The latest d’Alba Global earnings report for Q3 2025 has sent a wave of concern through the investment community. For a company celebrated for its premium vegan beauty brand ‘d’Alba’ and its impressive growth trajectory, the preliminary figures were a significant disappointment. Investors are now grappling with critical questions: Was this a temporary setback or a sign of deeper issues? And what is the most prudent d’Alba investment strategy moving forward? This deep-dive analysis unpacks the numbers, explores the underlying causes, and provides a clear roadmap for evaluating the future of d’Alba Global stock.

Deconstructing the d’Alba Global Earnings Shock

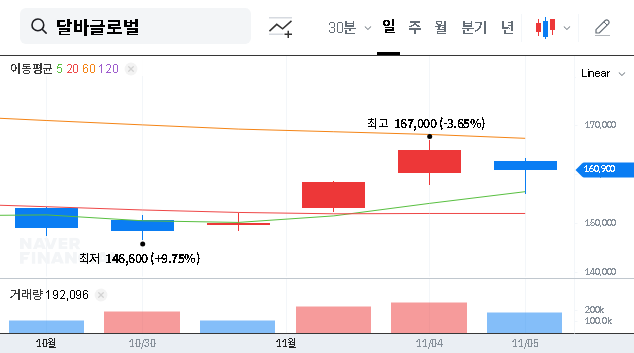

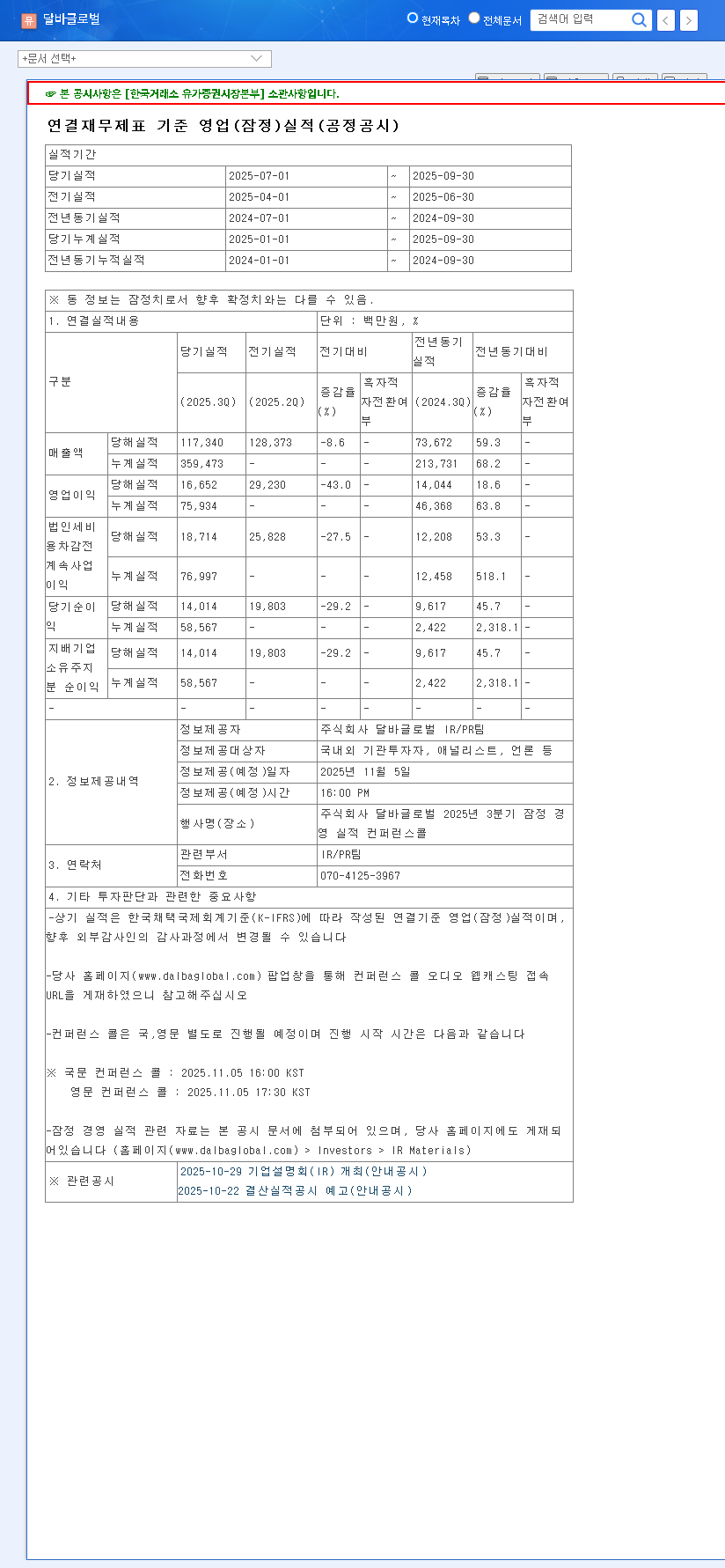

The preliminary Q3 results, released on November 5, 2025, fell alarmingly short of consensus expectations, particularly on the profitability front. The official figures paint a stark picture, which you can verify in the company’s Official Disclosure. Let’s examine the key metrics:

- •Revenue: KRW 117.3 billion, missing market expectations by 5.0%.

- •Operating Profit: KRW 16.7 billion, a staggering 31.0% below expectations.

- •Net Profit: KRW 14.0 billion, an even more dramatic 44.0% miss.

While a revenue miss is concerning, the severe underperformance in operating and net profit points to a significant erosion of the company’s profitability. This is the core issue that has rattled investor confidence and demands a closer look.

The Alarming Plunge in Profit Margins

To understand the severity, we must compare this quarter to past performance. In the first half of 2025, d’Alba Global was a model of profitability, boasting an operating profit margin of 24.48%. In Q3, that figure collapsed to just 14.24%. Similarly, the net profit margin fell from 18.38% to 11.94%. This isn’t just a minor fluctuation; it suggests a fundamental shift in the company’s cost structure or pricing power. The quarter-over-quarter revenue also declined by 8.6%, indicating that the growth engine is sputtering, at least temporarily.

The Q3 results reveal a dual threat: slowing top-line growth combined with rapidly deteriorating bottom-line profitability. This combination is a significant red flag for any growth-oriented company.

Balancing Strengths Against Market Headwinds

Before this report, the investment thesis for 483650 stock analysis was built on solid fundamentals. It’s crucial to weigh these enduring strengths against the new macroeconomic challenges.

Enduring Company Strengths

- •Strategic Diversification: Management has wisely expanded beyond cosmetics into health foods (‘Veganery’) and beauty devices, which could provide new, resilient revenue streams. You can read more about this trend in our analysis of the K-beauty market.

