The latest SK Biopharmaceuticals earnings report for Q3 2025 has sent a clear signal to the market: the innovative drug developer is not just meeting but dramatically exceeding expectations. In a biotech sector known for its volatility, such a significant ‘earnings surprise’ warrants a closer look. This comprehensive analysis will dissect the factors driving this robust performance, evaluate the company’s fundamental health, and provide a forward-looking perspective on the SK Biopharmaceuticals stock outlook.

We’ll explore the incredible momentum of its flagship epilepsy drug, Cenobamate (marketed as XCOPRI®), unpack the company’s strategic pivot into new therapeutic areas, and weigh the opportunities against the inherent risks that investors must consider for any biotech stock analysis.

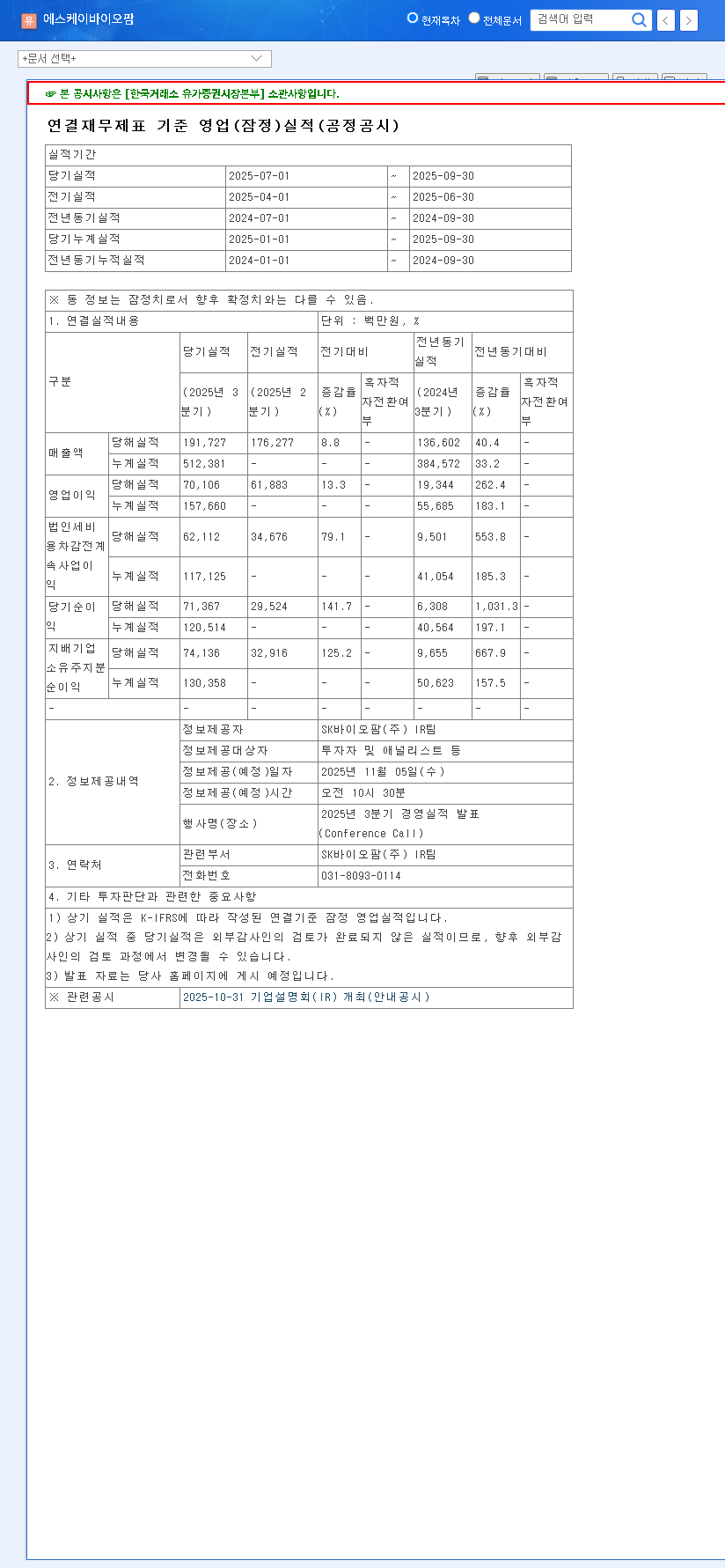

Q3 2025 Earnings Surprise: By the Numbers

On November 5, 2025, SK Biopharmaceuticals announced preliminary consolidated earnings that painted a picture of exceptional financial health and operational efficiency. The results didn’t just edge past market consensus; they shattered it.

