ECOPRO, a titan in the global secondary battery market, has sent a powerful signal to investors with its Q3 2025 earnings report. After a challenging period of operational losses, the company has officially achieved a ‘black turn,’ returning to profitability. This news has ignited discussions across trading floors, but a closer look reveals a more complex picture. While the return to profit is a significant milestone, a sequential decline in operating profit raises critical questions.

This comprehensive analysis will dissect the ECOPRO earnings report for Q3 2025, exploring the catalysts behind the recovery, the persistent risks that investors must not ignore, and a strategic outlook for the ECOPRO stock. Is this the beginning of a sustained rally, or a momentary reprieve? Let’s find out.

Analyzing ECOPRO’s Q3 2025 Financial Performance

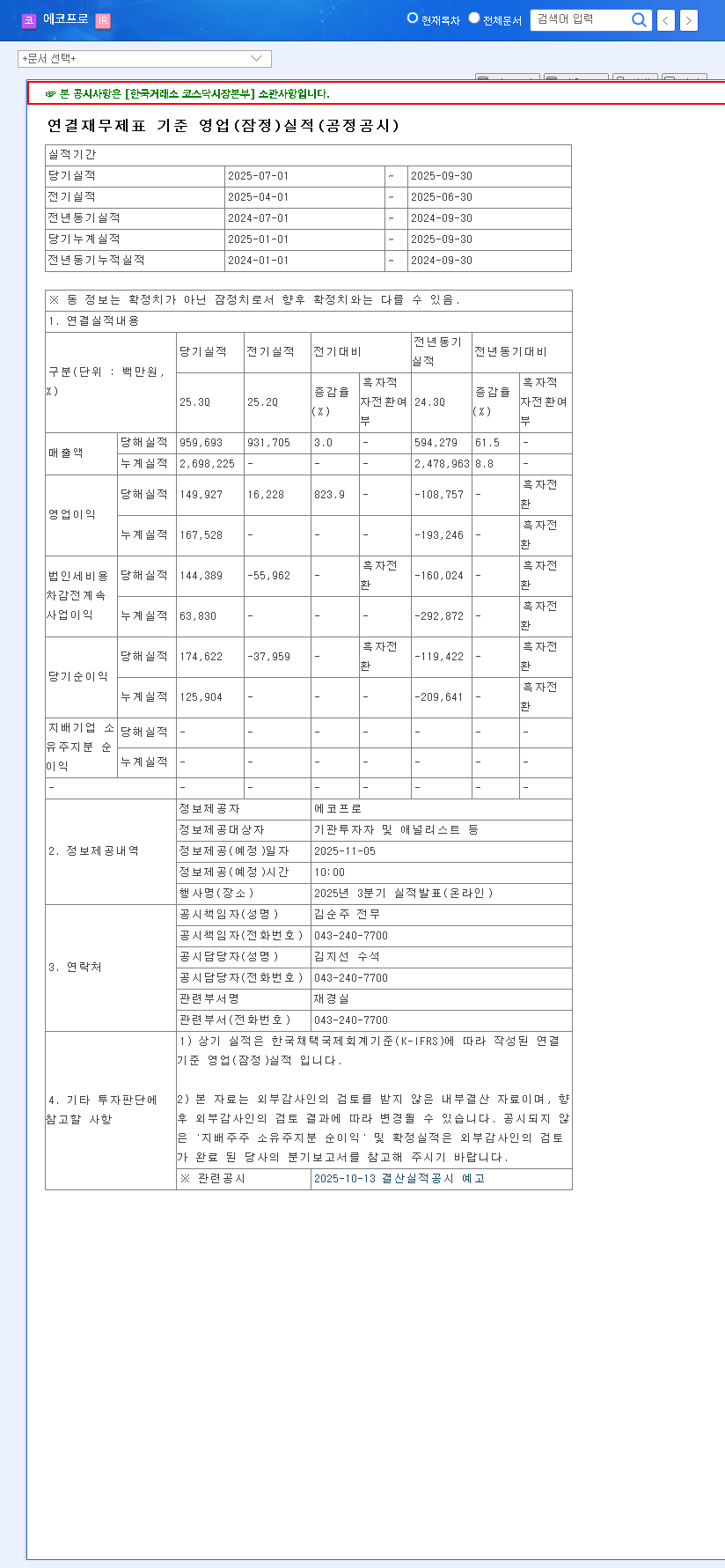

On November 5, 2025, ECOPRO released its provisional consolidated earnings, confirming its long-awaited return to the black. The numbers, as detailed in their Official Disclosure, paint a picture of recovery. Key figures include:

- •Revenue: 959.7 billion KRW

- •Operating Profit: 149.9 billion KRW

This performance successfully breaks the streak of operating losses that began in Q4 2024, demonstrating resilience and a potential rebound in demand for its core products. However, the nuance lies in the quarter-over-quarter (QoQ) comparison, which indicates a slight contraction in operating profit margin, a detail savvy investors are closely monitoring.

The Q3 black turn is a testament to ECOPRO’s operational adjustments and the recovering demand in the EV sector. Yet, the road ahead requires careful navigation of market volatility and competitive pressures.

Growth Catalysts: What’s Driving the Optimism?

Several strategic initiatives are underpinning ECOPRO’s recovery and long-term growth potential. Understanding these is key for anyone considering investing in ECOPRO.

Value Chain Fortification

ECOPRO is proactively strengthening its supply chain. The recent acquisition of a stake in an Indonesian nickel refinery is a masterstroke, aiming to secure a stable supply of a critical raw material and hedge against price volatility. This vertical integration enhances cost competitiveness and reduces external dependencies, a crucial advantage in the turbulent commodities market.

Commitment to R&D and Innovation

