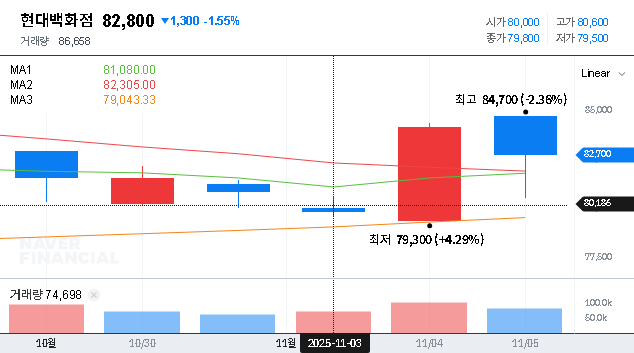

The latest Hyundai Department Store investment has sent ripples through the market. The company, HYUNDAI DEPARTMENT STORE CO.,LTD (069960), has officially committed a staggering KRW 150 billion to ‘The Hyundai Gwangju’, a move that signals a bold vision for future growth. This strategic decision is far more than a simple capital injection; it’s a calculated gamble to solidify its retail dominance. For investors, the critical question is whether this ambitious expansion will catalyze long-term value or become a significant short-term financial burden. This in-depth stock analysis will dissect the investment, evaluate its impact on the company’s fundamentals, and provide a clear action plan for current and prospective shareholders.