- •Revenue: KRW 191.7 billion, a solid 5% above the estimated KRW 182.6 billion.

- •Operating Profit: KRW 70.1 billion, a staggering 51% higher than the KRW 46.5 billion forecast.

- •Net Profit: KRW 74.1 billion, an incredible 123% above the market’s expectation of KRW 33.3 billion.

The massive outperformance in operating and net profit signals a pivotal moment for SK Biopharmaceuticals, demonstrating that the company has matured beyond simple revenue growth into a phase of significant and sustainable profitability.

Core Drivers of This Impressive Performance

Understanding the ‘why’ behind these numbers is crucial for any investor. The success story is multifaceted, rooted in both product excellence and strategic execution.

Cenobamate (XCOPRI®): The Engine of Growth

The primary catalyst is the continued global success of Cenobamate. Strong Cenobamate sales, particularly in the lucrative U.S. market, have solidified its status as a blockbuster drug for partial-onset seizures. Its robust performance validates the company’s direct commercialization strategy, a feat not easily achieved by biotech firms. This success provides the essential cash flow needed to fuel the company’s ambitious R&D pipeline. The drug’s efficacy has been well-documented and recognized by regulatory bodies like the U.S. Food and Drug Administration (FDA), contributing to its strong uptake by neurologists.

Operational Efficiency and Profitability

The remarkable beat on operating and net profit indicates that SK Biopharmaceuticals is mastering the art of cost management. This isn’t just about selling more; it’s about selling smarter. Efficient supply chain management, targeted marketing spend, and disciplined operational oversight are translating top-line growth directly into bottom-line results, a key metric for long-term corporate value.

Fundamental Analysis: Strengths and Risks

Core Strengths Fueling the Future

- •Proven Commercialization Engine: Successfully launching and scaling XCOPRI® in the US provides an invaluable playbook for future product launches.

- •Pipeline Diversification: Strategic entry into new modalities like Radiopharmaceutical Therapy (RPT) and Targeted Protein Degradation (TPD) opens up the high-growth oncology market, reducing long-term reliance on CNS therapies.

- •Financial Stability: A low debt-to-equity ratio provides a strong foundation for continued R&D investment without succumbing to financing pressures, a common challenge in the biotech space. Read more in our analysis of the CNS drug market.

Potential Risks on the Horizon

- •Revenue Concentration: With over 95% of revenue tied to Cenobamate, the company is highly exposed to risks like patent expiry, new competition, or pricing pressure. Diversifying revenue streams is a critical long-term goal.

- •Litigation Headwinds: An ongoing patent infringement lawsuit regarding generic applications for XCOPRI® is a significant variable. An unfavorable outcome could impact future sales projections and the SK Biopharmaceuticals stock price.

- •Macroeconomic Factors: As a global company, fluctuations in the USD/KRW exchange rate can materially affect reported profits. Broader economic trends like interest rates also influence funding costs and investor sentiment in the capital-intensive biotech sector.

Conclusion: Investor Outlook

The Q3 2025 SK Biopharmaceuticals earnings report is an overwhelmingly positive development. It confirms a powerful growth trajectory, showcases improving profitability, and strengthens the company’s narrative as it evolves into a global biopharmaceutical leader. The short-term momentum for its stock is likely to be positive.

For long-term investors, the focus should be on the company’s ability to execute its diversification strategy. Success in the RPT and TPD pipelines will be key to de-risking the company from its reliance on Cenobamate and unlocking the next phase of growth. While risks remain, SK Biopharmaceuticals has proven its ability to execute and is well-positioned for a bright future, provided it continues to manage its portfolio and external risks diligently. For full transparency, investors can review the Official Disclosure filed with DART.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. All investment decisions should be made based on your own research and judgment.

Leave a Reply