The CS Wind Corporation, a global titan in the manufacturing of wind turbine towers, has recently become a focal point for investors. A substantial new supply contract with industry leader Vestas has injected a wave of optimism, yet this positive news is clouded by significant and confusing discrepancies in the company’s reported financial data. This creates a critical question for any potential wind power investment: Is this a sign of resurgent growth or a warning signal to be heeded?

This comprehensive analysis dissects the new CS Wind Vestas contract, unpacks the troubling financial inconsistencies, and provides a clear, actionable investment outlook. We will explore the market tailwinds, potential risks, and what investors should watch for before making a decision on CS Wind stock.

Dissecting the 114 Billion KRW Vestas Contract

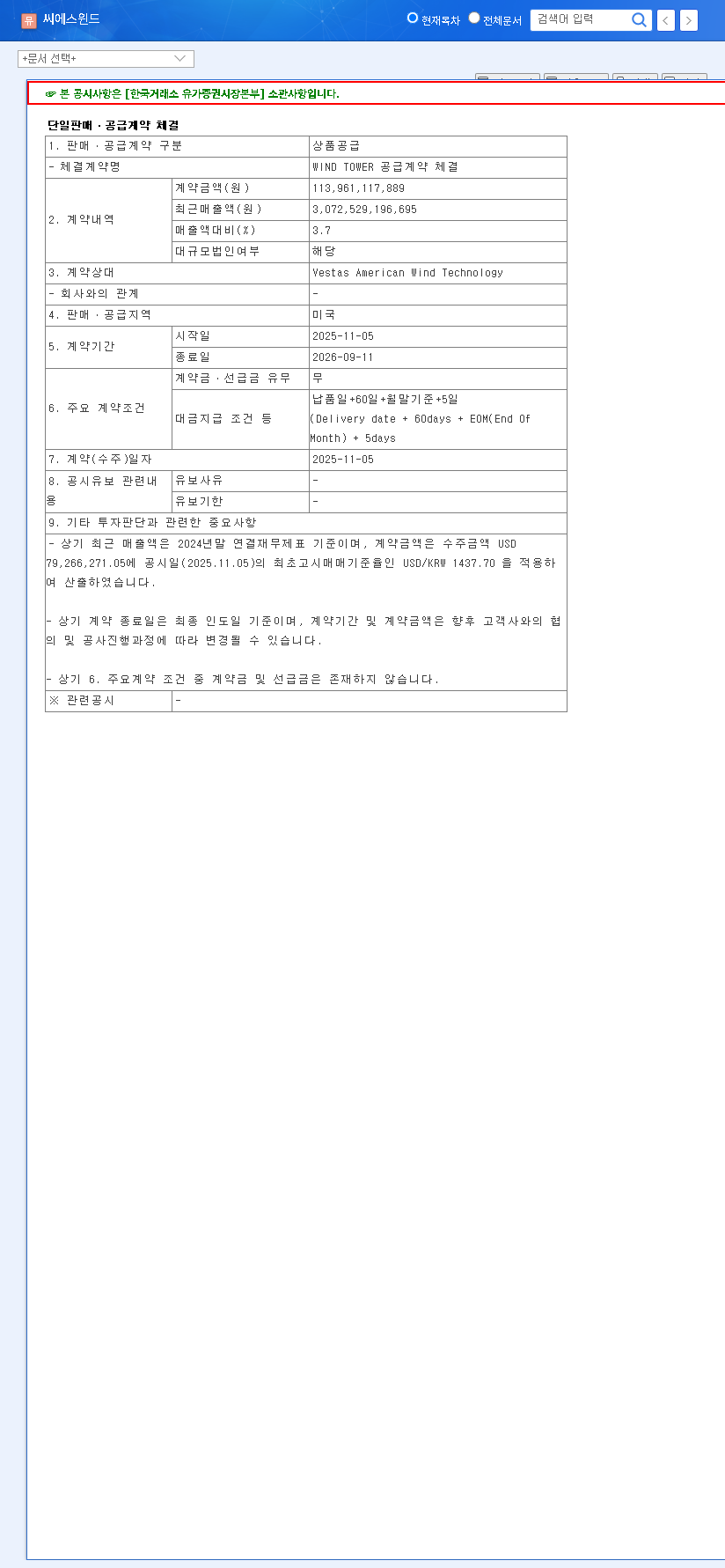

On paper, the latest announcement is a clear victory for CS Wind Corporation. The company secured a major supply agreement with Vestas American Wind Technology, one of the world’s most prominent turbine manufacturers. The deal, valued at approximately 114 billion KRW (approx. $83 million USD), is for the supply of high-demand wind turbine towers to the United States market.

The contract is set to run for 10 months, from November 2025 to September 2026, and represents about 3.7% of the company’s recent annual revenue. While not transformative on its own, this deal is strategically crucial as it reinforces CS Wind’s foothold in the lucrative North American market and deepens its partnership with a key global client.

This contract is more than just a number; it’s a vote of confidence from a market leader. It reaffirms CS Wind’s manufacturing prowess and competitive positioning in a market bolstered by favorable government policies like the IRA.

Market Context: Riding the Green Energy Wave

The deal arrives amidst powerful tailwinds for the renewable energy sector. Global initiatives toward carbon neutrality are creating unprecedented demand. According to the International Energy Agency (IEA), renewable capacity additions are soaring worldwide. Specifically for the wind power market, legislative support like the U.S. Inflation Reduction Act (IRA) and Europe’s REPowerEU plan are providing long-term visibility and financial incentives for projects, directly benefiting supply chain leaders like CS Wind. Furthermore, the company’s strategic 2023 acquisition of Bladt Industries signals a powerful pivot into the high-growth offshore wind substructure market, diversifying its revenue streams for the future. For more details, see our complete analysis of wind energy trends.

