The latest LG Uplus Q3 2025 earnings report has sent a mixed signal to the market, creating a complex puzzle for investors. While the company celebrated a robust revenue figure that comfortably surpassed market expectations, a sharp and unexpected decline in both operating and net profits has cast a shadow over its financial health. This divergence raises critical questions: Is the company’s growth sustainable, or are underlying profitability issues a cause for serious concern for holders of LG Uplus stock?

This comprehensive analysis will dissect the preliminary results, explore the root causes behind the numbers, and provide a clear, forward-looking perspective. We will move beyond the surface-level data to evaluate the company’s strategic investments, competitive landscape, and the macroeconomic headwinds it faces, helping you make a more informed decision about its future.

LG Uplus Q3 2025 Earnings at a Glance

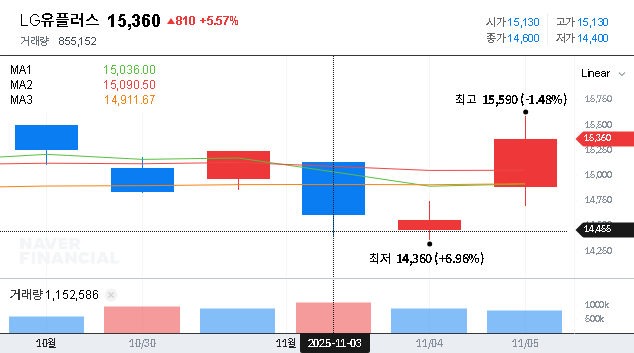

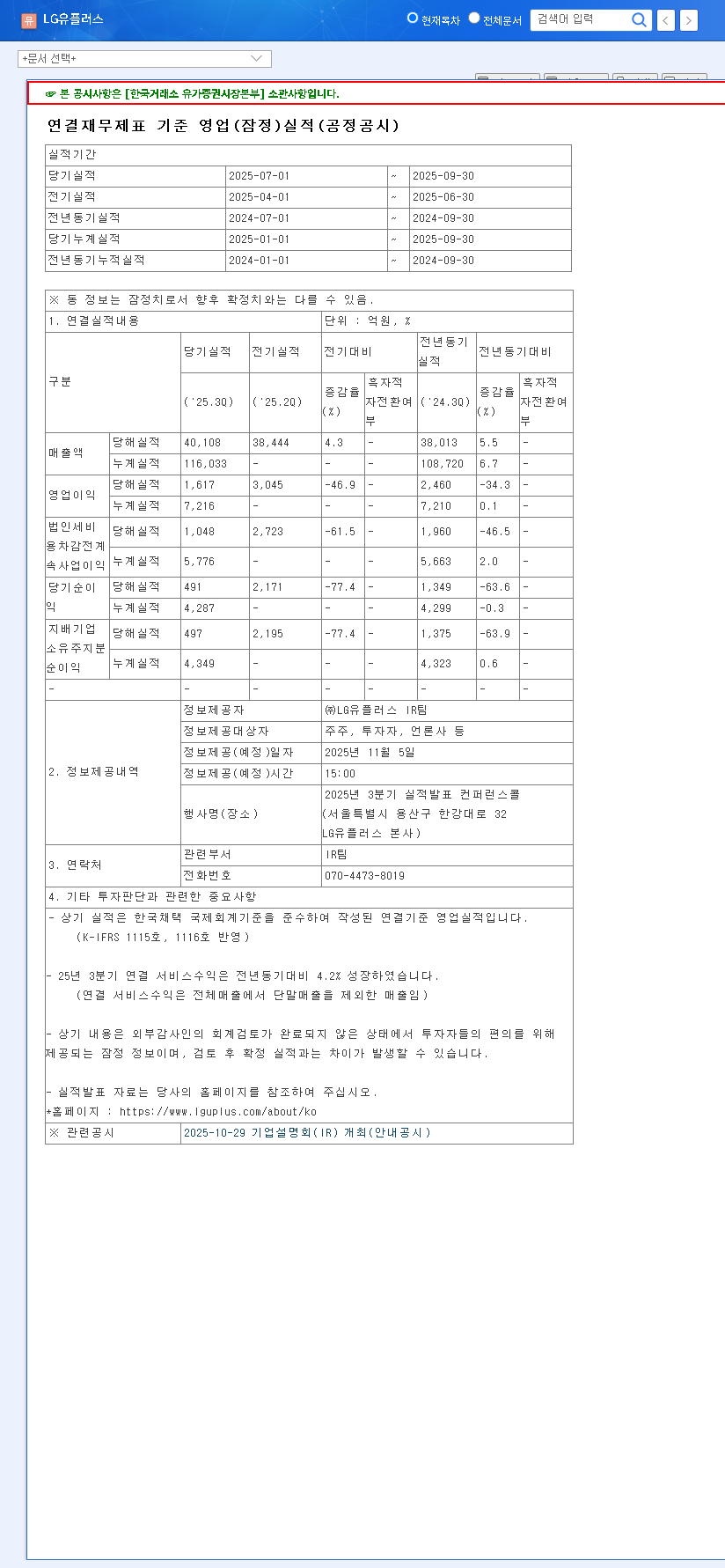

On November 5, 2025, LG Uplus Corp released its preliminary consolidated financial results for the third quarter. The headline figures revealed a significant performance gap between the top and bottom lines. You can view the full Official Disclosure on the DART system for granular details.

The Core Conflict: Revenue growth suggests a healthy core business, but the dramatic profit miss points to escalating costs, competitive pressures, and potentially one-off financial events that require careful scrutiny.

- •Revenue: KRW 4,010.8 billion, a solid 4% above market consensus.

- •Operating Profit: KRW 161.7 billion, a significant -11% below market expectations.

- •Net Profit: KRW 49.7 billion, a staggering -57% below market expectations.

Unpacking the Paradox: Strong Revenue vs. Weak Profitability

To understand the outlook for LG Uplus stock, we must investigate both sides of this financial story. The revenue growth is encouraging, but the profit erosion is a major red flag.

The Bright Side: What’s Driving Revenue Growth?

The top-line beat was not accidental; it stems from solid performance across the company’s key business pillars. This demonstrates that customer demand for its services remains strong.

- •Robust Mobile Segment: A consistent increase in high-value 5G subscribers continues to be a primary growth engine, boosting average revenue per user (ARPU).

- •Expanding Smart Home & Non-Telecom Ventures: The company’s push into non-telecom areas, particularly its Smart Home ecosystem, is showing consistent growth and diversifying its revenue streams.

- •Strong B2B and Enterprise Infrastructure: Enhanced competitiveness in the B2B sector, including cloud and data center solutions, has successfully contributed to the revenue increase.

The Headwinds: Why Did Profits Tumble?

