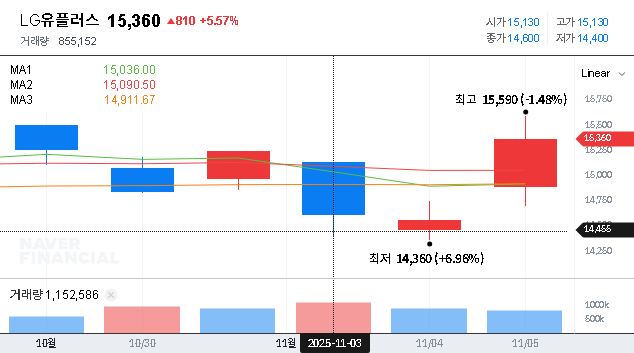

The latest LG Uplus Q3 2025 earnings report has sent ripples through the market, revealing a significant underperformance that caught many analysts and investors by surprise. With net profit falling to less than half of the consensus forecast, stakeholders are now asking critical questions: What triggered this sharp decline, and what does it signal for the future of LG Uplus stock? This comprehensive analysis unpacks the financial results, explores the underlying causes, and provides a strategic guide for navigating the path ahead.

We will provide a deep-dive into the core issues, from intense market competition and heavy investment costs to the challenging macroeconomic environment. By understanding these dynamics, investors can make more informed decisions about their position in LG Uplus Corp.

The Numbers Behind the ‘Earnings Shock’