The company has expanded its business objectives to include ‘technology research and service consignment.’ This signals a deeper commitment to innovation, likely focusing on next-generation cathode materials and battery recycling technologies. These R&D efforts are vital for maintaining a competitive edge and capturing future growth in the rapidly evolving global EV battery market.

Risk Factors and Headwinds to Consider

Despite the positive turn, a prudent investor must weigh the significant risks that could impact ECOPRO stock performance.

- •Raw Material & Currency Volatility: The prices of lithium, nickel, and cobalt are notoriously volatile. As seen in market analyses by sources like Bloomberg, these fluctuations can directly erode profit margins. Furthermore, a strengthening KRW against the USD can negatively impact export revenues.

- •Intense Market Competition: The secondary battery market is fiercely competitive, with major players constantly vying for market share. Increased competition can lead to price wars and pressure on profitability.

- •Macroeconomic Pressures: Lingering concerns of a global economic slowdown, coupled with high interest rates, can dampen consumer demand for electric vehicles and increase the financial burden on the company.

- •Annual Deficit Concerns: While Q3 was profitable, the company is still projected to post a net loss for the full 2024 fiscal year. A full annual turnaround is necessary to fully restore investor confidence.

Investor Outlook & Strategic Action Plan

ECOPRO is at a critical inflection point. The Q3 2025 results mark the early stages of a turnaround, but stability is not yet guaranteed.

Short-Term Perspective

The initial market reaction may be positive due to the headline profitability. However, the QoQ profit decline could cap immediate upside potential. Expect some volatility as the market digests the full report and awaits Q4 guidance.

Mid-to-Long-Term Perspective

Long-term success hinges on sustained profitability and the tangible results of its strategic investments in R&D and the supply chain. Investors should watch for consistent margin improvement and a clear path to annual profitability in 2026. The growth of the global EV market remains a powerful tailwind, but ECOPRO’s ability to execute its strategy will be the deciding factor.

In conclusion, while ECOPRO’s return to profitability is a commendable achievement, a cautious but optimistic approach is warranted. A thorough analysis of the forthcoming Q4 results and the 2026 annual forecast will be crucial for making an informed investment decision. The company has the potential, but the execution and market conditions in the coming quarters will truly define its trajectory.

Leave a Reply