The sharp decline in profitability can be traced to a confluence of strategic spending, market pressures, and broader economic factors. This is the area of greatest concern in the LG Uplus Q3 2025 earnings report.

- •Aggressive Investment in New Growth Engines: Significant capital expenditure on future-facing businesses like EV charging infrastructure and AI/data platforms has increased short-term costs without immediate profit returns.

- •Intensified Market Competition: The South Korean telecom market is fiercely competitive. Higher-than-expected marketing expenses were likely necessary to attract and retain 5G subscribers, eroding margins.

- •Rising Financial Costs: A sustained high-interest rate environment has likely increased the interest burden on the company’s debt, directly impacting net profit. For more on this, see analysis from sources like The Wall Street Journal on global interest rate trends.

- •Potential One-Off Expenses: The sharp drop in net profit could also be attributed to non-recurring costs, such as asset write-downs or restructuring charges, which will need to be clarified in the final report.

Investor Guidance: What’s the Outlook for LG Uplus Stock?

Given the conflicting data, a “Neutral” investment stance is warranted. The company is in a transitional phase, investing heavily for long-term growth at the expense of short-term profitability. The key for investors is to determine if this is a temporary dip or the beginning of a sustained trend of margin compression.

Key Strategic Questions for Investors to Monitor

Before making any investment decisions, closely monitor the company’s progress on these critical points in the upcoming quarters:

- •Path to Profitability for New Ventures: When will investments in EV charging and AI start generating meaningful returns? Look for management commentary on monetization timelines.

- •Cost Control and Efficiency: Are there clear corporate initiatives to streamline operations and reduce marketing spend without sacrificing subscriber growth?

- •Financial Health and Debt Management: How is the company addressing its high debt-to-equity ratio? Monitor any plans for refinancing or deleveraging.

- •Q4 2025 Earnings Performance: The next earnings report will be crucial. A rebound in profitability would suggest Q3 was an anomaly, while continued weakness would confirm a negative trend.

In conclusion, while the LG Uplus Q3 2025 earnings show a company with a robust and growing core business, the challenge of translating that growth into profit remains significant. Prudent investors should adopt a wait-and-see approach, focusing on the company’s ability to manage costs and monetize its new ventures. For more on the competitive landscape, read our deep dive into the Korean telecom market.

Leave a Reply