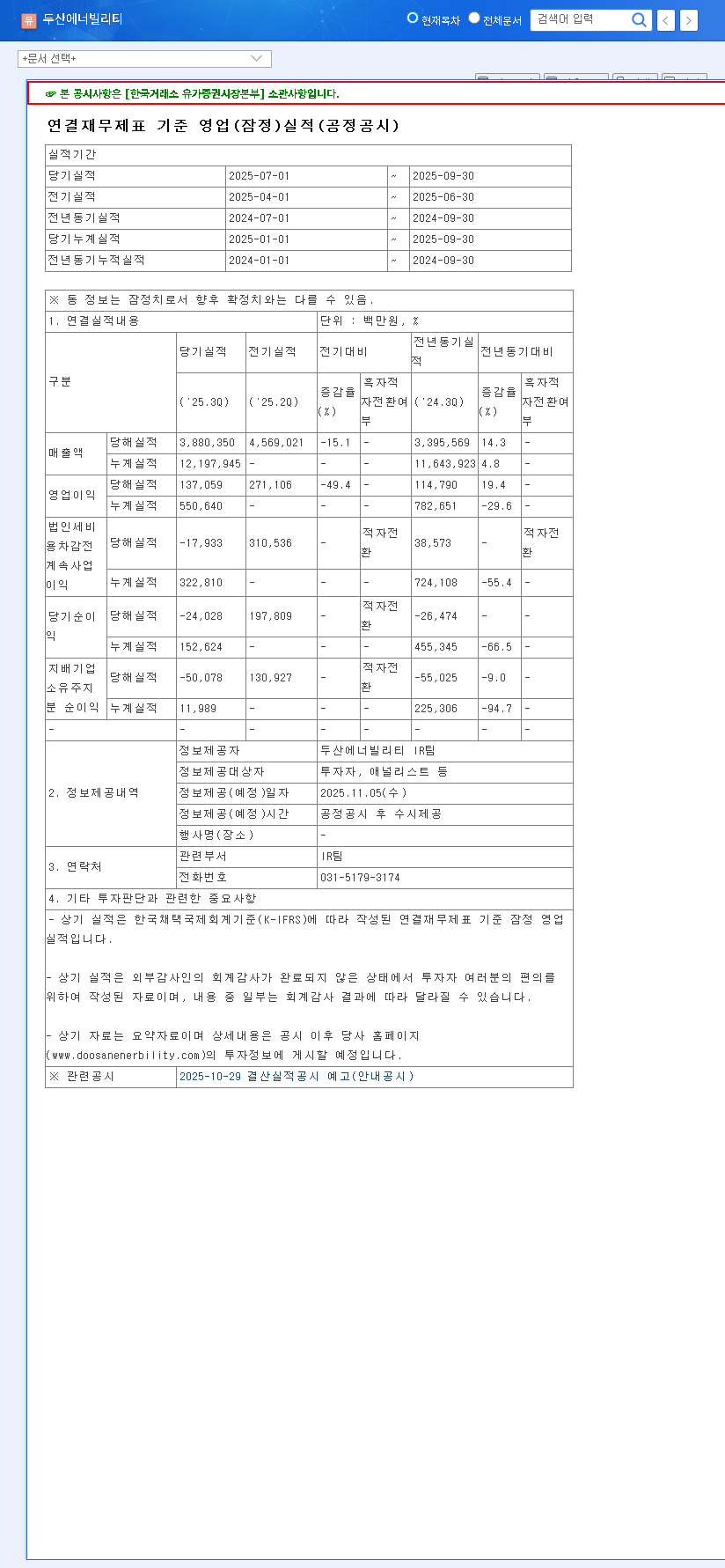

The preliminary consolidated financial results painted a grim picture, with every key metric failing to meet market expectations. The magnitude of the miss, particularly in profitability, suggests issues that may be more structural than temporary. The official figures, as per the company’s disclosure, are a cause for significant concern for anyone conducting a thorough Doosan Enerbility investment analysis.

Here is a breakdown of the key figures from the report. For full transparency, investors can review the Official Disclosure (DART).