The Elephant in the Room: Unpacking Financial Discrepancies

Herein lies the central challenge for investors. While the Vestas contract paints a rosy picture, some available financial forecasts suggest a deeply concerning trend. One set of data projects a sharp decline in revenue, operating profit, and net income for CS Wind Corporation through 2024, with a projected operating profit of just 19.1 billion KRW and a razor-thin margin of 3.05%.

However, this forecast stands in stark contrast to figures presented in other amended annual report analyses, which project a much healthier 2024 revenue of 3,072.5 billion KRW and an operating profit of 255.5 billion KRW. This is not a minor variance; it’s a massive chasm in financial reporting that makes an accurate assessment of the company’s health nearly impossible without further due diligence. Investors must prioritize verifying the company’s status through primary sources.

For the most accurate information, investors should directly consult the company’s regulatory filings. The contract details can be verified via the official disclosure: Source (DART Official Filing).

Investor Action Plan & Final Recommendation

Investment Opinion: Neutral (with a Cautious Watch)

The positive momentum from the CS Wind Vestas contract is undeniable, but it is currently overshadowed by the uncertainty of the company’s true financial standing. A prudent investment approach is required.

Key Factors to Consider:

- •Positive Catalysts: Strong global market growth, supportive government policies (IRA, REPowerEU), solidified client relationships, and strategic expansion into the offshore wind sector.

- •Critical Risks: The alarming discrepancy in financial data is the primary concern. Other risks include the unknown profitability margin of the new contract, USD/KRW exchange rate volatility, and broader macroeconomic pressures like interest rates and supply chain stability.

Recommendation

Do not invest based on headlines alone. Before any capital is committed to CS Wind stock, investors must perform thorough due diligence. This includes reconciling the conflicting financial reports by closely analyzing the company’s latest official quarterly and annual filings. A cautious, wait-and-see approach is warranted until a clear, verified picture of profitability emerges.

Leave a Reply