Deconstructing the ₩150 Billion Hyundai Department Store Investment

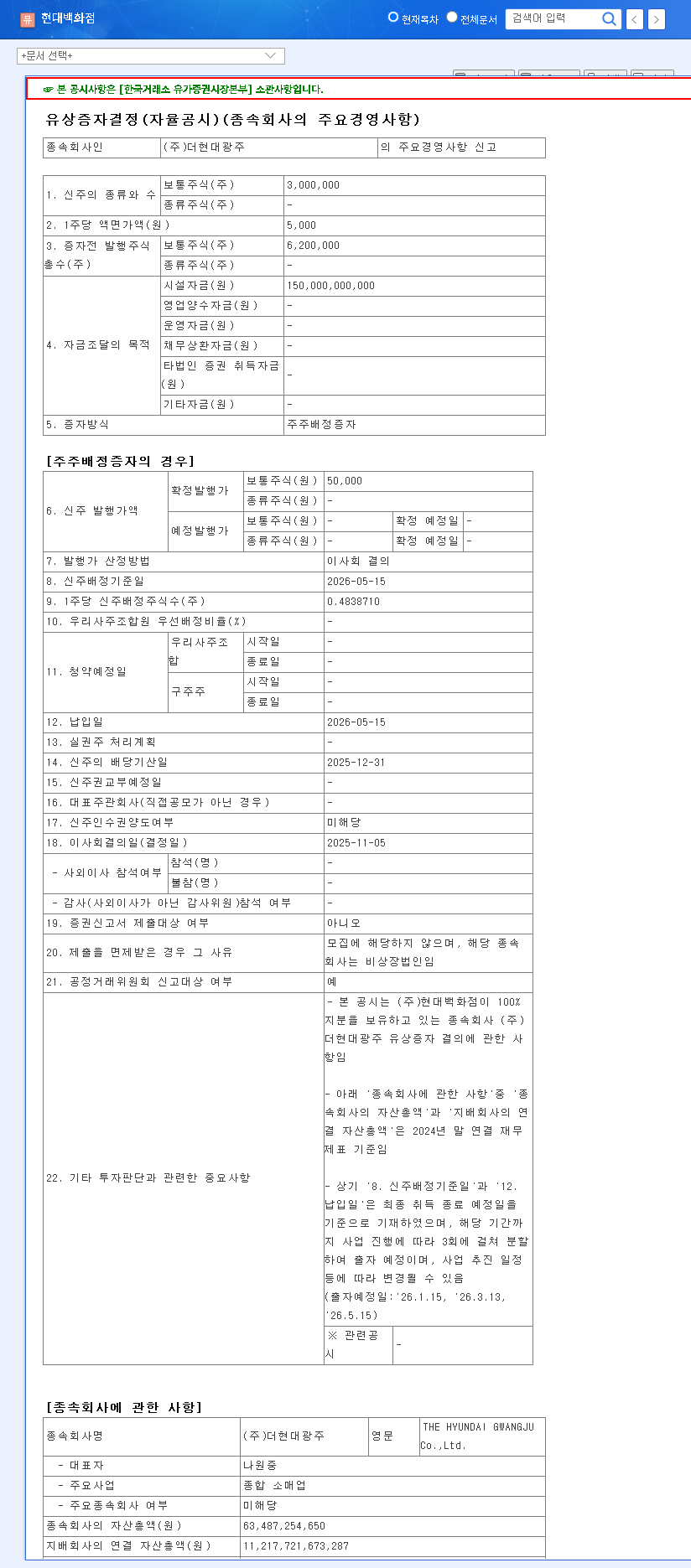

Hyundai Department Store has finalized its decision to acquire shares and equity securities by participating in the capital increase of its subsidiary, ‘The Hyundai Gwangju’. This ₩150 billion transaction, scheduled for completion by May 15, 2026, will grant the parent company 100% ownership. The primary objective is to fuel the development of a landmark retail space in the Gwangju metropolitan area, continuing the successful formula seen with ‘The Hyundai Seoul’. According to the Official Disclosure, this capital is earmarked for securing a strong foundation for the new venture’s business stability and future expansion.

The Strategic Rationale: The Bull Case

From a strategic viewpoint, the investment is a clear expression of the company’s commitment to growth. It aligns perfectly with their stated goal of establishing a robust distribution network across South Korea’s five major metropolitan cities. By planting a flagship store in Gwangju, Hyundai aims to capture a new regional market and enhance its overall brand prestige and competitiveness. The successful launch of ‘The Hyundai Gwangju’ could significantly expand market share and contribute to sustained revenue growth in the core department store segment for years to come.

- •Long-Term Growth Engine: A positive signal to the market about the company’s long-term vision and willingness to invest in its future.

- •Market Dominance: Strengthens its position in the competitive luxury retail sector, a key focus of our annual retail sector report.

- •Brand Enhancement: Replicates the ‘destination’ retail model that has proven immensely successful, attracting new demographics.

The Financial Reality: The Bear Case

Despite the strategic upside, the ₩150 billion cash outflow presents a tangible short-term risk. This substantial expenditure could create temporary liquidity pressure. More critically, Hyundai Department Store currently operates with a relatively high debt-to-equity ratio, and its net borrowings have been on an upward trend. In a persistent high-interest-rate environment, as analyzed by leading economists at major financial institutions, any additional fundraising required to finance this project could lead to a significant increase in interest expenses, potentially eroding profitability. While the investment represents only 2.41% of total capital and isn’t critically detrimental, the funding plan for 2026 must be meticulously managed and monitored.

While the vision for ‘The Hyundai Gwangju’ promises significant long-term rewards, investors must weigh this against the immediate financial pressures and macroeconomic headwinds facing the company. Prudent analysis is key.

Broader Business & Economic Outlook

No investment exists in a vacuum. The success of this venture depends heavily on the macroeconomic climate and the performance of Hyundai’s other key business segments.

Macroeconomic Headwinds

Fluctuations in benchmark interest rates in both the US and Korea directly impact the company’s financial costs and consumer spending power. Persistent inflation and high rates can dampen consumer sentiment, particularly in the premium and luxury goods sectors that department stores rely on. Exchange rate volatility (USD/KRW) also poses a risk, especially for the cost competitiveness and overseas sales of its furniture subsidiary, ZINUS.

Performance of Key Business Segments

- •Department Stores: This core segment has shown solid revenue recovery, but operates in a fiercely competitive landscape. New store openings like ‘The Hyundai Gwangju’ are vital for securing future growth.

- •Duty-Free: Performance is gradually improving with the rebound in international tourism, but achieving strong profitability remains a pressing challenge.

- •Furniture (ZINUS): Expected to grow through global market expansion and a strong online presence. However, it must navigate shifting product demands, intense competition, and volatile logistics costs.

Investor Action Plan & Final Recommendation

The Hyundai Department Store investment in ‘The Hyundai Gwangju’ is a classic case of balancing long-term ambition with short-term risk. The strategic logic is sound and essential for future growth. However, the financial implications, particularly in the current economic climate, cannot be ignored.

Given this balance, the immediate event is unlikely to cause major stock price volatility. The mid-to-long-term trajectory, however, hinges on the successful execution of this project. Therefore, a ‘Hold’ opinion is appropriate. Investors should maintain their positions while closely monitoring key developments.

Key Monitoring Points for Investors

- •Detailed progress and construction timelines for ‘The Hyundai Gwangju’.

- •The company’s specific funding strategy for the 2026 capital injection and any changes to its debt profile.

- •Quarterly performance trends across all major business segments.

- •Shifts in macroeconomic indicators, especially consumer sentiment and interest rate policies.

Disclaimer: This analysis is based on publicly available information. Investment decisions carry risk and should be made based on an individual’s own judgment and financial situation.

Leave a Reply