- •Global Footprint: Aggressive expansion into international markets remains a primary growth lever, reducing dependency on the domestic market.

- •Financial Stability: A low debt-to-equity ratio of 25.41% (as of H1 2025) means the company is not over-leveraged and has the financial health to weather downturns.

Mounting Macroeconomic Pressures

Unfortunately, d’Alba Global operates in a challenging global environment. Several external factors are likely contributing to the margin compression:

- •Currency & Commodity Costs: A rising KRW/USD exchange rate and higher oil prices (WTI $60.43) directly increase the cost of imported raw materials and manufacturing.

- •Logistics Expenses: A surge in international shipping indices means higher costs to get products to its global customers.

- •Interest Rate Environment: As reported by sources like Bloomberg, rising US 10-Year Treasury yields typically lead to investor risk aversion, which disproportionately affects growth stocks like d’Alba Global.

The Investor’s Action Plan: A Cautious Path Forward

Given the negative sentiment surrounding the d’Alba Global earnings, a reactive decision could be costly. A prudent and strategic approach is required. The stock price will likely face significant downward pressure in the short term. For long-term investors, the focus should be on verification and patience.

Key Actions for Investors:

- •Analyze the Q4 Outlook: Pay close attention to management’s guidance for the upcoming quarter during their next earnings call. Are they providing a concrete plan to restore margins?

- •Scrutinize New Ventures: Demand clear data on the performance of the ‘Veganery’ and beauty device segments. Are they contributing meaningfully to revenue and, more importantly, profit?

- •Monitor Macro Indicators: Keep an eye on the macroeconomic factors mentioned above. A stabilization or reversal in these trends could provide a tailwind for the company.

- •Adopt a ‘Wait and See’ Stance: Avoid making hasty buys or sells. The prudent move is to wait for Q4 results and 2026 guidance to confirm whether the company can navigate these challenges and reignite its growth story.

In conclusion, while d’Alba Global’s long-term potential from diversification and global expansion remains, the Q3 earnings have introduced serious profitability concerns. The path forward for investors is to demand evidence of a turnaround before committing further capital. The narrative has shifted from pure growth to one of resilience and margin recovery.

Disclaimer: This report is based on the provided information and analysis; the final responsibility for investment decisions rests with the investor.

Leave a Reply