The recent SunBio stock cancellation has captured significant market attention. SunBio, Inc. (선바이오) announced a plan to cancel 1 billion KRW in treasury stock, a move widely seen as a commitment to boosting shareholder value. However, for savvy investors, this action warrants a deeper look beyond the headlines. Is this a sign of sustainable growth, or a short-term boost for a company facing financial headwinds?

This comprehensive analysis will dissect the stock cancellation event, evaluate SunBio’s fundamental financial health, assess its promising but uncertain business pipeline, and consider the macroeconomic landscape. Our goal is to provide investors with the critical insights needed to make informed decisions about SunBio’s long-term potential.

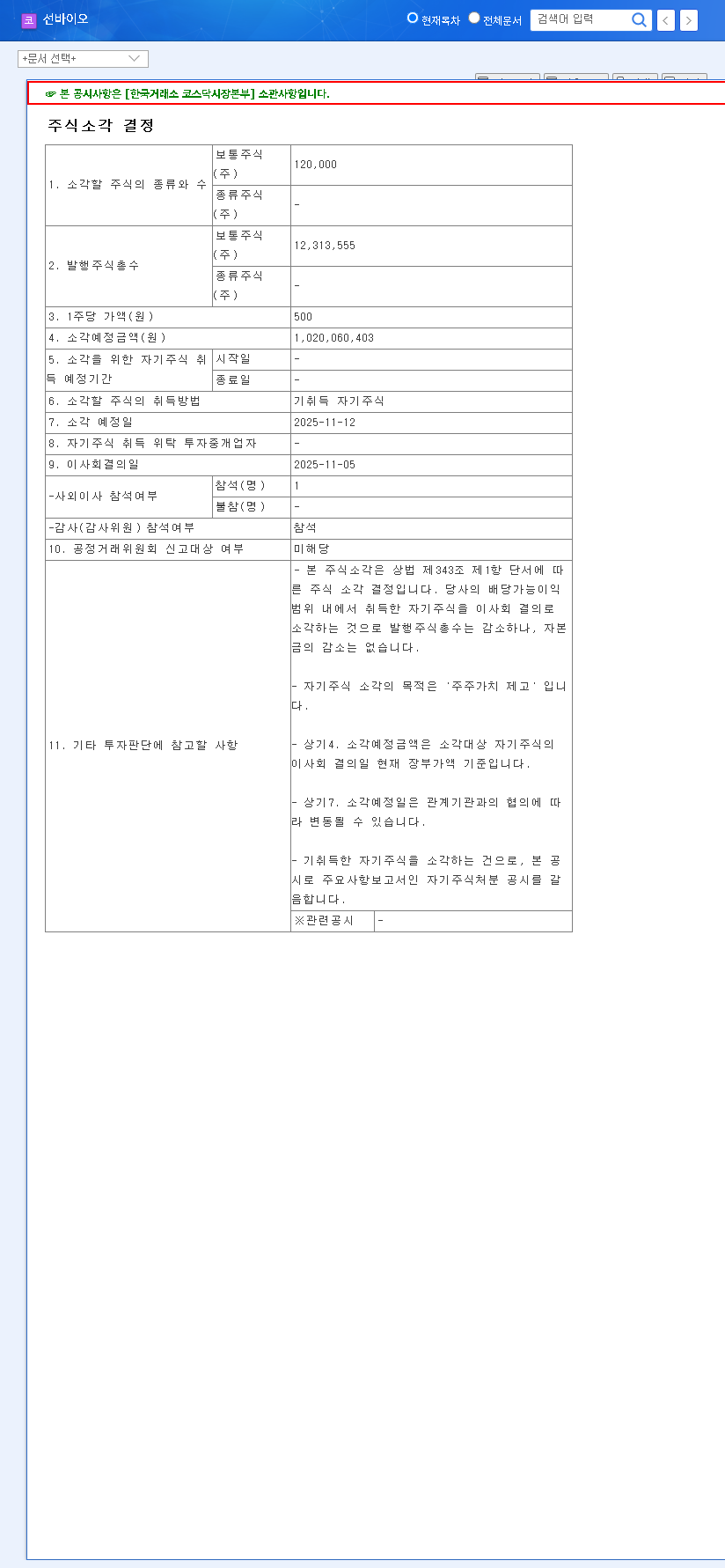

Deconstructing the SunBio Stock Cancellation

On November 5, 2025, SunBio’s board made a decisive move: the cancellation of 120,000 common shares held as treasury stock. This action, valued at approximately 1 billion KRW, removes 1.58% of the company’s market capitalization from circulation. The cancellation is officially scheduled for November 12, 2025, as detailed in their Official Disclosure (DART).