- •Revenue: KRW 3.88 trillion, missing the estimate of KRW 4.02 trillion by 4.0%.

- •Operating Profit: KRW 137.1 billion, a staggering 51.7% below the estimate of KRW 282.9 billion.

- •Net Income: A loss of KRW -50.1 billion, completely reversing the expected profit of KRW 156.8 billion—a 132% negative swing.

While a revenue dip is concerning, the collapse in operating profit and the swing to a net loss signals severe margin compression. This suggests that the company is struggling with rising costs, operational inefficiencies, or a combination of both.

“The Q3 report is a red flag. The market can forgive a top-line miss in a tough economy, but a profitability collapse of this scale points to deeper internal challenges. We’re now closely watching for management’s plan to stabilize margins and restore investor confidence.”

Analyzing the Underperformance: A Two-Front Battle

Doosan Enerbility’s poor 034020 performance can be attributed to a confluence of internal operational struggles and a volatile external macroeconomic environment.

Internal Factors: Worsening Profitability and Execution Gaps

The Doosan Enerbility Q3 earnings report continues a troubling trend noted in the first half of 2025. Key internal drivers of the underperformance include:

- •Core Business Decline: Both the main Enerbility division (power plants, turbines) and the Doosan Bobcat division faced revenue challenges, indicating broad-based weakness.

- •Cost Pressures: Surging raw material costs, coupled with increased selling, general, and administrative (SG&A) expenses, have severely eroded profitability. The inability to pass these costs on to customers is a major concern.

- •Transition Pains: The strategic pivot towards eco-friendly energy sources like hydrogen, wind, and Small Modular Reactors (SMRs) is capital-intensive. These investments are not yet generating enough revenue to offset the decline in legacy businesses, creating a drag on current earnings. You can read more in our deep dive into the future of SMR technology.

External Environment: Navigating Global Headwinds

The global economic landscape has been unforgiving, compounding Doosan’s internal issues. As noted by sources like Bloomberg’s economic analysis, several factors are at play:

- •Global Trade Slowdown: Key shipping indicators like the Baltic Dry Index have been trending downward, signaling a contraction in global trade. This directly impacts a heavy industrial exporter like Doosan, leading to project delays and reduced order flow.

- •Currency Volatility: While a weaker Won can benefit exports, it also inflates the cost of imported raw materials, putting further pressure on margins.

- •Geopolitical Instability: Ongoing global conflicts increase market uncertainty, causing corporations to delay major capital expenditures—the very projects that form Doosan’s core business.

Investment Outlook and Strategic Recommendations

Given the severe Doosan Enerbility underperformance, investors must adopt a cautious and strategic approach. The market’s reaction will likely be negative in the short term, with significant downward pressure on the stock price.

Short-Term Strategy: Observe and Verify

A knee-jerk reaction is ill-advised. The immediate priority is to wait for the full, detailed earnings report and the subsequent management conference call. Key areas to watch are:

- •Management’s Explanation: A clear, credible explanation for the profitability collapse is essential.

- •Cost Control Measures: Concrete plans for improving operational efficiency and controlling SG&A expenses.

- •Updated Guidance: Any revision to the full-year or 2026 outlook will be a key indicator of future performance.

Mid-to-Long-Term Strategy: Focus on the Turnaround Story

For long-term investors, the focus shifts to the viability of Doosan’s strategic pivot. The Doosan Enerbility investment thesis hinges on its successful transformation into a green energy powerhouse. Monitor these key pillars:

- •New Energy Order Book: Look for tangible progress in securing contracts for nuclear SMRs, hydrogen turbines, and large-scale wind projects.

- •Financial Health: Keep an eye on the debt-to-equity ratio and operating cash flow. A successful turnaround requires a stable financial foundation.

- •Doosan Bobcat Performance: A recovery in this key subsidiary is crucial for providing the cash flow needed to fund the energy transition.

In conclusion, the Doosan Enerbility Q3 earnings are a significant setback. While the short-term outlook is bearish, the long-term potential remains, albeit with increased risk. Prudent investors will exercise caution, demand clarity from management, and wait for evidence of a fundamental turnaround before committing new capital.

Leave a Reply