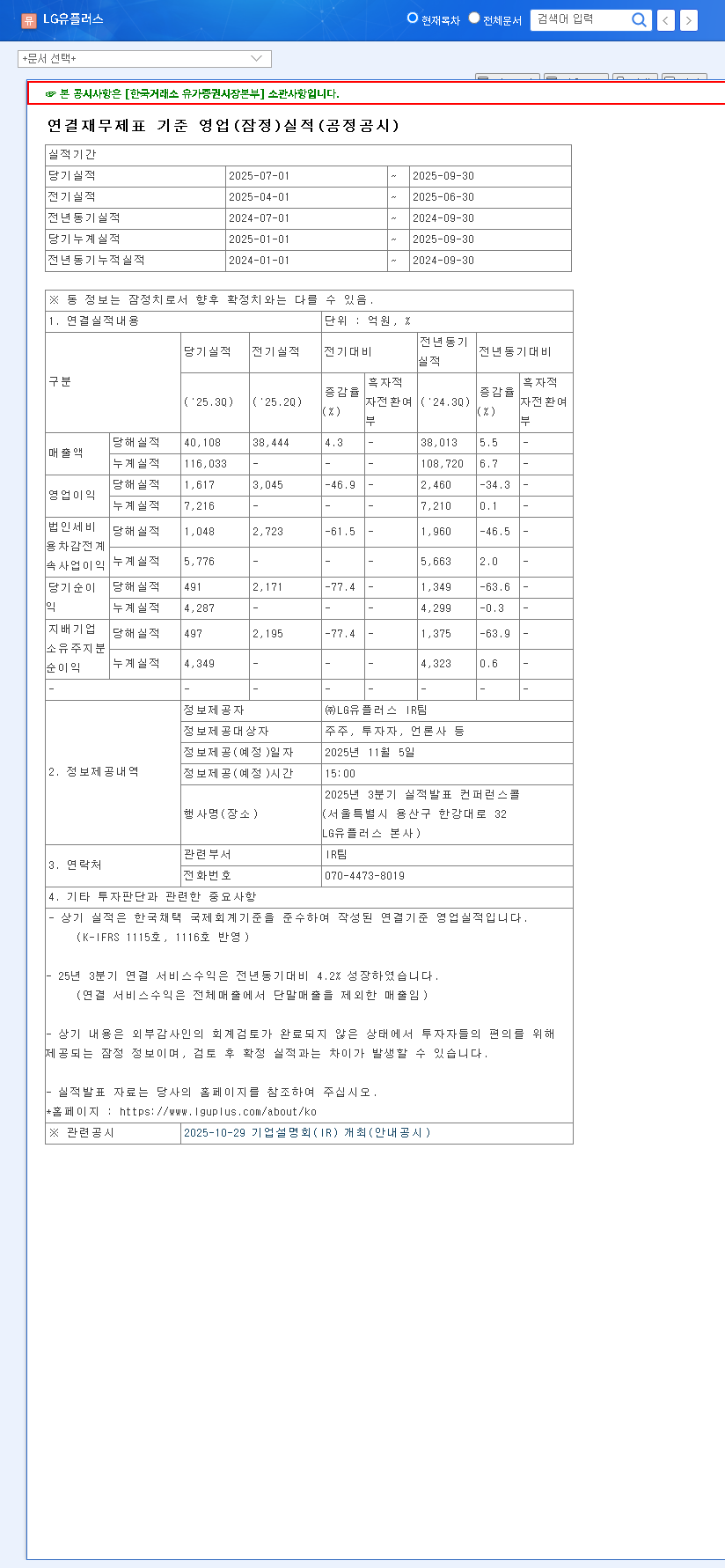

The Q3 2025 financial results starkly illustrate the gap between market expectations and reality. The figures reveal a broad-based miss across all key metrics, with net income showing the most alarming deviation.

Q3 2025 Financial Performance vs. Market Estimates:

• Revenue: KRW 3,713.5 billion (6% below estimate)

• Operating Profit: KRW 156.5 billion (16% below estimate)

• Net Income: KRW 45.2 billion (a staggering 62% below estimate)

This severe LG Uplus profit decline, particularly in net income, signals a significant erosion of profitability. The operating profit margin plummeted from 7.92% in the previous quarter to just 4.21%, while the net profit margin collapsed from 5.65% to a mere 1.22%. These figures raise serious concerns about the company’s current profit structure and operational efficiency.

Unpacking the Causes of the Decline

The disappointing LG Uplus Q3 2025 earnings were not caused by a single issue, but rather a convergence of internal strategic pressures and external economic headwinds.

Intensified Competition & Investment Burdens

The South Korean telecommunications market remains fiercely competitive. This environment forced LG Uplus to increase marketing expenditures to retain and attract customers, directly impacting the bottom line. Furthermore, Average Revenue Per User (ARPU) growth has stagnated despite the launch of new services. Compounding this were the significant upfront costs associated with strategic long-term investments, such as the construction of the new Paju Internet Data Center (AIDC), which are yet to generate substantial returns. These investments, while crucial for future growth, are currently weighing heavily on profitability.

Challenging Macroeconomic Environment

Global economic factors have added another layer of pressure on LG Uplus Corp. These headwinds include:

- •Adverse Exchange Rates: An appreciating Won/Dollar exchange rate increases the cost of imported network equipment and other foreign currency-denominated expenses.

- •Sustained High Interest Rates: The high-interest-rate environment elevates the cost of borrowing, increasing the financial burden of new capital-intensive projects.

- •Inflationary Pressures: Rising international oil prices and logistics costs have driven up operational expenses, from network maintenance to general operating costs.

Future Outlook: Short-Term Pain for Long-Term Gain?

Despite the bleak Q3 results, the long-term picture is not without potential. The company’s heavy investments are targeted at high-growth sectors. The IDC business, in particular, is poised to benefit from the explosive growth of the AI and cloud computing markets, as confirmed by recent market analysis from leading firms. Similarly, strategic pushes into AI services and EV charging infrastructure align with major technological and societal shifts. The key challenge is the timing—when will these future growth engines begin to offset the current drag on profitability and contribute meaningfully to the company’s financial performance?

Actionable Guide for LG Uplus Investors

Given the current volatility, investors considering LG Uplus stock must adopt a cautious and analytical approach. A thorough telecom sector analysis requires focusing on the following critical areas:

- •Monitor New Business Performance: Watch for clear evidence that the IDC, AI, and EV charging segments are beginning to generate significant revenue and, more importantly, profit.

- •Assess Cost Control Measures: Look for management’s strategies to improve operational efficiency and control marketing spend without sacrificing market share. Can they restore the eroded profit margins?

- •Review Primary Sources: For complete due diligence, investors should analyze the company’s primary financial documents. The Official Disclosure on DART provides the full, unfiltered data.

In conclusion, the LG Uplus Q3 2025 earnings represent a significant setback. While the company is making strategic investments for the future, it faces immense immediate pressure. Wise investment decisions will require careful monitoring of the company’s ability to navigate these challenges, which requires a deeper understanding of how to evaluate telecom sector stocks in a volatile market.

Leave a Reply