By reducing the total number of outstanding shares, the value of each remaining share theoretically increases. This is a classic strategy to enhance SunBio shareholder value and signal confidence from management to the market. However, its true impact is intrinsically linked to the company’s underlying financial strength.

Treasury stock cancellation is a powerful signal. It tells investors that management believes the company’s shares are undervalued and that returning capital to shareholders is a better use of funds than other investment opportunities at this moment.

A Financial Health Check: The Numbers Behind SunBio

The Revenue and Profit Paradox

SunBio’s H1 2025 report presents a mixed financial picture. While revenue saw a significant year-over-year decrease of 59.7% to 4.75 billion KRW, the company successfully managed a turnaround in operating profit to 118 million KRW. This was achieved through aggressive cost-cutting in sales, general, and administrative expenses. While operational efficiency is commendable, the sharp revenue decline remains a primary concern that cost control alone cannot solve indefinitely. Furthermore, a widening net loss of 1.187 billion KRW, driven by financial costs, signals ongoing pressures.

Debt, Liquidity, and Risk Management

With a debt-to-equity ratio of 130.32%, SunBio is more leveraged than many of its peers. A high proportion of current liabilities combined with insufficient cash reserves to cover short-term debt obligations means liquidity management is paramount. Investors must watch for improvements in cash flow and any efforts to restructure or pay down debt. For a deeper understanding of financial ratios, you can explore resources from authoritative sites like Bloomberg’s financial analysis section.

SunBio’s Business Pipeline: Potential and Pitfalls

A company’s future is defined by its products and innovations. Here’s a look at SunBio’s core and emerging business lines:

- •PEG Derivatives: This core business faced a temporary production halt for new plant certification, causing the recent revenue dip. With operations normalizing, revenue is expected to recover in the latter half of the year, driven by a solid order backlog.

- •Pegfilgrastim (Neutropenia Treatment): Awaiting U.S. FDA approval, this biologic could be a game-changer for SunBio. Pegfilgrastim is a long-acting treatment for low white blood cell counts, often a side effect of chemotherapy, and represents a significant market opportunity. Approval would be a major catalyst.

- •New Ventures (Secondary Battery Electrolytes): Diversification into high-growth areas like battery technology shows foresight. However, these ventures are in their infancy and carry inherent uncertainty and capital requirements. Their success is a long-term play.

Investor Action Plan: Key Checkpoints

While the SunBio stock cancellation is a positive short-term signal, a long-term investment thesis must be built on fundamental progress. Investors should maintain a watchlist focused on the following key areas. For more tips on portfolio management, consider reading our guide on evaluating biotech stocks.

- •Tangible Growth: Watch for a rebound in PEG derivative sales and, most importantly, any news regarding the U.S. FDA approval of Pegfilgrastim. This is the single most significant potential catalyst on the horizon.

- •Financial Fortitude: Monitor quarterly reports for improvements in the debt-to-equity ratio, positive cash flow generation, and a reduction in net losses. Sustainable profitability is the ultimate goal.

- •Macroeconomic Sensitivity: As an exporter, SunBio is sensitive to EUR/KRW and USD/KRW exchange rate fluctuations. Keep an eye on global currency trends and how they might impact earnings.

In conclusion, SunBio’s stock cancellation is a welcome gesture of shareholder-friendliness. It provides a short-term tailwind for investor sentiment. However, the company’s long-term trajectory will be determined not by financial engineering, but by its ability to execute on its business plan, secure regulatory approvals, and fundamentally improve its financial health.

Leave a Reply