The latest SKC LTD earnings report for Q3 2025 has sent significant ripples through the investment community, revealing a stark underperformance that widely missed market expectations. With mounting operating losses and declining revenue, investors are questioning the path forward for the materials giant. This comprehensive analysis unpacks the official SKC LTD financial results, explores the structural issues plaguing its core businesses, and provides a clear-eyed view of its future outlook and what it means for the company’s stock.

Dissecting the Q3 2025 SKC LTD Earnings Report

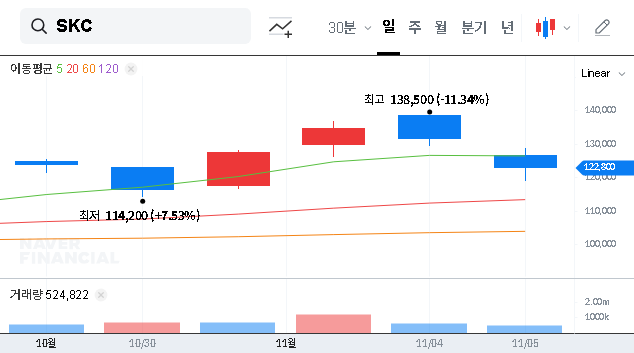

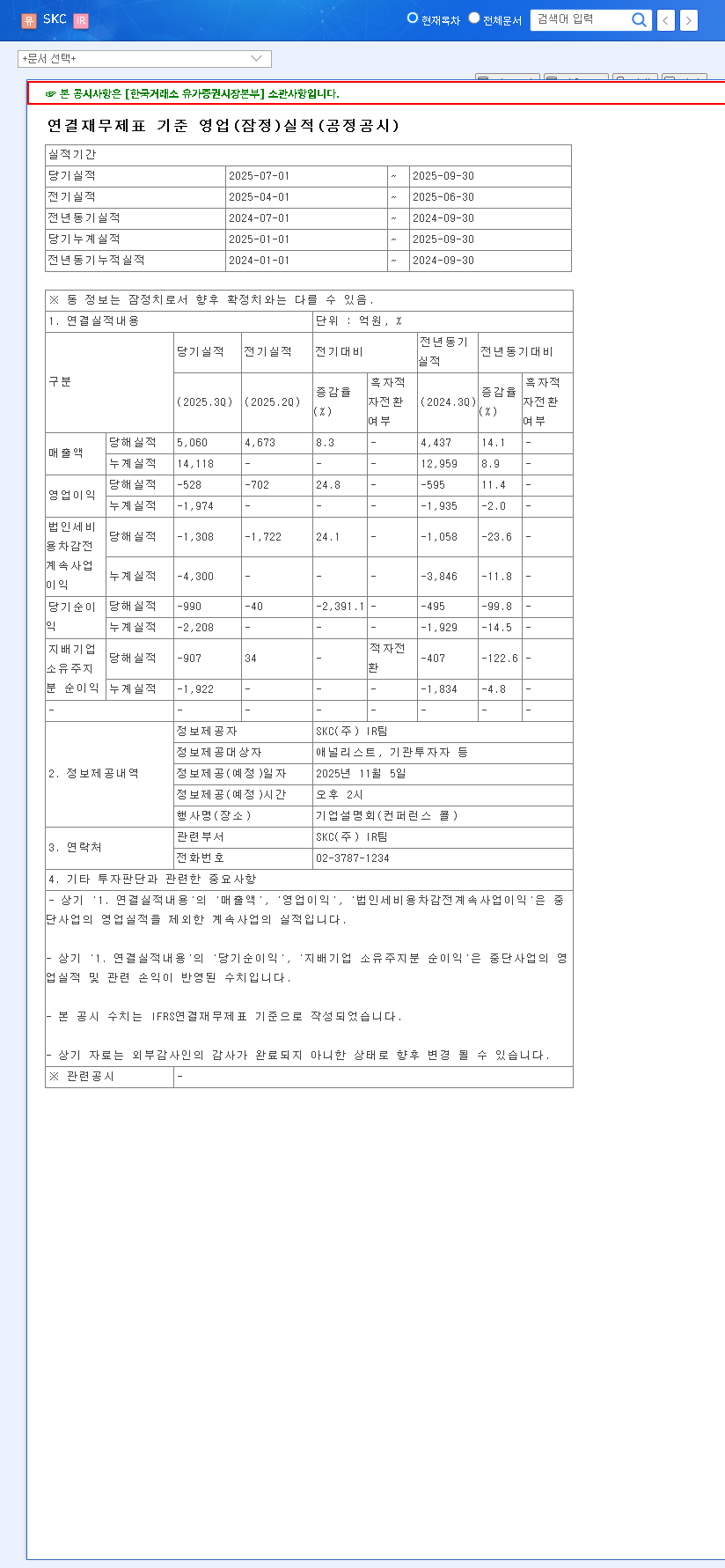

SKC LTD’s preliminary Q3 2025 results painted a challenging picture, marking its third consecutive quarter of operating losses. The numbers highlight a significant downturn compared to the previous year and fell far short of consensus estimates, triggering concerns about the company’s near-term profitability and financial stability.

Key Financial Highlights:

– Consolidated Revenue: KRW 506 billion (a 70.5% decrease year-on-year).

– Operating Loss: KRW 52.8 billion (a stark reversal from a KRW 276.8 billion profit in the prior year).

– Net Loss: KRW 90.7 billion.

– Debt-to-Equity Ratio: 188%, indicating significant financial leverage.

This performance points to deep-seated issues within SKC’s primary business segments. For a complete breakdown of the financial data, investors can refer to the Official Disclosure filed with DART, which provides granular detail on the company’s filings.

What’s Behind the Underperformance? A Sector-by-Sector Breakdown

The poor SKC LTD earnings are not the result of a single issue but a confluence of challenges across its main divisions, compounded by macroeconomic pressures.

Secondary Battery Materials: A Perfect Storm

The secondary battery materials business, once a key growth driver, is now facing a perfect storm. A notable slowdown in the global Electric Vehicle (EV) market, as detailed by sources like BloombergNEF, has led to widespread inventory adjustments by battery cell makers. This directly impacted SK Nexilis, whose copper foil plant in Poland operated at a mere 58.6% utilization. This low rate drastically increases the fixed cost burden per unit produced, crushing profitability in a market already experiencing intense price competition.

Semiconductor Materials: Cyclical Downturns and Integration Questions

Similarly, the semiconductor materials business is suffering from the well-documented global industry downturn. With a low utilization rate of just 21.7%, fixed costs have become a major drain. Furthermore, the recent high-profile acquisition of ISC, intended to bolster its post-process business, is now under scrutiny. Investors are expressing concerns about the potential for weakened synergy and a longer-than-expected path to profitability improvement, a common challenge discussed in our article on successful M&A integration strategies.

Macroeconomic and Financial Headwinds

Broad economic factors are exacerbating the company’s internal challenges. Volatile raw material prices and slowing global demand are squeezing margins across the board. More alarmingly, SKC’s high debt-to-equity ratio of 188% becomes a significant risk in a rising interest rate environment. This increases the company’s interest burden and strains its financial stability. Adverse currency fluctuations, particularly the appreciation of the KRW against the USD and EUR, also negatively impact a company with substantial foreign currency dealings.

The Road Ahead: Future Outlook for SKC LTD

Despite the grim Q3 results, SKC LTD is actively pursuing a long-term strategy to navigate these challenges. However, the path to recovery is fraught with uncertainty.

Strategic Investments for Long-Term Growth

Management is focused on securing new growth engines by investing heavily in next-generation technologies. Key initiatives include the expansion of the SK Nexilis copper foil plant, a strategic investment in Nexeon to enter the high-growth silicon anode materials business, and the aforementioned acquisition of ISC for the semiconductor post-process sector. The company is also divesting non-core assets to streamline its portfolio and improve capital efficiency. These moves are designed to build a foundation for future growth, even as they strain near-term financials.

Why a Short-Term Recovery is Unlikely

The SKC LTD underperformance is structural, and a quick turnaround is not on the horizon. Persistent market uncertainties in both the battery and semiconductor industries mean that demand is unlikely to rebound sharply. The significant financial burden from the high debt ratio remains a major obstacle that cannot be resolved overnight. This current state negatively impacts corporate value, and any meaningful recovery in SKC LTD stock analysis will depend on a visible improvement in both performance and financial structure.

Investor Action Plan: Key Metrics for Your Watchlist

Given the structural difficulties and financial pressures, investors should adopt a cautious and highly vigilant approach. The following factors are critical to monitor:

- •Market Recovery Timing: Watch for signs of a rebound in the secondary battery materials market and a corresponding improvement in SK Nexilis’ plant utilization rate.

- •Synergy Realization: Monitor the integration of ISC and whether the expected synergies in the semiconductor business begin to materialize in financial reports.

- •Next-Gen Commercialization: Track progress on new ventures like silicon anodes and glass substrates, looking for successful commercialization milestones.

- •Financial Health Improvement: Look for concrete actions to improve the financial structure, such as strategic asset sales or capital increases, and their visible impact on the balance sheet.

In conclusion, while SKC LTD is making long-term strategic bets, the immediate negative SKC LTD earnings report serves as a major deterrent. A meaningful recovery in corporate value will require tangible business achievements and a clear, sustained improvement in financial health.

Leave a Reply